Chapter 1: Preface

1.1 Background

Indonesia’s frozen food industry has moved from being a niche category into a mainstream food consumption segment. The shift is driven by urbanization, rising middle-income households, dual-income families, changing lifestyles, expansion of modern retail, wider e-commerce adoption, and the growing need for convenient food solutions. Frozen food is no longer perceived only as emergency stock or supplementary food; it has increasingly become part of daily household consumption, foodservice operations, small business supply chains, and digital food commerce. Indonesia’s geographic structure also makes the frozen food industry strategically important. As an archipelagic country with more than 17,000 islands, logistics, cold-chain infrastructure, warehousing, and last-mile distribution play a decisive role in the availability, quality, and affordability of frozen food products.

The country’s large population base, expanding urban centers, and rising demand for practical food options create a strong long-term market foundation. At the same time, the same geographic conditions create complexity in maintaining temperature-controlled distribution across regions. The Indonesian Ministry of Foreign Affairs describes Indonesia as the world’s largest archipelagic country, with more than 17,000 islands and around 7,000 inhabited islands, which highlights the structural logistics challenge for cold-chain-dependent sectors such as frozen food. The frozen food market in Indonesia is also becoming more competitive. Established consumer goods companies, poultry processors, seafood producers, meat processors, bakery companies, ready-meal brands, importers, private-label players, and small-to-medium enterprises are all competing in the same consumption space. Major categories include frozen chicken products, nuggets, sausages, meatballs, seafood, dumplings, ready meals, frozen vegetables, frozen potatoes, frozen bakery products, and dessert-related frozen products. From an industry perspective, frozen food sits at the intersection of several important sectors: food manufacturing, agriculture, fisheries, livestock, retail, logistics, e-commerce, household consumption, and foodservice. This makes the industry highly relevant not only as a consumer market, but also as a strategic economic ecosystem.

1.2 Definition and Scope of the Frozen Food Industry

For the purpose of this report, the frozen food industry in Indonesia refers to the production, processing, storage, distribution, import, export, marketing, and consumption of food products preserved through freezing technology. The scope includes both locally manufactured and imported frozen food products sold through retail, wholesale, foodservice, institutional, and online channels.

The report covers the following major product categories:

- Frozen processed meat products, including nuggets, sausages, meatballs, patties, and other poultry or beef-based products.

- Frozen seafood products, including shrimp, fish fillets, squid, crab products, and processed seafood.

- Frozen ready meals, including rice-based meals, pasta, dim sum, dumplings, and other heat-and-eat meals.

- Frozen vegetables and fruits.

- Frozen potato products, including fries and wedges.

- Frozen bakery and pastry products.

- Frozen dessert and specialty products.

- Imported frozen meat, seafood, potatoes, and other frozen processed foods.

- Cold-chain infrastructure and logistics supporting frozen food movement.

- Distribution channels such as supermarkets, minimarkets, traditional markets, foodservice, online grocery, social commerce, and direct-to-consumer platforms.

This report does not treat frozen food only as a packaged consumer product category. Instead, it views the industry as a complete value chain, starting from raw material sourcing and manufacturing, continuing through cold storage and distribution, and ending with consumer purchase and consumption.

1.3 Importance of the Industry

The frozen food industry is important for Indonesia for five major reasons.

- First, frozen food supports food security by extending shelf life and reducing spoilage. In a country where distribution distances can be long and infrastructure quality varies across regions; frozen food can help maintain product availability and quality when supported by proper cold-chain systems.

- Second, the industry supports household convenience. Urban consumers increasingly need food that is easy to prepare, consistent in quality, and available at any time. This is especially relevant for working parents, students, young professionals, small households, and consumers living in urban apartments or boarding houses.

- Third, frozen food supports the foodservice economy. Restaurants, cloud kitchens, hotels, caterers, cafés, and street-food businesses rely on frozen products to maintain consistency, reduce preparation time, control inventory, and minimize waste.

- Fourth, frozen food creates industrial value addition. Indonesia has strong agricultural, poultry, livestock, and fisheries resources. Processing these resources into frozen products can increase economic value, extend market reach, and support export opportunities.

- Fifth, the frozen food industry creates opportunities for SMEs. In recent years, many local entrepreneurs have entered the frozen food category through home-based production, reseller networks, online marketplaces, and social media commerce. This has expanded competition but also raised questions about food safety, licensing, halal certification, packaging standards, and cold-chain reliability.

1.4 Market Relevance from 2020 to 2025

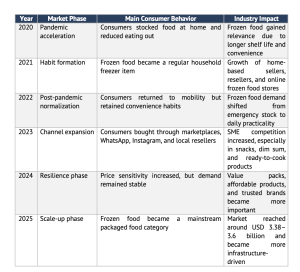

The period of 2020 to 2025 is particularly important because it marks a structural change in consumer behavior. The COVID-19 pandemic accelerated household stocking behavior, online grocery adoption, home cooking, and demand for practical food products. Frozen food benefited from these changes because it offered longer shelf life, ease of preparation, and perceived value for money. After the pandemic, demand did not fully return to pre-pandemic patterns. Many consumers retained the habit of keeping frozen food at home. At the same time, foodservice recovery, cloud kitchen expansion, and online retail growth continued to support frozen food sales. Market research providers estimate that Indonesia’s frozen food market has reached a multi-billion-dollar scale. Mordor Intelligence estimated Indonesia’s frozen food market at around USD 3.38 billion in 2025, with projected growth to USD 3.61 billion in 2026 and USD 5.01 billion by 2031, representing a forecast CAGR of 6.78% for 2026–2031. Another market estimate places Indonesia’s frozen food market at USD 3.55 billion in 2025, with a projection of USD 6.05 billion by 2034, implying a CAGR of around 6.1%.

These figures indicate that Indonesia’s frozen food industry is not a short-term pandemic-driven trend. It is becoming a structural category supported by demographic, retail, logistics, and lifestyle changes.

1.5 Strategic Context of Indonesia

Indonesia has several structural advantages for frozen food market growth.

- The first advantage is population size. Indonesia is one of the world’s largest consumer markets, creating a large domestic demand base for affordable, convenient, and scalable food products.

- The second advantage is the growth of urban consumption. Cities such as Jakarta, Surabaya, Bandung, Medan, Semarang, Makassar, Denpasar, and other urban centers have stronger access to modern retail, freezers, delivery platforms, and foodservice channels.

- The third advantage is raw material availability. Indonesia has significant poultry, fisheries, agriculture, and processed-food manufacturing capacity. This enables local companies to create products tailored to Indonesian taste profiles, including spicy variants, local flavors, halal-certified products, family-sized packs, and affordable price points.

- The fourth advantage is the expansion of digital commerce. Frozen food products are increasingly sold through online marketplaces, WhatsApp reseller networks, Instagram shops, TikTok Shop-style content commerce, quick commerce, and direct-to-consumer delivery models. This allows smaller brands to enter the market without relying only on modern retail shelf space.

However, Indonesia also faces structural constraints. Cold-chain infrastructure remains uneven. Distribution outside Java can be expensive. Electricity reliability, freezer availability, fuel costs, storage standards, and last-mile delivery quality can affect product safety and profitability. These factors make the frozen food business not only a product competition, but also an operational and logistics competition.

1.6 Report Objectives

This report is designed to provide a comprehensive overview of the frozen food industry in Indonesia from 2020 to 2025, while also benchmarking Indonesia against ASEAN, the United States, Australia, and the European Union.

The objectives are:

- To explain the development and relevance of the frozen food industry in Indonesia.

- To analyze market trends and market size from 2020 to 2025.

- To identify major industry players and their competitive positioning.

- To examine distribution networks and logistics coverage.

- To review production, import, and export statistics from 2020 to 2025.

- To identify potential challenges and barriers in the industry.

- To benchmark Indonesia against selected regional and global markets.

- To provide SWOT analysis for Indonesia’s frozen food industry.

- To present the writer’s opinion on the future direction of the industry.

- To conclude with key implications for investors, producers, distributors, and policymakers.

