Why Green Data Centers Matter Now?

Data centers are entering a phase of sustained expansion, with global demand showing no signs of slowing. The sector is projected to grow at a CAGR of 11–13% from 2026–2034, positioning it as one of the fastest-growing infrastructure asset classes and a core enabler of the next wave of digital transformation. This growth is driven by a fundamental shift in how data is generated, processed, and consumed. Cloud computing and artificial intelligence are significantly increasing compute intensity, requiring not only more capacity, but also a new generation of high-density, power-intensive infrastructure. The United States remains the dominant market, hosting approximately 45% of global operational capacity and accounting for 4.4% of national electricity consumption—highlighting the scale at which data centers are evolving from IT assets into major resource consumers.

As hyperscalers expand beyond core markets, Southeast Asia has emerged as a critical frontier. Supported by rapid digital economy growth, rising cloud adoption, and competitive cost structures, the Asia-Pacific region is expected to account for 34% of global operational capacity by 2028, with ASEAN contributing over 50% of the development pipeline in key markets. Relative to mature hubs, markets such as Malaysia, Indonesia, Thailand, and Singapore offer ~20% lower CAPEX and OPEX, alongside 20–30% lower power costs. However, this rapid expansion comes with a growing environmental footprint across the entire data center lifecycle—from construction and continuous 24/7 operations to equipment decommissioning. During operations, reducing environmental impact hinges on the deployment of energy-efficient ICT equipment, sustainable cooling technologies, and access to reliable low-carbon energy. At the same time, improvements in server efficiency, software optimization, and network design are essential to limiting long-term electricity demand and emissions. Data centers also rely on power and water sourced beyond their immediate locations, placing additional strain on regional infrastructure systems.

Sustainability challenges extend to end-of-life management, where large volumes of decommissioned equipment must be handled through structured reuse, repair, and recycling to minimize environmental impact and resource loss.

As demand scales, the cumulative footprint—spanning energy consumption, water use, and e-waste—becomes increasingly material. As a result, sustainability is no longer a secondary consideration, but a core constraint shaping where and how data centers can be developed. Leading hyperscalers such as Google, Amazon Web Services (AWS), and Microsoft are already embedding renewable energy sourcing, water stewardship, and efficiency standards into their infrastructure strategies—making green data centers a baseline requirement rather than a differentiator.

In this context, the key question is no longer simply where data centers can be built, but where they can be built sustainably at scale. For Indonesia, this places increasing importance on its ability to align energy infrastructure, environmental conditions, and regulatory frameworks to support the next generation of green data center development.

Understanding Data Centers: Definition and Key Types

Before assessing market dynamics, it is important to establish a clear understanding of what a data center is and how it is structured.

A data center is a dedicated physical facility designed to house critical IT infrastructure used to process, store, and distribute data and digital applications. These facilities form the backbone of digital services, enabling everything from cloud computing and enterprise systems to artificial intelligence and real-time data processing.

At its core, a data center is built on several key infrastructure layers:

- IT Infrastructure: Servers, storage systems, and networking equipment that handle data processing and transmission.

- Power Infrastructure: High-capacity electrical systems, including backup generators and uninterruptible power supply (UPS), to ensure continuous operations.

- Cooling Systems: Advanced cooling solutions required to manage heat generated by high-density computing environments.

- Connectivity Infrastructure: Fiber networks and interconnection systems that enable high-speed, low-latency data transfer.

Given the critical nature of the data hosted, data centers also require robust physical and digital security systems. This includes multi-layered access controls, surveillance, cybersecurity protocols, and redundancy mechanisms to ensure data protection, operational resilience, and minimal downtime.

From these, then data centers are divided into several types according to its uses:

- Enterprise Data Center: Owned and operated by a single company to support its internal IT needs.

- Usually used for predictable workloads

- Can be on-site or off-site

- Best for companies with strong internal IT capability

- Managed Services Data Center: Operated by a third-party provider, while used by one company.

- Operations and maintenance are outsourced

- Less flexible, but easier to manage

- Suitable for companies that need capacity but lack technical expertise

- Colocation Data Center: Multiple companies share one facility but manage their own servers.

- Provider handles power, cooling, and infrastructure

- Clients control their own IT equipment

- More scalable and cost-efficient than building a facility

- Cloud Data Center: Provides computing services over the internet (on-demand).