1.7 Research Methodology

This report uses a secondary research approach. The analysis is based on publicly available sources, market research summaries, government statistical references, trade data portals, industry publications, company information, and relevant news sources.

Key source categories include:

- Market research reports and industry summaries.

- Indonesian government statistical platforms, especially BPS export-import data references.

- Trade classification references such as HS codes for food products.

- Company websites and public corporate information.

- Industry news and business media.

- International benchmarks from ASEAN, the United States, Australia, and the European Union.

- Academic or applied research related to frozen food consumption, consumer behavior, and food distribution.

For trade-related sections, the report will refer to the Harmonized System classification used in export-import statistics. BPS provides an export-import data portal and HS Code Master reference, which are relevant for identifying frozen meat, seafood, vegetables, fruit, potato products, and other frozen categories.Because frozen food spans multiple HS codes, the production, import, and export chapter will need to classify the industry into several product clusters rather than relying on one single “frozen food” code. This is important because frozen poultry, frozen beef, frozen fish, frozen shrimp, frozen vegetables, frozen potatoes, and processed frozen meals may be recorded under different trade classifications.

Conclusion

In other words, the future winners of Indonesia’s frozen food industry will likely be companies that can master both consumer branding and operational infrastructure. Frozen food is not only about taste and packaging. It is about reliability, temperature control, stock availability, affordability, and trust. Indonesia has the demand base to become one of the most important frozen food markets in Southeast Asia. However, to unlock its full potential, the industry must overcome logistics fragmentation, quality inconsistency, regional distribution gaps, and the high cost of maintaining cold-chain integrity across an archipelagic market.

Chapter 2: Market Trends and Size of Frozen Food Industry in Indonesia

2.1 Overview

The Indonesian frozen food industry experienced a major structural shift between 2020 and 2025. Before 2020, frozen food was already available in modern retail, foodservice, hotels, restaurants, cafés, institutional catering, and selected household segments. However, the COVID-19 period accelerated consumer adoption because frozen food offered longer shelf life, convenience, portion flexibility, and easier home preparation.

During the pandemic period, Indonesian consumers became more cautious about food availability and household stock. Frozen food benefited from this behavior because it allowed households to reduce shopping frequency while still maintaining food variety at home. Products such as nuggets, sausages, meatballs, dim sum, seafood, frozen snacks, and ready-to-cook meals became more relevant for daily household consumption. From 2022 onward, the market entered a normalization phase. Demand did not disappear after mobility recovered. Instead, many consumers retained the habit of keeping frozen food at home. This shows that frozen food demand in Indonesia was not only a temporary pandemic effect. It became part of a broader lifestyle shift toward convenience, practicality, and time efficiency.

By 2025, Indonesia’s frozen food market had reached a multi-billion-dollar scale. Mordor Intelligence estimated Indonesia’s frozen food market at USD 3.38 billion in 2025, rising to USD 3.61 billion in 2026, with a projected value of USD 5.01 billion by 2031 at a 6.78% CAGR for 2026–2031. IMARC Group estimated the market at USD 3.6 billion in 2025, with a projection of USD 6.1 billion by 2034 at a 5.99% CAGR for 2026–2034. This indicates that the frozen food industry in Indonesia has moved beyond early adoption. It has become a serious consumer goods category supported by urbanization, changing household lifestyles, foodservice demand, e-commerce, and cold-chain development.

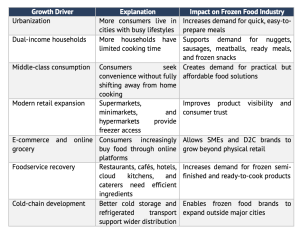

2.2 Key Market Growth Drivers

The frozen food industry in Indonesia is driven by several interconnected factors. The most important drivers are urbanization, time efficiency, dual-income households, modern retail expansion, e-commerce growth, foodservice recovery, and cold-chain development.

2.3 Market Development by Year, 2020–2025

The development of the frozen food industry from 2020 to 2025 can be divided into six phases: pandemic acceleration, habit formation, normalization, channel expansion, resilience, and scale-up.

2.4 Product Category Trends

Frozen food in Indonesia covers many product categories.

- Frozen processed chicken

- Nuggets

- Sausages

- Meatballs

- Frozen seafood

- Frozen dim sum

- Frozen ready meals

- Frozen potatoes

- Frozen bakery and pastry

- Frozen vegetables and fruits

The strongest categories are still processed chicken, nuggets, sausages, meatballs, seafood, and frozen snacks. However, newer growth categories such as ready meals, frozen bakery, dim sum, and frozen potatoes are becoming more relevant.

2.5 Competitive Market Dynamics

The frozen food industry in Indonesia is increasingly competitive. Large companies dominate formal retail and mass-market categories, while SMEs compete through niche products, local flavors, online channels, and reseller networks.

2.5.1 Large Companies vs SMEs

Large companies have advantages in manufacturing scale, procurement, certification, product consistency, cold-chain access, and modern retail distribution. They are more capable of serving national markets. SMEs have advantages in flexibility, speed of innovation, niche products, local taste adaptation, and community selling. Many SMEs succeed by offering products that feel homemade, local, or more specialized. As the market matures, SMEs will need to professionalize. Food safety, halal certification, packaging, shelf-life testing, and distribution reliability will become more important.

2.5.2 Price Competition

Price competition is intense in categories such as nuggets, sausages, meatballs, frozen snacks, and dim sum. Consumers often compare price per gram, package size, and promotional offers. This means brands must manage cost carefully. Raw materials, packaging, electricity, labor, transportation, and cold storage all affect profitability.

2.5.3 Product Differentiation

Product differentiation is becoming more important as more brands enter the market. Common differentiation strategies include local flavor innovation, premium ingredients, family packs, healthier positioning, child-friendly products, spicy variants, halal assurance, and restaurant-quality positioning. The strongest brands are likely to combine product innovation with strong distribution and operational reliability.

2.5.4 Branding and Digital Influence

Frozen food marketing is becoming more visual and content driven. Cooking videos, recipe content, before-after preparation shots, reviews, and user-generated content help consumers understand product quality before buying. This is especially important for online and social commerce. Consumers cannot physically inspect the product, so content, reviews, and seller credibility become important trust signals.

2.6 Market Outlook Entering 2026

Entering 2026, the Indonesian frozen food market is expected to continue growing. The outlook remains positive because the main structural drivers are still present: urbanization, middle-class consumption, foodservice demand, online grocery, and cold-chain investment. Mordor Intelligence projects the Indonesian frozen food market to reach USD 5.01 billion by 2031, while IMARC Group projects it to reach USD 6.1 billion by 2034. However, future growth will not be automatic. The industry will face stronger competition, higher consumer expectations, price sensitivity, logistics cost pressure, and stricter compliance needs. Companies that want to grow in this market must treat frozen food not only as a product category, but as an integrated value chain involving sourcing, manufacturing, freezing, storage, distribution, retail execution, digital marketing, and customer trust.

Chapter 3: Major Players in the Industry

3.1 Overview

The frozen food industry in Indonesia is served by a combination of large integrated food companies, poultry processors, seafood exporters, meat-processing companies, imported-product distributors, foodservice suppliers, retail private labels, and small-to-medium frozen food brands. The competitive landscape is not dominated by one type of company only. Instead, each segment has different major players. Processed chicken and nuggets are mostly dominated by large poultry and consumer-food companies. Frozen seafood is led by seafood processors and export-oriented manufacturers. Sausages and premium processed meat products are driven by both large consumer brands and specialized meat processors. Meanwhile, frozen snacks, dim sum, bakery, and ready meals have more participation from SMEs and local specialty producers. The key point is that frozen food competition in Indonesia is not only about product taste. Major players win through a combination of production capacity, raw material access, halal certification, food safety standards, cold-chain capability, retail distribution, pricing strategy, and brand trust.