- Fully managed by providers

- Highly scalable and flexible

- Includes services like SaaS, IaaS, and PaaS

- Pay only for what you use

- Hyperscale Data Center: Large-scale facilities operated by tech giants like Google, Amazon Web Services (AWS), and Microsoft.

- Designed for massive workloads

- Highly automated and globally distributed

- Backbone of cloud and AI services

- Edge Data Center: Smaller facilities located close to users.

- Reduces delay (latency)

- Supports real-time applications (e.g., IoT, streaming)

- Often operated by telecom, streaming & IoT companies such as Telkom, Netflix, Twitch.

Inside Indonesia’s Data Center Ecosystem

As ASEAN’s largest economy—supported by its population scale, land availability, and natural resources—Indonesia has strong underlying potential to become a major data center hub. As of 2026, the country hosts approximately 184 data centers, with development highly concentrated in a few key locations.

The market is heavily skewed toward Greater Jakarta (99 facilities) and Batam (15 facilities), with the remaining capacity distributed unevenly across secondary cities such as Surabaya, Bandung, Denpasar, etc. This concentration reflects a two-hub structure, where each location serves a distinct strategic role:

- Greater Jakarta as the domestic core

- Batam as the international gateway

Greater Jakarta: The Domestic Core

Greater Jakarta remains the primary center of data center activity and is expected to maintain its dominance in the near term. Its position is driven by a highly concentrated ecosystem of demand, infrastructure, and connectivity. As Indonesia’s political, financial, and commercial hub, Jakarta hosts the largest concentration of end-users and enterprise demand, making it essential for latency-sensitive services. It is also home to the Indonesia Internet Exchange (IIX), where the majority of domestic internet traffic is routed.

This has led to the rapid development of large-scale, carrier-neutral facilities in industrial corridors such as Cibitung, Cikarang, and Karawang, creating strong interconnection hubs for cloud providers, telecom operators, and enterprises. However, this concentration is a double-edged sword. While Jakarta offers scale and connectivity, it also creates risks, particularly given its exposure to climate and infrastructure pressures, including land constraints, energy demand, and environmental vulnerability.

Batam: The International Gateway

Batam plays a distinct role as Indonesia’s primary international data center gateway, driven by its proximity to Singapore—Southeast Asia’s leading digital hub. Positioned along key subsea cable routes, Batam offers low-latency connectivity to global networks, making it attractive for companies prioritizing international data flows. It has increasingly become part of the Singapore–Johor–Batam (SJB) corridor, capturing spillover demand as Singapore faces land and power constraints.

The government has further strengthened Batam’s position through initiatives such as Nongsa Digital Park, offering:

- Tax incentives and holidays

- Streamlined permitting

- Free Trade Zone (FTZ) advantages

These measures aim to position Batam as a regional extension of Singapore’s data center ecosystem, rather than a standalone domestic hub. However, similar to Jakarta, Batam faces climate-related challenges, particularly around cooling efficiency in a hot and humid environment.

Current Market Landscape

Indonesia’s data center market is shaped by a dual structure of local operators and international hyperscalers, creating a competitive environment that is balanced rather than dominated.

The market does not exhibit characteristics of high concentration (dominated by a few players), nor is it overly fragmented with excessive competition. Instead, it sits in a moderate concentration zone, where:

- Local players anchor domestic infrastructure and connectivity

- International players drive hyperscale demand, capital inflows, and technology standards

This results in a hybrid competitive landscape, where competition is present but still evolving, with no single player or small group exerting overwhelming market control.

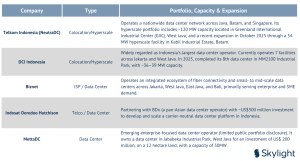

Currently, there are ~16 notable leading players shaping Indonesia’s data center ecosystem.

Local Players (Indonesia):

Source: Various Sources

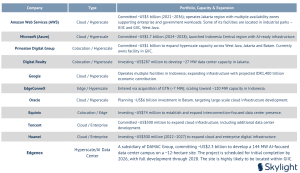

International Players

Source: Powering the Future: Advancing Green Data Centers in Indonesia (Research Report) & Various Sources

Key Market Insight:

Indonesia’s data center market is transitioning from market entry to capacity scaling, where the competitive dynamic is no longer defined by who enters, but by who can deliver large-scale, energy-efficient infrastructure fastest.

- Local players remain critical in providing connectivity, land access, and ecosystem integration

- International players are accelerating hyperscale and AI-driven capacity expansion

- The convergence of both is driving a shift toward industrial park-based, large-format developments

As competition intensifies, the next phase will be defined less by market presence, and more by execution capability—particularly in power availability, sustainability, and speed to deployment.

Key Site Selection Factors

Data centers face growing sustainability challenges, driven by high energy consumption, intensive water usage for cooling, and increasing electronic waste (e-waste). With the rapid rise of AI, these demands are accelerating, placing additional strain on power grids and water resources, and elevating environmental concerns. In response, operators are increasingly locating data centers within industrial parks, which offer a more infrastructure-ready and secure operating environment compared to non-industrial locations.

Industrial parks provide ready access to power, connectivity, and large-scale land, enabling faster deployment and reduced development complexity. At the same time, given the mission-critical and sensitive nature of data, these environments offer controlled access, clear zoning, and managed operations—ensuring high standards of security, reliability, and uptime. To capture this demand, industrial park developers are upgrading their capabilities by increasing power provision, strengthening fiber infrastructure, and developing dedicated zones tailored for data center operations. This trend is clearly reflected in Indonesia’s current data center distribution. While a significant portion remains concentrated in Jakarta, industrial corridors such as Cikarang, where major parks are located—including GIIC, KIIC, Jababeka, MM2100, etc—have also emerged as key data center hubs.

Some industrial parks owns a dedicated data center clusters. For instance, GIIC has introduced a Data Center Park spanning approximately 300 hectares, designed specifically to accommodate large-scale digital infrastructure. The area is supported by high-capacity power supply (up to ~993 MVA from PLN), robust fiber connectivity, and scalable infrastructure, with initial power capacity starting from ~20 MW and expandable up to ~80 MW. This ecosystem has already attracted a growing number of data center operators, reinforcing its position as a specialized hub.

Data center operators typically evaluate locations based on 4 interdependence pillar framework: Energy, Environment, Infrastructure, and Socioeconomics.

1. Energy – The Primary Constraint

Energy is the single most critical factor in data center site selection, often accounting for >50% of total operating costs. For green data centers, the focus extends beyond availability to include scalability, cost, and carbon intensity.

Key considerations:

- Power Availability & Scalability: Access to large, reliable power capacity (often 50–500 MW for hyperscale campuses) with clear expansion pathways.

- Grid Reliability & Quality: Stable grid performance (low outage frequency/duration) and redundancy to meet uptime requirements.

- Power Cost & Long-Term Economics: Competitive electricity pricing, including tariffs, grid fees, and exposure to volatility.

- Energy Mix & Carbon Intensity: Increasing preference for low-carbon energy sources (renewables vs coal), driven by ESG targets.

- Access to Renewable Energy: Proximity to geothermal, hydro, or solar resources, enabling long-term PPAs and carbon reduction commitments.

- Environment – Efficiency and Risk Management

Environmental conditions directly affect both operating efficiency and long-term resilience, making them central to green data center development.

Key considerations:

- Climate & Cooling Efficiency: Cooler, less humid environments reduce cooling loads and improve energy efficiency.

- Water Availability & Regulation: Reliable and sustainable water access for cooling, with increasing scrutiny in water-stressed regions.

- Environmental & Climate Risk: Exposure to flooding, extreme heat, earthquakes, and other natural hazards that may disrupt operations.

- Sustainable Resource Management: Ability to manage water usage (WUE), waste heat, and e-waste responsibly.

- Infrastructure – Connectivity and Execution Readiness

A data center’s value is defined by its ability to connect and operate at scale, making both digital and physical infrastructure critical.

Key considerations:

- Connectivity & Network Access: Proximity to fibre networks, subsea cables, and internet exchanges (e.g., IIX) to ensure low latency and redundancy.

- Ecosystem & Clustering: Presence of existing data center clusters, cloud on-ramps, and enterprise demand, enabling network effects.

- Land Availability & Scalability: Large, contiguous land parcels suitable for campus-style development and future expansion.

- Land Cost & Acquisition Complexity: Pricing, permitting, and ease of acquisition—industrial parks typically offer advantages.