3.2 Industry Player Classification

The major players in Indonesia’s frozen food industry can be grouped into several categories:

Classification of Major Frozen Food Players in Indonesia

3.3 Major Players in Processed Chicken and Poultry-Based Frozen Food

Poultry-based frozen food is one of the strongest segments in Indonesia. This includes nuggets, chicken sausages, chicken meatballs, chicken sticks, chicken karaage, breaded chicken, spicy chicken, and other ready-to-cook products. This segment is attractive because chicken is widely accepted by Indonesian consumers, relatively affordable compared with beef, and suitable for halal-certified mass-market products.

3.3.1 PT Charoen Pokphand Indonesia Tbk — Fiesta, Champ, Okey, Akumo

PT Charoen Pokphand Indonesia Tbk is one of the most important players in Indonesia’s poultry and frozen processed food industry. The company is vertically integrated across feed, poultry farming, slaughtering, and food processing. This gives the company strong control over raw material supply and production scale.

Its consumer frozen food brands include Fiesta, Champ, Okey, and Akumo. Fiesta is generally positioned as a higher-quality or premium frozen processed food brand, while Champ and Okey serve broader mass-market needs. These brands are widely found across supermarkets, minimarkets, frozen food stores, and online channels.

Charoen Pokphand’s advantage comes from its integrated poultry supply chain, national distribution network, production capacity, and strong brand recognition. Its ability to serve both modern retail and general trade gives it a strong position in the processed chicken category.

Industry research and applied market studies often identify Fiesta as one of the strongest brands in Indonesia’s frozen processed chicken category. A case study on Belfoods cited Top Brand Index data showing Fiesta, So Good, and Belfoods among the leading frozen food brands in 2022, with Fiesta holding the largest cited share in that study’s category comparison.

3.3.2 Japfa Group — So Good, So Nice, Best Chicken, Olagud

Japfa Comfeed Indonesia is another major integrated agro-food company in Indonesia. The company describes itself as one of Indonesia’s largest agro-food companies and a provider of total poultry solutions, supported by an integrated production chain.

Japfa’s consumer food brands include So Good, So Nice, Best Chicken, and other food products under the Japfa Food ecosystem. So Good is one of the most recognized frozen food brands in Indonesia, especially in nuggets, processed chicken products, sausages, and ready-to-cook items. So Nice is more strongly associated with affordable processed meat and sausage products.

Japfa’s advantage lies in its integrated poultry operations, product variety, brand recognition, and distribution network. The group is positioned not only as a frozen food manufacturer, but also as an integrated food company that can supply both consumer retail and foodservice markets.

Japfa’s public product ecosystem also shows active online retail presence through Japfa Food Official Shop, including chicken, beef slice, and processed products, indicating the company’s participation in modern digital distribution channels.

3.3.3 PT Belfoods Indonesia / PT Sreeya Sewu Indonesia Tbk — Belfoods, Royal

Belfoods is another important frozen food brand in Indonesia. PT Belfoods Indonesia is part of PT Sreeya Sewu Indonesia Tbk and operates in processed chicken-based frozen food. Belfoods states that it is part of an integrated group covering poultry farming through chicken processing.

Belfoods’ products include chicken nuggets, sausages, chicken meatballs, chicken patties, and other processed frozen food products. Third-party company information also describes Belfoods as producing chicken nuggets, sausage, chicken meatball, chicken patty, and mantau, with marketing coverage across modern markets, traditional markets, fast-food restaurants, cafés, and other restaurants.

Belfoods is strategically positioned as an accessible family frozen food brand. The brand has also used affordable price-point strategies and reseller-style networks to reach wider consumers. During the pandemic period, Belfoods was reported to have launched affordable frozen food products at Rp5,000 and Rp10,000 price points and built a Belfoods Entrepreneur Indonesia network to help small entrepreneurs market products through digital and direct channels.

3.3.4 Kanzler — Premium Sausages, Nuggets, and Processed Meat

Kanzler is a premium processed meat and frozen food brand associated with the Cimory Group ecosystem. Kanzler’s own website positions the brand around sausages and meat products made from selected beef and chicken, with product claims such as “Extra Meaty” and “Extra Juicy.” Kanzler has a strong position in sausages, ready-to-eat sausage singles, home-pack sausages, nuggets, and premium processed meat products. Cimory’s product page lists Kanzler sausage products such as Beef Cocktail, Cheese Cocktail, Frankfurter Cocktail, Cheese Frankfurter, Bockwurst, Garlic Frankfurter, Blackpepper Frankfurter, and Bratwurst variants. Cimory also lists Kanzler nugget products such as Crispy Chicken Nugget, Chicken Nugget, Chicken Cordon Bleu, and Crispy Chicken Stick.

Kanzler’s competitive strength is brand premiumization. It competes not only on price, but also on taste, meat content perception, product texture, packaging, and lifestyle branding. This makes Kanzler particularly strong in urban consumers and middle-income households that are willing to pay more for perceived quality.

3.4 Major Players in Frozen Seafood

Indonesia is a major seafood producer and exporter, making frozen seafood one of the most strategically important categories in the industry. Unlike nuggets or sausages, frozen seafood has a stronger export orientation. Key products include frozen shrimp, tuna, tilapia, squid, crab, octopus, cuttlefish, and value-added seafood. Frozen seafood players compete through processing standards, export certifications, access to raw materials, freezing technology, traceability, and compliance with destination-market requirements.

3.4.1 PT Sekar Bumi Tbk

PT Sekar Bumi Tbk is one of Indonesia’s notable frozen seafood and processed food companies. Its annual report explicitly identifies the company as part of the frozen food product manufacturing industry in Indonesia. The company’s public financial highlights show net revenue figures across 2020–2024, indicating its continued participation in the sector across the report period.

Sekar Bumi’s business is closely associated with frozen value-added seafood and processed food. It is an important player because frozen seafood requires more demanding export and cold-chain standards than many domestic processed-food categories.

3.4.2 PT Bumi Menara Internusa

PT Bumi Menara Internusa is one of Indonesia’s well-known seafood processing and export companies. The company appears in Indonesia Seafood’s supplier database, which lists seafood suppliers and includes PT Bumi Menara Internusa among relevant companies. Bumi Menara Internusa is often associated with shrimp and value-added seafood processing. Its relevance comes from export processing capability, seafood sourcing, and cold-chain handling.

3.4.3 PT Medan Tropical Canning & Frozen Industries

PT Medan Tropical Canning & Frozen Industries is also listed in Indonesia Seafood’s supplier database. The company name itself indicates a focus on canned and frozen seafood-related processing. This type of player is important in the Indonesian frozen seafood ecosystem because it connects local marine resources with domestic and export markets.

3.4.4 Regal Springs Indonesia

Regal Springs Indonesia is a major tilapia producer and exporter. Regal Springs states that frozen Indonesian fish products are in demand because of quality, processing standards, and sustainable cultivation practices, and identifies Regal Springs Indonesia as an internationally certified tilapia exporter, including Aquaculture Stewardship Council certification. Regal Springs is strategically important because it represents a more structured aquaculture-based frozen fish model, rather than only wild-capture seafood processing. This is relevant for long-term supply consistency.

Marine Product Indonesia describes its business as delivering premium-quality seafood exports and local frozen food products, showing the dual role of some seafood companies in both export and domestic frozen food markets.

3.5 Major Players in Sausages and Processed Meat

Processed meat is another important segment in Indonesia’s frozen food industry. This includes sausages, smoked beef, sliced beef, meatballs, beef patties, and ready-to-cook meat products.

The segment is shaped by several forces:

- Halal requirements.

- Beef and chicken raw material costs.

- Imported meat dependency for some products.

- Consumer preference for affordable protein.

- Strong demand from foodservice and household channels.

Kanzler stands out in the premium segment, while brands such as So Nice, Champ, and Belfoods compete strongly in broader mass-market consumption. Fiesta remains highly visible in the premium mass-market frozen chicken category.