- Physical Infrastructure & Access: Roads, ports, and logistics infrastructure to support construction, equipment delivery, and operations.

- Socioeconomics – Enabling Environment

Beyond physical factors, site selection is heavily influenced by regulatory, economic, and human capital conditions that determine long-term viability.

Key considerations:

- Permitting & Regulatory Certainty: Speed, transparency, and predictability of approvals and compliance requirements.

- Government Support & Incentives: Tax incentives, special economic zones (SEZ/KEK), and policy support for digital infrastructure.

- Security & Operational Environment: Controlled access, zoning compliance, and low-risk environments for mission-critical assets.

- Talent & Operational Ecosystem: Availability of skilled engineers, technicians, and data center operators.

- Economic Competitiveness: Overall cost structure, including labor, land, and infrastructure, affecting total cost of ownership.

Reality Check: Where the Green Data Center Thesis Gets Tested

Renewable Energy in a Coal Dominated Landscape

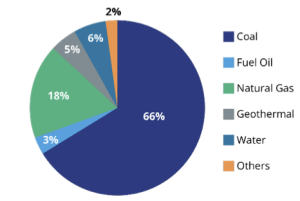

Source: PLN Annual Report 2024

Indonesia’s electricity system is dominated by thermal power generation, primarily coal-fired plants, alongside a smaller but growing contribution from renewable sources such as hydropower, geothermal, solar, and wind. This structure has historically ensured supply reliability and relatively low electricity costs, supporting industrial growth. However, it presents a fundamental challenge for decarbonization—particularly for energy-intensive users such as data centers. In reality, coal remains the dominant source of power generation, accounting for approximately 66.4% of the total energy mix, followed by natural gas (~18%). Renewable sources remain limited, with hydropower (~6%) and geothermal (~5%) forming the bulk of clean energy supply, while other sources such as solar and biomass contribute marginally.

For green data centers—whose operations depend on large, continuous, and reliable power supply—this coal-heavy system creates a constraint. Currently access to renewable electricity in the country is shaped not by resource availability, but by institutional and market factors, including:

- PLN’s centralized control over generation and transmission

- Limited mechanisms for direct renewable procurement (e.g., corporate PPAs)

- Grid rigidity, limiting large-scale renewable integration

Under Indonesia’s current regulatory framework, green data centers have four main pathways to access renewable electricity. Each offers a different balance of control, flexibility, and regulatory complexity.

1. Affiliate as Independent Power Producer (IPP)

In this scheme, green data center developer has an affiliate acting solely as an IPP. Then, the green data center affiliate sells electricity to the integrated IUPTLU holder (PLN or private entity with Wilus) whose Wilus is where the green data center is located. Then, the integrated IUPTLU holder sells electricity to the green data center.

- Requires Power Purchase Agreements (PPAs) with IUPTLU holder

- Subject to competitive bidding (direct selection) under prevailing regulations

- Involves multi-layered contracting (IPP → IUPTLU holder → data center)

Key constraint: Procurement is lengthy and inflexible, as direct appointment is not allowed—even when demand is already secured.

2. Integrated Electricity Supply (Wilus Model)

The data center affiliate operates a fully integrated power business (generation, transmission, distribution) within a designated electricity business area (Wilus).

- Requires Wilus designation + RUPTL approval

- Tariffs must be approved by government (Ministry of Energy and Mineral Resources (MEMR) & House of Representative (DPR))

- Enables direct power supply to the data center

Key constraint: Highly regulated and approval-heavy, limiting speed and scalability.

3. Captive Power (Own-Use Generation)

The data center generates electricity for its own consumption, e.g. via rooftop solar PV under a leasing model.

- Requires IUPLTS (own-use license)

- Commonly structured via operational lease with solar developers

- Capacity limited by PLN quota system (2024–2028 cap)

Key constraint: Scalability is restricted by quota and intermittency, making it insufficient for large hyperscale demand on its own.

4. Grid Joint Utilization (Shared Infrastructure)

Allows renewable power producers to use existing transmission/distribution infrastructure owned by other entities.

- Designed to enable open access to grid infrastructure

- Widely implemented in other markets

Key constraint: Not yet effectively operational in Indonesia, due to regulatory gaps and lack of transmission license issuance.

In practice, Renewable Energy Certificates (RECs) offered by PLN remain the most accessible option, while captive power—particularly within industrial parks—provides partial control over energy sourcing. However, both approaches come with trade-offs. RECs are often viewed as insufficient by hyperscalers seeking verifiable green energy, while captive solutions risk reinforcing fossil-based generation if not directly linked to renewables. Rather than facing a scarcity of renewable resources, data centers in Indonesia operate within a system where coal-based generation remains structurally embedded, and where existing procurement mechanisms are not yet able to support green energy access at scale.

Key implication: Indonesia’s challenge is not resource availability, but system accessibility—without reforms in power market structure and renewable integration, green data center development will remain constrained at scale.

Water Constraints: The Emerging Bottleneck for Green Data Centers

Water is emerging as a critical constraint in data center development, increasingly linked to public scrutiny and community tension. As facilities scale, their cooling requirements place significant pressure on local water systems—particularly in regions where supply is already constrained. Globally, this issue is becoming more visible. In the United States, hyperscale data centers have faced criticism for exacerbating water scarcity in drought-prone regions. In contrast, China has begun experimenting with underwater data centers to reduce both energy and water consumption—highlighting how central cooling efficiency has become to next-generation infrastructure.

A commonly used benchmark is Water Usage Effectiveness (WUE), measured in liters per kilowatt-hour (L/kWh), indicating how much water is required to support computing load. Conventional data centers typically operate at ~1.5–2.5 L/kWh, while more efficient designs can reduce this to below 1.0 L/kWh. The scale of impact becomes clear at the project level.

Let’s take a look in Indonesia: the 54 MW data center facility by NeutraDC in Kabil Industrial Estate, Batam, is estimated to require ~3 million liters of water per day—equivalent to the daily drinking needs of approximately 35,000 people (based on WHO standards).

With around 15 data centers already operating in Batam, cumulative demand is expected to place significant strain on the island’s water system. This risk is already materializing. Batam relies entirely on rainfall-fed reservoirs, distributed through an infrastructure network that remains vulnerable to leaks, maintenance issues, and seasonal variability. Groundwater extraction has been banned, further limiting supply flexibility. As of recent observations, 18 areas across Batam continue to face water shortages, with some residents receiving water for only around four hours per day, forcing reliance on storage tanks and external supply. Tensions have begun to surface. Between late 2024 and 2025, residents have reportedly gathered near Nongsa Digital Park to protest worsening water access, linking shortages to the rapid expansion of data center activity. This reflects a growing friction between industrial-scale digital infrastructure and basic public service provision.

Key implication: Water is not just an operational input, but a shared and constrained resource. Data center expansion must be carefully calibrated against local water capacity—ensuring not only operational reliability, but also equitable access for surrounding communities. This requires stricter planning around water allocation, improved infrastructure, and adoption of low-WUE and alternative water sourcing solutions (e.g., recycled water). Encouragingly, the Indonesian government has begun to recognize and prepare mitigations to support water consumption in data center development.

Defining “Green”: A Fragmented Global Standard

Another structural challenge is that, globally, there is no single standardized framework that fully defines what constitutes a “green data center.” While international standards such as International Organization for Standardization ISO 14001 and ISO 50001 provide guidance on environmental and energy management, they are not data center-specific and are applied inconsistently across operators and regions.

As a result, “green” in the data center context is often defined through a combination of metrics—such as energy efficiency through the Power Usage Effectiveness (PUE), carbon intensity, and water usage through the Water Usage Effectiveness (WUE)—and company-level commitments for best practices, rather than a universally enforced standard.

However, several jurisdictions have begun to move ahead with more structured and sector-specific approaches:

- European Union: Through the Climate Neutral Data Centre Pact, operators voluntarily commit to measurable targets on carbon neutrality, energy efficiency (PUE), water usage (WUE), and circularity by 2030—creating a quasi-standardized, industry-wide benchmark with clear accountability and timelines.

- Singapore: Led by the Infocomm Media Development Authority, the country has developed SS 564 Green Data Centre Standards, a formal national framework tailored specifically to data centers.