3.6 Major Players in Frozen Potatoes and Imported Frozen Food

Frozen potatoes, especially French fries, are a major foodservice category. The market is strongly linked to restaurants, cafés, hotels, quick-service restaurants, and home snacking. Unlike poultry-based frozen food, frozen potatoes in Indonesia are more dependent on imports because large-scale French-fry production requires specific potato varieties, processing facilities, and consistent raw material supply. Major global brands and suppliers in the frozen potato category typically include international producers such as McCain, Lamb Weston, Aviko, and other imported frozen potato suppliers. In Indonesia, these products are distributed through importers, foodservice distributors, modern retail, and HORECA suppliers. The competitive advantage in frozen potatoes is not only brand recognition, but also supply reliability, consistent cut size, frying quality, price, and availability for foodservice buyers.

3.7 Major Players in Frozen Ready Meals, Snacks, and Dim Sum

Frozen ready meals and snacks are among the fastest-growing areas for SMEs and local brands. This segment includes dim sum, dumplings, gyoza, risoles, kebab, cireng, pastel, spring rolls, frozen rice meals, pasta, and local ready-to-cook meals. Unlike large-scale poultry processing, frozen snacks and dim sum can be produced at smaller scale. This makes the segment more accessible for home industries and SMEs. However, the segment is fragmented. Many brands operate locally and rely on reseller networks, social commerce, and marketplaces rather than national modern retail distribution. The rise of SME frozen food brands has made the market more dynamic. Many SMEs compete through local taste, affordability, personal branding, social proof, and reseller networks. However, long-term scalability requires formalization through business licensing, halal certification, food safety standards, packaging improvement, and reliable logistics.

3.8 Retail Private Labels and Modern Trade Players

Modern retail chains also play a role in the frozen food industry through private-label products and freezer-based retail distribution. Supermarkets and hypermarkets often sell frozen chicken, seafood, vegetables, fries, meatballs, and snacks under private labels or exclusive supplier arrangements.

Retail private labels are important because they can compete on price and shelf access. Retailers control freezer placement, promotions, and customer traffic. However, private labels must still build consumer trust, especially in frozen food where quality and safety are critical. For major frozen food brands, modern retail is both an opportunity and a challenge. It provides visibility and trust, but also creates cost pressure through fees, promotions, and competition for freezer space.

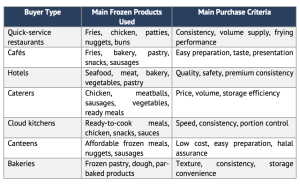

3.9 Foodservice and HORECA Suppliers

Foodservice is a major frozen food demand channel. Restaurants, hotels, cafés, bakeries, caterers, cloud kitchens, canteens, and institutional kitchens often prefer frozen products because they improve operational consistency.

Foodservice suppliers may provide:

- Frozen potatoes.

- Frozen beef and chicken.

- Frozen seafood.

- Frozen bakery and pastry.

- Frozen vegetables.

- Ready-to-cook appetizers.

- Semi-finished meal components.

Foodservice buyers prioritize consistency, price stability, reliable delivery, portion control, and cooking performance. Unlike household consumers, foodservice buyers often make repeat bulk purchases and evaluate products based on operational efficiency.

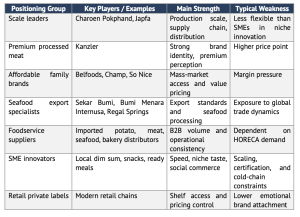

3.10 Competitive Positioning of Major Players

The frozen food industry can be divided into several competitive positioning groups.

Competitive Positioning Map

This map shows that no single type of player dominates the entire frozen food market. Leadership depends on category. Charoen Pokphand and Japfa are strong in poultry-based products. Kanzler is strong in premium sausages and processed meat. Sekar Bumi and other seafood processors are important in frozen seafood. SMEs are highly active in snacks and dim sum.

Chapter 4: Distribution Network and Logistics Coverage

4.1 Overview

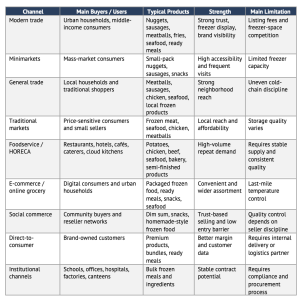

Distribution and logistics are critical factors in the frozen food industry because frozen products require continuous temperature control from production to consumption. Unlike dry packaged food, frozen food can lose quality, texture, safety, and consumer trust if the cold chain is broken. In Indonesia, this issue is even more important because the country is geographically complex. As an archipelagic market, Indonesia requires frozen food companies to manage land transportation, sea freight, regional warehouses, local distributors, freezer display, and last-mile delivery. Therefore, logistics is not only a support activity, but a core part of the frozen food business model. The frozen food distribution system in Indonesia is built around several main channels: modern trade, general trade, foodservice, e-commerce, social commerce, direct-to-consumer delivery, and reseller networks. Large companies usually use multiple channels, while SMEs often rely on local delivery, marketplaces, and community-based resellers.

4.2 Main Distribution Channels

Frozen food products in Indonesia are distributed through both formal and informal channels. Modern retail provides trust and visibility, while general trade and resellers provide wider neighborhood reach. Foodservice serves bulk buyers, while e-commerce and social commerce support direct access to consumers.

Main Distribution Channels for Frozen Food in Indonesia

4.3 Modern Trade and General Trade

Modern trade remains one of the most important channels for established frozen food brands. Supermarkets, hypermarkets, and minimarkets provide freezer infrastructure, consumer traffic, product comparison, and retail credibility. Products from brands such as Fiesta, Champ, So Good, Belfoods, and Kanzler are commonly distributed through modern retail because these channels support national brand visibility. However, modern trade also creates barriers. Brands need to compete for freezer space, pay listing or promotion costs, and maintain consistent stock. This channel is easier for large players than for SMEs because it requires certification, packaging standards, production consistency, and distribution reliability. General trade and traditional markets remain highly relevant, especially for price-sensitive consumers. Frozen food products such as meatballs, sausages, frozen chicken, seafood, and local snacks are sold through neighborhood shops, wet markets, wholesalers, and small distributors. This channel provides strong local reach, but cold-chain discipline can vary depending on freezer quality, electricity reliability, and seller handling.

4.4 Foodservice and HORECA Channel

Foodservice is a major B2B distribution channel for frozen food in Indonesia. Restaurants, hotels, cafés, caterers, canteens, cloud kitchens, and bakeries use frozen products because they help reduce preparation time, maintain consistency, and control inventory. Foodservice buyers usually prioritize consistency, price stability, supply reliability, portion control, and cooking performance. For example, cafés and restaurants may use frozen fries, chicken, sausages, seafood, pastry, bakery products, and semi-finished ingredients to simplify operations.

Foodservice Frozen Food Distribution

The foodservice channel offers stable volume, but it also requires operational discipline. Suppliers must provide reliable delivery, consistent quality, and competitive pricing. If a product becomes part of a restaurant menu, supply failure can directly affect the buyer’s business.

4.5 E-Commerce, Social Commerce, and Reseller Networks

E-commerce and social commerce have become important channels for frozen food, especially after 2020. Consumers now buy frozen products through online grocery platforms, marketplaces, brand-owned stores, Instagram, WhatsApp, TikTok-style content commerce, and reseller networks. This channel is especially useful for SMEs because they can sell directly without entering modern retail. Products such as dim sum, risoles, kebab, cireng, frozen snacks, and homemade-style ready meals often grow through community-based selling. However, online frozen food distribution is operationally challenging. Sellers must manage insulated packaging, ice gel, delivery radius, same-day delivery, and customer communication. If the product arrives thawed or damaged, customer trust can decline quickly.

4.6 Cold-Chain Infrastructure

Cold-chain infrastructure is the backbone of frozen food distribution. It includes production freezing, blast freezing, cold storage, regional cold hubs, refrigerated trucks, freezer displays, insulated packaging, and temperature monitoring. Indonesia’s cold-chain infrastructure has improved, but coverage remains uneven. Java and major cities generally have better cold-chain capacity, while outer islands and secondary cities often face higher logistics costs and weaker infrastructure. Cold-chain capability determines how far a brand can scale. Brands with better cold storage, reefer transport, and distributor discipline can expand beyond major cities more effectively.

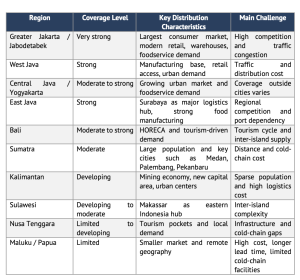

4.7 Regional Logistics Coverage

Frozen food logistics coverage in Indonesia is strongest in Java because Java has the highest concentration of population, manufacturing, modern retail, warehouses, ports, and foodservice demand. Greater Jakarta, Bandung, Semarang, Yogyakarta, Surabaya, and surrounding areas are the strongest frozen food markets. Outside Java, distribution becomes more complex. Sumatra, Kalimantan, Sulawesi, Bali, Nusa Tenggara, Maluku, and Papua require stronger regional hubs and inter-island logistics. Sea freight, port handling, local cold storage, and last-mile delivery become major factors.

Regional Frozen Food Logistics Coverage in Indonesia

This regional structure means national expansion usually starts from Java, then moves to Sumatra, Bali, Sulawesi, Kalimantan, and selected eastern markets.

4.8 Last-Mile Delivery and Logistics Cost

Last-mile delivery is one of the most difficult parts of frozen food distribution. Products must remain frozen or within safe temperature limits until they reach the customer. In urban areas, traffic, heat, and delivery delays can increase thawing risk. Frozen food logistics is also more expensive than dry food logistics because it requires electricity, cold storage, refrigerated vehicles, insulated packaging, ice gel, freezer maintenance, and temperature monitoring. Because of this cost structure, frozen food brands need to carefully manage minimum order quantity, delivery radius, packaging format, and pricing strategy.

4.9 Strategic Implications

Distribution and logistics are central to competitive advantage in the frozen food industry. Large manufacturers need national freezer visibility, strong distributor governance, and regional cold hubs. SMEs need to control delivery radius, improve packaging, train resellers, and avoid scaling faster than their logistics capability. For foodservice suppliers, the priority is consistent supply, stable pricing, and delivery reliability. For e-commerce brands, the priority is last-mile quality, packaging, delivery timing, and customer communication.

4.10 Chapter Conclusion

Distribution and logistics are fundamental to the growth of Indonesia’s frozen food industry. The industry cannot be understood only through product innovation or consumer demand because frozen food depends heavily on temperature-controlled infrastructure. Modern trade provides visibility and trust. General trade provides local reach. Foodservice provides repeat volume. E-commerce and social commerce create new growth channels. However, every channel requires different logistics capabilities. The main conclusion is that frozen food companies in Indonesia compete not only through product and price, but also through logistics reliability. Brands that can maintain product quality, stock availability, cold-chain control, and delivery consistency will have stronger long-term competitiveness.

Chapter 5: Production, Export and Import Statistics

5.1 Overview

The production, import, and export structure of Indonesia’s frozen food industry is complex because “frozen food” is not recorded under one single statistical category. Frozen food covers multiple product groups, including frozen poultry, processed chicken, sausages, nuggets, meatballs, frozen seafood, frozen shrimp, frozen fish, frozen beef, frozen potatoes, frozen vegetables, frozen bakery, and ready-to-cook products.

Therefore, this chapter analyzes the industry through three main dimensions:

- Domestic production capacity and production scale, especially from major players mentioned in Chapter 3.

- Export performance, mainly driven by seafood, shrimp, fish, and value-added seafood.

- Import dependency, especially for frozen beef, buffalo meat, meat products, frozen potatoes, and selected specialty frozen ingredients.

The key conclusion is that Indonesia has strong domestic capability in poultry-based frozen food and seafood processing, but still depends on imports for frozen beef, processed meat inputs, frozen potatoes, and selected foodservice products.

5.2 Statistical Classification and Data Limitation

Frozen food is spread across several HS code categories. This makes official statistics fragmented. BPS provides export-import data and HS code references, but frozen food must be interpreted by product cluster rather than as one single commodity. Relevant categories include frozen meat, frozen poultry, frozen fish, frozen shrimp, frozen vegetables, processed meat, prepared seafood, frozen potatoes, and prepared foods.

Main HS Code Clusters Relevant to Frozen Food

Because of this classification issue, the statistics in this chapter should be read as category-level indicators, not as a single audited national frozen food total.

5.3 Domestic Production Structure and Major Player Capacity

Indonesia’s domestic production is strongest in poultry-based frozen food, processed chicken, sausages, nuggets, meatballs, and seafood. Large integrated poultry companies control much of the formal processed chicken market, while seafood processors support both domestic supply and export demand. Major players such as Charoen Pokphand Indonesia, Japfa / So Good Food, Belfoods / Sreeya Sewu, Cimory / Kanzler, and Sekar Bumi represent different production strengths in the industry.

5.3.1 PT Charoen Pokphand Indonesia Tbk

PT Charoen Pokphand Indonesia is one of the strongest players in processed chicken and poultry-based frozen food. Its processed chicken brands include Golden Fiesta, Fiesta, Champ, Okey, Akumo, and Asimo. The company’s 2024 annual report stated that its processed chicken brands include products such as karaage, nuggets, spicy wings, sausages, and others. In 2024, Charoen Pokphand’s processed chicken net sales reached Rp11.94 trillion, increasing from Rp10.01 trillion in 2023, or around 19.31% growth. The company stated that the increase was mainly caused by higher sales quantity and expansion of processed chicken plants. Charoen Pokphand also reported that its processed chicken products had approximately 47% market share, indicating its leadership position in the processed chicken category.

5.3.2 PT Japfa Comfeed Indonesia Tbk / PT So Good Food

Japfa is another major integrated poultry and processed-food company. Its downstream frozen and processed food brands include So Good, So Nice, Best Chicken, and Olagud. Japfa is described in its 2025 annual report as one of Indonesia’s main livestock players and the second-largest player in terms of production capacity for DOC, feed, and carcass, while also being one of the biggest players in the processed chicken meat industry. For operational scale, a government-related livestock monitoring document stated that PT So Good Food’s poultry slaughterhouse had a cutting capacity of 32,000 chickens per day, chilling room capacity of 60 tons per day, and cold storage capacity of 750 tons. This shows that Japfa’s production strength is not only brand-based, but also supported by upstream poultry infrastructure, slaughtering, chilling, cold storage, and processed-food manufacturing capability.

5.3.3 PT Sreeya Sewu Indonesia Tbk / PT Belfoods Indonesia

PT Belfoods Indonesia, part of PT Sreeya Sewu Indonesia Tbk, produces processed frozen chicken products under brands such as Belfoods, Royal by Belfoods, Uenaaak by Belfoods, and Bonanza by Belfoods. Belfoods states that it has factories in Bogor, West Java and Nganjuk, East Java, with three main production lines: nuggets, meatballs, and sausages. A secondary annual-report source for Sreeya Sewu stated that Belfoods’ production capacity reached 25,200 tons per year. Because this number is not as directly accessible from the current official page, it should be treated as an indicative capacity reference rather than a fully verified current capacity figure.

5.3.4 Cimory Group / PT Macroprima Panganutama — Kanzler

Cimory Group operates in premium consumer food through the Kanzler brand. Its 2024 annual report stated that Kanzler’s portfolio includes sausages, chicken nuggets, luncheon meat, and meatballs, and that Kanzler is known as a pioneer in ready-to-eat sausages and meatballs under the Kanzler Singles line. Cimory’s consumer food segment recorded Rp5.16 trillion in net sales in 2024, increasing by 25% from the previous year. Although Cimory does not publicly disclose a frozen-food tonnage capacity for Kanzler in the same way as some poultry processors, its revenue scale and product portfolio indicate a major role in premium processed meat and frozen-ready-to-cook products.

5.3.5 PT Sekar Bumi Tbk

PT Sekar Bumi Tbk is one of the key players in frozen seafood and value-added seafood. Sekar Bumi publicly states that it has 45,000 tons per year of production capacity, more than 80 product types, more than 20 export destination countries, and more than 4,000 partner outlets.

In its 2025 annual report, Sekar Bumi reported value-added seafood production of 21,153 tons in 2025, up 23.76% from 17,093 tons in 2024. It also reported processed food production of 5,810 tons in 2025, up 9.17%from 5,322 tons in 2024. This positions Sekar Bumi as one of the most important frozen seafood and export-linked processed food companies in Indonesia.