- Based on ISO 50001 but adapted for Data Center operations

- Uses Plan–Do–Check–Act (PDCA) for continuous improvement

- Defines standardized performance metrics (e.g., energy efficiency)

- Provides technical best practices across design, cooling, and operations

These examples highlight a clear shift toward codified, measurable, and enforceable definitions of “green” in leading markets. In contrast, Indonesia has yet to establish a dedicated policy or standardized framework specifically governing green data center development. Operators in the country largely rely on a mix of general regulations and voluntary adoption of international standards, resulting in fragmented implementation, limited benchmarking, and inconsistent sustainability outcomes across facilities in the country.

Global Success Cases: What Green Data Centers Look Like in Practice

1. Google Hamina Data Center — Industrial Reinvention Meets Ultra-Efficient Design

Google’s Hamina data center with 140MW capacity (largest data center in Finland), stands as one of the best real-world examples of how sustainability can be embedded into both site selection and engineering design. Located in Hamina, Finland the facility was developed on a repurposed paper mill site acquired from Stora Enso in 2009. What differentiates Hamina is its innovative cooling architecture, which integrates natural conditions with existing infrastructure. The facility leverages seawater from the Gulf of Finland for cooling. Instead of relying on freshwater or energy-intensive cooling systems, seawater is circulated through heat exchangers, significantly reducing both electricity consumption and water stress.

- Seawater from the Baltic Sea is pumped through underground granite tunnels, originally built for the paper mill

- The cold seawater absorbs heat from the servers via heat exchangers

- Water is then returned to the sea at near-original temperature, minimizing environmental disruption

Combined with Finland’s naturally cool climate (average ~2°C), this system significantly reduces reliance on energy-intensive mechanical cooling.

From an energy standpoint:

- The facility operates on Finland’s grid, supplemented by renewable energy through a power purchase agreement (PPA) with a Swedish wind farm

- It achieves a PUE of ~1.09, compared to a global average of ~1.57—indicating extremely low overhead energy use (PUE 1.0 represents theoretical perfection of energy efficiency).

- The site is located in a low-carbon energy region, with a carbon-free energy (CFE%) of ~94%, among the highest in Google’s global portfolio

Key takeaway: Hamina demonstrates that green data center leadership is driven by system integration—combining site reuse, natural cooling, and low-carbon energy sourcing to achieve both operational efficiency and minimal environmental impact.

2. Switch Citadel Campus — Scaling Green Data Centers Through Renewable Energy

The Switch Citadel Campus in Las Vegas represents one of the largest and most advanced green data center developments globally, with projected capacity up to 650MW. Operating in a hot desert climate, where cooling demand is structurally high, Citadel highlights how constraints can be addressed not through geography, but through system design and energy sourcing.

A defining feature of Switch’s model is its early and firm commitment to renewable energy. Since January 2016, all Switch data centers have been powered by 100% renewable energy, positioning the company as a clear industry leader in sustainable operations. This is achieved through large-scale solar integration and long-term renewable procurement strategies, ensuring both energy reliability and carbon reduction at scale.

Key features:

- 100% renewable energy operations since 2016

- Hyperscale, campus-style design enabling modular and efficient expansion

- Advanced cooling and power management systems optimized for extreme climate conditions

- Holds an E-1 environmental rating from S&P Global, the highest possible score, reflecting leadership in sustainability performance and governance

- Maintains a PUE of 1.18, among the sector’s most efficient ratings.

Key takeaway: Citadel demonstrates that green data center development can scale even in resource-intensive environments, provided there is strong alignment between renewable energy access, infrastructure design, and measurable sustainability standards.

From Constraint to Coordination: Making Green Data Centers Work in Indonesia

Indonesia’s data center sector is entering a critical transition—from rapid capacity build-out to execution under structural constraints. Demand fundamentals remain robust, but the next phase of growth will be defined by the sector’s ability to scale sustainably rather than simply expand.

Global benchmarks show that green data centers are fundamentally about leveraging geography as a strategic asset. Google Hamina Data Center utilizes the Baltic Sea for seawater cooling, significantly reducing energy consumption for temperature control. Similarly, Switch Citadel Campus capitalizes on Nevada’s arid climate and abundant solar exposure to optimize cooling efficiency and integrate renewable energy at scale. In both cases, sustainability is not retrofitted—it is engineered by aligning infrastructure design with local terrain and natural conditions. Indonesia, with its diverse geography and renewable resource base, holds a comparable opportunity. However, realizing this potential depends on how effectively the country translates its natural endowments into integrated, site-specific infrastructure strategies.