5.5 Production Trend, 2020–2025

From 2020 to 2025, domestic production was shaped by household demand, foodservice recovery, and downstream processing investment. In 2020–2021, pandemic-related home consumption increased demand for long-shelf-life products such as nuggets, sausages, meatballs, dim sum, and ready-to-cook meals. Large companies benefited from established production and distribution systems, while SMEs entered frozen snack categories through online and reseller channels.

In 2022–2023, the market normalized. Foodservice reopened, supporting frozen poultry, frozen potatoes, seafood, bakery, and semi-finished ingredients. Consumer demand shifted from emergency stock to routine convenience. In 2024–2025, the market entered a more competitive production phase. Charoen Pokphand expanded processed chicken plants and grew processed chicken sales volume. Sekar Bumi increased value-added seafood and processed food production in 2025.

Meanwhile, the government’s food security and free-meal program direction increased the strategic importance of domestic protein and processed-food capacity. Reuters reported that Indonesia planned around Rp371 trillion, or roughly US$22 billion, in agricultural processing investment, including livestock and food processing sectors.

5.6 Export Statistics: Seafood as Indonesia’s Main Frozen Export Strength

Indonesia’s strongest frozen-food-related export category is seafood. Seafood exports include frozen shrimp, fish, tuna, squid, crab, tilapia, molluscs, and value-added seafood products. Not all seafood exports are frozen, but frozen seafood is a major part of the export structure. Indonesia’s seafood exports were reported at US$6.27 billion in 2025, up 5.2% from the previous year, with the United States as the largest market. Earlier data also shows that Indonesia’s fishery export value peaked at about US$6.24 billion in 2022 before falling to about US$5.63 billion in 2023.

5.7 Shrimp Export and Seafood Risk

Frozen shrimp is one of Indonesia’s most important seafood export products. Reuters reported that Indonesia’s shrimp exports were worth around US$1.68 billion in 2024, with the United States accounting for about 60% of exports. Another Reuters report stated that the U.S. accounted for 63.7% of Indonesia’s 215,000 tonnes of shrimp exports in 2024, valued at US$1.7 billion. This shows that shrimp is a strong export product, but also highly exposed to U.S. demand, tariffs, and food safety requirements. In 2025, Indonesian shrimp exporters faced pressure from new U.S. tariffs, and Reuters reported that exporters were exploring China and other markets as alternatives. A separate Reuters report also described a Cesium-137 contamination case that affected buyer confidence and reduced processing absorption in parts of the shrimp industry.

5.8 Import Statistics: Meat, Beef, Seafood, and Frozen Potatoes

Indonesia remains import-dependent in several frozen-food-related categories, especially meat, beef, buffalo meat, and frozen potato products. For meat, Agriculture and Agri-Food Canada reported that Indonesia imported US$862.3 million or 252.0 thousand tonnes of fresh and processed meat products in 2024. Its top suppliers were Australia, India, the United States, Brazil, and New Zealand. Frozen boneless bovine meat was the largest meat import item, valued at US$569.5 million or 143.7 thousand tonnes in 2024.Historical meat import data shows Indonesia’s meat imports rose from US$736.1 million in 2020 to US$1.103 billion in 2022, then declined to US$862.3 million in 2024. In volume terms, imports rose from 230,362 tonnes in 2020 to 317,005 tonnes in 2023, before falling to 251,961 tonnes in 2024. For fish and seafood imports, Agriculture and Agri-Food Canada reported Indonesia imported US$509.0 million or 309.2 kilotonnes in 2024, up from US$394.9 million or 254.7 kilotonnes in 2020. Top imported fish and seafood products in 2024 included frozen mackerel, fish meals/pellets, and frozen crab.

Frozen potato products are important for foodservice, but official public figures are less consistently available under one clean category because frozen potatoes may be recorded differently depending on the HS classification used. Therefore, this report treats frozen potatoes as an import-dependent foodservice category, especially for French fries, wedges, and hash browns.

5.9 Chapter Conclusion

Indonesia’s frozen food production, import, and export structure is mixed. The country has strong domestic capability in poultry-based frozen food and seafood processing. Charoen Pokphand, Japfa / So Good Food, Belfoods / Sreeya Sewu, Kanzler / Cimory, and Sekar Bumi are among the most important production-side players, each with different strengths.

Chapter 6: Potential Issues and Challenges

6.1 Overview

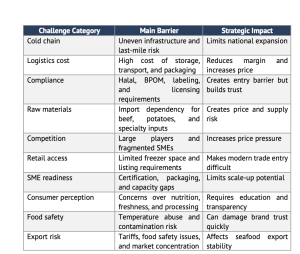

Indonesia’s frozen food industry has strong growth potential, but the industry also faces structural barriers that can limit scalability, profitability, and consumer trust. These barriers are not only related to product competition. They are also connected to cold-chain infrastructure, logistics cost, price sensitivity, food safety, halal compliance, raw material dependency, import regulation, and SME readiness.

The main challenge is that frozen food requires an integrated value chain. A company must manage sourcing, production, freezing, storage, distribution, retail placement, last-mile delivery, and post-purchase handling. Failure in one part of this chain can damage the whole product experience. In Indonesia, the barriers are more complex because of geography. Java and major urban centers have stronger cold-chain infrastructure, while outer islands and secondary cities often face higher logistics costs and weaker temperature-controlled distribution. As a result, national expansion is difficult for brands that do not have strong logistics partners or regional cold hubs.

6.2 Cold-Chain and Logistics Barriers

Cold-chain infrastructure is the most important operational barrier in the frozen food industry. Frozen food must remain within proper temperature conditions from production to consumption. If the product thaws during transport or storage, quality, texture, shelf life, and food safety can be affected. Indonesia’s cold-chain infrastructure is improving, but it remains uneven. The Indonesian Cold Chain Association, ARPI, highlighted that the significant increase in Indonesia’s frozen food market requires better governance from the first mile to the last mile to maintain freshness, safety, and nutritional value. ARPI also noted that cold-chain growth in 2025 would continue to be supported by third-party logistics players, private companies, refrigerated transportation, last-mile providers, and processors of fresh produce into ready-to-eat products. Cold-chain barriers make frozen food a logistics-heavy business. Companies that can solve this issue will have stronger national scalability than competitors that rely only on product quality or low price.

6.3 Price Sensitivity and Cost Pressure

Indonesia is a highly price-sensitive consumer market. Frozen food must compete not only with other frozen food brands, but also with fresh food, street food, home cooking, and ready-to-eat meals from food delivery platforms. Consumers often compare frozen food based on price per gram, pack size, promo bundles, and perceived value. This creates margin pressure, especially when raw material, packaging, labor, electricity, fuel, and distribution costs increase. For large companies, scale helps reduce cost per unit. For SMEs, cost pressure is more difficult because they may buy raw materials in smaller quantities, use third-party freezing or storage, and rely on manual production. If SMEs raise prices too much, consumers may switch to larger brands. If they keep prices too low, margins can become unsustainable. The challenge for brands is to maintain affordability without reducing quality. This is difficult because frozen food consumers want convenience, taste, safety, and low price at the same time.

6.4 Halal, Food Safety, and Regulatory Compliance

Regulation is a major barrier and also a trust-building requirement. Frozen food often contains meat, poultry, seafood, seasoning, additives, sauces, and processed ingredients. This makes halal certification and food safety compliance highly important. Indonesia’s halal certification obligation officially began applying to products entering, circulating, and traded in Indonesia starting October 18, 2024, according to BPJPH. BPJPH also stated that non-compliant products may face administrative sanctions such as written warnings or product withdrawal from circulation. Reuters reported that Indonesian authorities planned inspections of grocery shelves as the halal-label deadline approached, while some importers and restaurants faced challenges because of complex supply chains and unclear guidelines. Food labeling is also becoming stricter. Reuters reported in 2025 that Indonesia would give food and beverage companies a two-year period to comply with new labeling rules for products high in salt, sugar, and fat, with traffic-light labeling expected to become mandatory by the end of 2027. Reuters later reported in 2026 that Indonesia had mandated color-graded labels within two years under a new Health Ministry decree.