Sources:

- Skylight Analytics Hub

- Neutradc (n.d.) Jakarta HQ. Available at:https://www.neutradc.com/data-center/jakarta-hq (Accessed: 18 March 2026).

- IBM (n.d.) Data centers. Available at:https://www.ibm.com/id-id/think/topics/data-centers (Accessed: 18 March 2026).

- McKinsey & Company (n.d.) The next big shifts in AI workloads and hyperscaler strategies. Available at:https://www.mckinsey.com/industries/technology-media-and-telecommunications/our-insights/the-next-big-shifts-in-ai-workloads-and-hyperscaler-strategies (Accessed: 18 March 2026).

- Cushman & Wakefield (n.d.) APAC data centre update. Available at:https://www.cushmanwakefield.com/en/singapore/insights/apac-data-centre-update (Accessed: 18 March 2026).

- Tenggara (n.d.) Powering the future: Advancing green data centers in Indonesia. Available at:https://tenggara.id/project/powering-the-future-advancing-green-data-centers-in-indonesia (Accessed: 18 March 2026).

- Mordor Intelligence (n.d.) Indonesia data center market. Available at:https://www.mordorintelligence.com/industry-reports/indonesia-data-center-market (Accessed: 19 March 2026).

- Wood Mackenzie (n.d.) Southeast Asian data centre power demand is set to explode. Available at:https://www.woodmac.com/news/opinion/southeast-asian-data-centre-power-demand-is-set-to-explode/ (Accessed: 19 March 2026).

- Ember Energy (n.d.) From AI to emissions: Aligning ASEAN digital growth with energy transition. Available at:https://ember-energy.org/latest-insights/from-ai-to-emissions-aligning-asean-digital-growth-with-energy-transition/setting-the-scene/ (Accessed: 19 March 2026).

- Maybank KE (n.d.) PDF report: 407187. Available at:https://mkefactsettd.maybank-ke.com/PDFS/407187.pdf(Accessed: 19 March 2026).

- Data Centre Map (n.d.) Indonesia. Available at:https://www.datacentermap.com/indonesia/ (Accessed: 19 March 2026).

- Green DK INSEA (n.d.) High demand for green solutions within Southeast Asia’s booming data centre sector. Available at:https://www.greendkinsea.com/post/high-demand-for-green-solutions-within-southeast-asia-s-booming-data-centre-sector (Accessed: 20 March 2026).

- KPMG (2025) The Asia data centre landscape. Available at:https://assets.kpmg.com/content/dam/kpmg/cn/pdf/en/2025/03/the-asia-data-centre-landscape.pdf (Accessed: 20 March 2026).

- CBRE (n.d.) Key factors to consider for effective data centre site selection. Available at:https://www.cbre.co.uk/insights/articles/key-factors-to-consider-for-effective-data-centre-site-selection (Accessed: 20 March 2026).

- Telkom Indonesia (n.d.) TelkomGroup siap operasikan hyperscale data center Neutradc Nxera Batam. Available at:https://www.telkom.co.id/sites/berita/id_ID/news/telkomgroup-siap-operasikan-hyperscale-data-center-neutradc-nxera-batam-dukung-ekosistem-ai-3387 (Accessed: 20 March 2026).

- Diskominfo Jawa Barat (n.d.) Peresmian data center JK6 PT DCI Indonesia. Available at:https://diskominfo.jabarprov.go.id/postingan/peresmian-data-center-jk6-pt-dci-indonesia-68ae8940abe0a12dd904f09e(Accessed: 20 March 2026).

- DCI Indonesia (n.d.) Homepage. Available at:https://dci-indonesia.com (Accessed: 21 March 2026).

- Biznet Data Center (n.d.) Homepage. Available at:https://www.biznetdatacenter.com (Accessed: 21 March 2026).

- Marketeers (2025) Investasi US$200 juta, data center MettaDC dibangun di Jawa Barat. Available at:https://www.marketeers.com/investasi-us-200-juta-data-center-mettadc-dibangun-di-jawa-barat/ (Accessed: 21 March 2026).