Compliance increases operating burden, especially for SMEs. However, it also creates a competitive advantage because certified and properly labeled products are more trusted by consumers, retailers, and institutional buyers.

6.5 Raw Material and Import Dependency

Indonesia has strong local production capacity in poultry and seafood but still depends on imports for several frozen-food-related categories. Beef, buffalo meat, frozen potatoes, specialty meat products, premium seafood, dairy-based ingredients, and some bakery inputs are often imported. This dependency creates exposure to exchange rates, import quotas, international supply disruptions, shipping cost, tariffs, and regulatory changes. For example, the foodservice sector’s frozen French fries category depends heavily on imported processed potato products because large-scale domestic processing capacity remains limited. Meat-based frozen food producers may also rely on imported beef or buffalo meat depending on product formulation and pricing. When import costs rise, producers face a difficult choice: raise prices, reduce margins, reformulate products, or adjust pack sizes. Import dependency does not mean the industry is weak. It means companies must manage sourcing strategy carefully. Businesses that diversify suppliers and increase local sourcing where possible will be more resilient.

6.6 Competitive Pressure and Market Fragmentation

The frozen food industry is becoming more crowded. Large companies dominate poultry-based frozen food, while SMEs compete aggressively in snacks, dim sum, ready meals, and local frozen products. Large players compete through scale, brand trust, retail access, and price architecture. SMEs compete through local taste, community selling, flexibility, and social commerce. This creates highly competitive pressure across price tiers. The main challenge is commoditization. Many products look similar: nuggets, sausages, meatballs, dim sum, risoles, kebab, and cireng. When differentiation is weak, consumers compare mainly on price. This can reduce margins and make long-term brand building difficult. The companies that win will be those that combine differentiation with operational reliability. Taste alone is not enough if the brand cannot deliver consistently.

6.7 SME Barriers

SMEs are important to the frozen food industry, especially in frozen snacks, dim sum, local meals, and social commerce. However, SMEs face many barriers when trying to scale. Common SME barriers include limited production capacity, inconsistent quality, weak packaging, lack of halal certification, limited cold storage, manual operations, unclear shelf-life testing, and dependence on resellers. A 2025 study on Indonesian frozen food MSMEs found that halal certification was positively associated with better financial performance, indicating that certification can strengthen business credibility and market performance. This is important because many SME frozen food brands still treat certification as a cost, while in practice it can become a growth enabler. SMEs can grow, but they need to professionalize. The most important upgrades are certification, packaging, production standardization, freezer management, and reseller governance.

6.8 Consumer Trust and Product Perception

Consumer trust is a major barrier because frozen food often faces perception issues. Some consumers still associate frozen food with preservatives, high sodium, artificial ingredients, or lower freshness compared with fresh food. This perception is not always accurate, because freezing itself is a preservation method that can maintain food quality when managed properly. However, perception still matters. Brands must educate consumers on storage, cooking method, ingredients, halal status, and food safety. Product perception is especially important for ready meals and processed meat. Consumers may question nutrition, sodium, fat content, and ingredient quality. With Indonesia moving toward clearer nutrition labeling, frozen food companies may need to reformulate or improve transparency, especially for products high in salt, sugar, or fat. Trust is not built only through advertising. It is built through consistent product quality, clear labeling, safe delivery, and repeat customer experience.

6.9 Summary of Potential Challenges and Barriers

The barriers in Indonesia’s frozen food industry can be grouped into operational, regulatory, financial, competitive, and consumer-related challenges.

Summary of Industry Challenges and Barriers

6.10 Chapter Conclusion

Indonesia’s frozen food industry has strong growth potential, but the path to scale is challenging. The industry is not only product-driven; it is infrastructure-driven, compliance-driven, and trust-driven. The biggest barrier is cold-chain reliability. Without proper freezing, storage, transportation, and last-mile delivery, even a good product can fail. The second major barrier is cost pressure, because frozen logistics and production require more expensive infrastructure than dry packaged food. The third barrier is compliance, especially halal certification, food safety, and nutrition labeling. These requirements increase complexity, but they also create trust and support long-term market development. For large companies, the main challenge is maintaining scale, affordability, and distribution efficiency. For SMEs, the main challenge is professionalization. They must improve certification, packaging, production consistency, and storage discipline if they want to move beyond local reseller networks. The main conclusion from Chapter 6 is that future winners in Indonesia’s frozen food industry will not be determined only by taste or price. They will be determined by the ability to combine product quality, cold-chain reliability, regulatory compliance, consumer trust, and cost efficiency.

Chapter 7: Benchmark and Common Practices

7.1 Overview

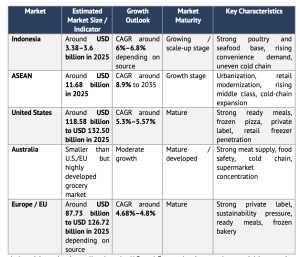

Indonesia’s frozen food industry is growing, but its level of maturity is still different from several regional and global markets. Compared with ASEAN peers, Indonesia has one of the largest domestic demand bases because of its population size, urbanization, and expanding middle class. Compared with the United States and the European Union, Indonesia is still developing in terms of freezer penetration, ready-meal variety, cold-chain maturity, private-label strength, and premium frozen food innovation. Compared with Australia, Indonesia has a larger domestic consumer base but weaker cold-chain coverage and higher geographic complexity.

In 2025, Indonesia’s frozen food market was estimated at around USD 3.38 billion to USD 3.6 billion, while the ASEAN market was estimated at about USD 11.68 billion, the U.S. market at above USD 118 billion to USD 132 billion, and Europe at more than USD 87 billion to USD 126 billion, depending on the research source and market definition. These figures show that Indonesia is already significant within Southeast Asia, but still far smaller than mature Western frozen food markets.

The purpose of this chapter is to benchmark Indonesia against four comparison groups:

- ASEAN, representing regional emerging-market peers.

- United States, representing a mature, high-consumption frozen food market.

- Australia, representing a developed market with strong cold-chain, protein, and retail systems.

- European Union / Europe, representing a mature and regulation-driven market with strong private-label and ready-meal development.

The benchmark is not intended to show that Indonesia should copy every market. Instead, it identifies what Indonesia can learn from each region and where Indonesia has its own structural advantages.

7.2 Benchmark Summary

Indonesia’s frozen food industry is in a growth stage. ASEAN as a region is also growing, especially because of urbanization, modern retail expansion, rising disposable income, and changing consumer lifestyles. The U.S. and Europe are more mature, with strong frozen ready-meal categories, private-label penetration, advanced cold-chain systems, and strong retail freezer infrastructure. Australia is smaller in population but more developed in cold-chain systems, food safety standards, meat supply, and modern grocery penetration.

Frozen Food Market Benchmark

Indonesia’s market is smaller than the U.S. and Europe, but its growth potential is attractive because frozen food penetration is still developing. Compared with mature markets, Indonesia has more room to grow in ready meals, frozen bakery, frozen vegetables, premium seafood, healthy frozen food, and modern distribution. Indonesia’s benchmark position can be summarized as follows: large potential, strong local protein base, strong halal relevance, but weaker logistics maturity compared with developed markets.

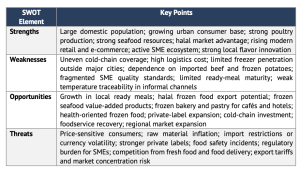

7.8 SWOT Analysis of Indonesia’s Frozen Food Industry

SWOT Analysis

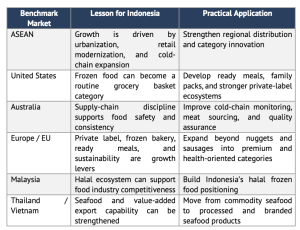

7.9 Strategic Lessons from Benchmark Markets

Indonesia does not need to copy the U.S., Australia, or Europe exactly. However, several lessons are relevant.