- Capacity Global (n.d.) BDX inks US$300M Indonesian JV with Indosat Ooredoo, Hutchison, and Lintasarta. Available at:https://capacityglobal.com/news/bdx-inks-300m-indonesian-jv-with-indosat-ooredoo-hutchison-and-lintasarta/(Accessed: 21 March 2026).

- Antara News (n.d.) Indonesian govt oversees Microsoft’s US$17 bln investment. Available at:https://en.antaranews.com/news/336717/indonesian-govt-oversees-microsofts-us17-bln-investment (Accessed: 21 March 2026).

- Data Centre Map (n.d.) Amazon AWS CGK Sukamahi. Available at:https://www.datacentermap.com/indonesia/jakarta/amazon-aws-cgk-sukamahi/ (Accessed: 21 March 2026).

- Sinarmas Land (n.d.) Sinar Mas Land hadirkan kawasan perusahaan data di Deltamas. Available at:https://www.sinarmasland.com/news/sinar-mas-land-hadirkan-kawasan-perusahaan-data-di-deltamas (Accessed: 22 March 2026).

- IDN Financials (n.d.) DAMAC Digital asal Dubai bangun data centre US$2.3 miliar di Cikarang. Available at:https://www.idnfinancials.com/id/news/56071/damac-digital-asal-dubai-bangun-data-centre-us-2-3-miliar-di-cikarang(Accessed: 22 March 2026).

- Kominfo Digital (n.d.) Komdigi sambut positif investasi Edgnex senilai Rp37 triliun untuk perkuat infrastruktur data nasional. Available at:https://www.komdigi.go.id/berita/siaran-pers/detail/komdigi-sambut-positif-investasi-edgnex-senilai-rp37-triliun-untuk-perkuat-infrastruktur-data-nasional (Accessed: 22 March 2026).

- Katadata (n.d.) Data center Batam. Available at:https://katadata.co.id/data-center-batam (Accessed: 22 March 2026).

- Antara News (n.d.) AHY minta ekspansi data center perhatikan ketahanan air. Available at:https://www.antaranews.com/berita/5435986/ahy-minta-ekspansi-data-center-perhatikan-ketahanan-air (Accessed: 23 March 2026).

- Katadata (2025) Pemerintah andalkan energi terbarukan untuk genjot investasi data center. Available at:https://katadata.co.id/digital/teknologi/698459f67caa2/pemerintah-andalkan-energi-terbarukan-untuk-genjot-investasi-data-center (Accessed: 23 March 2026).

- IMDA Singapore (n.d.) Green Data Centre Standard. Available at:https://www.imda.gov.sg/regulations-and-licensing-listing/ict-standards-and-quality-of-service/it-standards-and-frameworks/green-data-centre-standard#:~:text=In%20addition%2C%20the%20Green%20DC,was%20published%20the%20same%20year. (Accessed: 23 March 2026).

- Greencode VC (n.d.) Green data center insights. Available at:https://greencode.vc/insights/green-data-center-part1#:~:text=Europe%27s%20Potential%20Advantage,in%20green%20data%20center%20expertise. (Accessed: 23 March 2026).

- Data Centre Dynamics (n.d.) Climate Neutral Data Centre Pact produces audit framework for EU. Available at:https://www.datacenterdynamics.com/en/news/climate-neutral-data-centre-pact-produces-audit-framework-for-eu/#:~:text=Standards%20&%20Regulations-,Climate%20Neutral%20Data%20Centre%20Pact%20produces%20audit%20framework%20for%20EU,continent%20climate%20neutral%20by%202050. (Accessed: 24 March 2026).

- io (n.d.) Hamina Google data center. Available at:https://templ.io/blog/hamina-google-data-center/ (Accessed: 24 March 2026).

- Sustainability Mag (n.d.) How will Google’s Finnish data centre heat reuse plan work. Available at:https://sustainabilitymag.com/news/how-will-googles-finnish-data-centre-heat-reuse-plan-work (Accessed: 24 March 2026).

- Data Centre Magazine (n.d.) How is Switch building AI-ready sustainable data centres. Available at:https://datacentremagazine.com/news/how-is-switch-building-ai-ready-sustainable-data-centres (Accessed: 24 March 2026).

- Dgtl Infra (n.d.) Inside the world’s largest data center. Available at:https://dgtlinfra.com/inside-the-worlds-largest-data-center/ (Accessed: 24 March 2026).