Strategic Lessons for Indonesia

The most important lesson is that frozen food industry maturity depends on infrastructure and trust. Mature markets do not grow only because consumers like frozen food. They grow because consumers trust that the product will be safe, available, high quality, and convenient.

7.10 Chapter Conclusion

Compared with ASEAN, the United States, Australia, and Europe, Indonesia’s frozen food industry is still in a growth and scale-up stage. The market is large within Southeast Asia, but still far smaller and less mature than the United States and Europe. Indonesia’s key strengths are its large domestic population, strong poultry production, seafood resources, halal relevance, and active SME ecosystem. However, Indonesia still faces major gaps in cold-chain infrastructure, freezer penetration, product maturity, ready-meal development, SME standardization, and import dependency for selected categories. Mature markets show that frozen food can grow into a broad category beyond nuggets and sausages, including ready meals, frozen vegetables, bakery, premium seafood, healthy meals, and private-label products.

The strategic conclusion from Chapter 7 is that Indonesia has strong growth potential, but it must move from a basic frozen food market into a more mature frozen food ecosystem. This means improving cold-chain reliability, expanding product innovation, building halal and food safety trust, strengthening value-added seafood exports, and developing local ready meals suited to Indonesian taste and price expectations.

Chapter 8: Writer’s Opinion

Chapter 8 — Writer’s Opinion

8.1 Overview

In the writer’s opinion, Indonesia’s frozen food industry is entering a decisive transition period. The industry is no longer merely a convenience-food category driven by nuggets, sausages, and household emergency stock. It is gradually becoming a strategic food ecosystem that connects consumer lifestyle, food manufacturing, cold-chain infrastructure, halal assurance, seafood exports, retail modernization, and digital commerce. The period between 2020 and 2025 was important because it changed the way consumers perceived frozen food. The pandemic accelerated trial, but the post-pandemic period proved that demand did not disappear. Consumers continued buying frozen food because it solved practical problems: limited time, meal planning, children’s food, foodservice efficiency, and affordable convenience.

However, the next stage of the industry will be more difficult. The easy growth phase has already passed. When a category is still new, demand can grow simply because more people try the product. But when the market becomes more crowded, the winners are no longer determined only by who enters first or who has the lowest price. The winners are determined by who can build the strongest system.

For frozen food, that system includes production capacity, product consistency, halal and food safety compliance, cold storage, refrigerated distribution, retail freezer access, online delivery capability, and consumer trust. This is why frozen food should not be understood only as a product business. It is a full value-chain business.

The writer’s main view is that Indonesia has strong potential to become one of the most important frozen food markets in Southeast Asia. The country has a large population, growing urban consumption, strong poultry production, seafood resources, and increasing digital commerce adoption. However, Indonesia still needs to improve cold-chain infrastructure, product diversification, SME standardization, and value-added processing before the industry can reach its full potential.

8.2 Frozen Food Is Becoming a Structural Consumer Category

The first important point is that frozen food in Indonesia should no longer be viewed as a temporary pandemic trend. The pandemic only accelerated consumer education. It introduced many households to the habit of storing frozen products at home, but the reason they continued buying after mobility returned is because frozen food solves a permanent lifestyle problem.

Modern urban life creates time scarcity. Many consumers have less time to cook from raw ingredients every day. Working parents need quick food options for children. Students and young professionals need practical meals. Small households do not always want to cook large portions. Foodservice operators need consistent ingredients that reduce preparation time.

Frozen food fits these needs because it combines convenience, shelf life, portion flexibility, and predictable taste. It allows consumers to reduce preparation time without fully depending on food delivery. It also allows households to keep backup meals without worrying about short expiry periods.

This is important because it changes the role of frozen food. In the past, frozen food was often treated as an occasional snack or emergency stock. Going forward, it can become part of routine household planning. This shift from occasional purchase to routine consumption is the foundation of long-term category growth.

The opportunity is especially strong in urban and semi-urban areas. In these markets, consumers have better access to freezers, modern retail, delivery services, digital payments, and online grocery. These conditions make frozen food easier to buy, store, and consume. However, the next challenge is expanding this behavior beyond large cities and into secondary cities with weaker cold-chain infrastructure.

8.3 The Real Competition Is Not Only Product vs Product, but System vs System

Many people think frozen food competition is mainly about taste, packaging, and price. Those factors matter, but they are not enough. In the writer’s opinion, the real competition in the frozen food industry is system versus system.

A frozen food brand can have an excellent recipe, but if the product thaws during delivery, the customer experience fails. A brand can have good packaging, but if it cannot secure freezer space in retail, consumers may never see the product. A brand can have strong online demand, but if last-mile delivery is unreliable, repeat purchases will be weak. A company can have low prices, but if cold-chain costs are not controlled, margins will collapse.

This is why large integrated players have strong advantages. Companies such as Charoen Pokphand, Japfa, Belfoods/Sreeya Sewu, Kanzler/Cimory, and Sekar Bumi do not compete only through products. They compete through manufacturing scale, raw material access, certification, distribution networks, sales teams, retail relationships, cold storage, and brand trust.

For SMEs, this creates both opportunity and risk. SMEs can innovate faster and respond to local tastes more quickly than large companies. They can launch dim sum, risoles, kebab, cireng, frozen sambal meals, regional dishes, or niche ready meals with strong community appeal. However, when they try to scale, they will face the same operational requirements as larger players: consistent production, certification, packaging, cold storage, shelf-life management, reseller governance, and delivery discipline. This is why many frozen food SMEs grow quickly in the beginning but struggle to expand beyond their local market. The problem is not always demand. The problem is the system behind the demand.

8.4 Cold Chain Will Become the Industry’s Most Important Competitive Barrier

Cold chain is the most important structural issue in Indonesia’s frozen food industry. In the writer’s opinion, cold-chain capability will determine which companies can scale nationally and which companies remain local. Frozen food is highly sensitive to temperature.

If a product is not handled properly, quality can decline even before the consumer opens the package. Thawing and refreezing can affect texture, taste, safety, and shelf life. This makes cold-chain reliability part of the product promise.

Indonesia’s cold-chain challenge is not simply about having freezers. It is about maintaining temperature control across the entire journey: production, blast freezing, cold storage, loading, transportation, distributor warehouse, retail display, reseller freezer, last-mile delivery, and consumer storage.

This is particularly difficult in Indonesia because of geography. Distribution inside Java is already challenging because of traffic, density, and retail competition. Distribution outside Java is more complex because it may involve sea freight, ports, regional warehouses, local distributors, and longer lead times. For eastern Indonesia, logistics cost and cold-chain availability can become major barriers.

Therefore, cold-chain infrastructure is not only an operational issue. It is a market access issue. Brands that can maintain cold-chain integrity can enter more cities and regions. Brands that cannot will be limited to local delivery or selected urban markets.

The strategic implication is clear: frozen food companies must treat logistics as a core investment, not as an afterthought. This includes choosing reliable third-party logistics providers, building regional stock points, training distributors, setting strict delivery radius rules, using proper insulated packaging, and monitoring product condition.

8.5 Large Players Will Dominate Core Categories, While SMEs Will Create Category Diversity

Indonesia’s frozen food market will likely develop in two parallel directions.

- First, large players will continue to dominate core mass-market categories. Products such as nuggets, sausages, processed chicken, breaded chicken, and branded meatballs require large-scale production, strong procurement, quality control, halal certification, and national distribution. These are areas where large companies have natural advantages. Charoen Pokphand, for example, benefits from its integrated poultry supply chain and strong processed chicken brands such as Fiesta, Champ, Okey, and Akumo. Japfa benefits from its poultry ecosystem and brands such as So Good and So Nice. Belfoods competes strongly in affordable family frozen food. Kanzler has built a premium position in sausages and processed meat. These companies are difficult to challenge directly because they have scale and trust.

- Second, SMEs will continue to create product diversity. This is where Indonesia’s frozen food market becomes interesting. Local SMEs can create products that large companies may not immediately prioritize regional snacks, homemade-style dim sum, local ready meals, premium frozen sambal dishes, niche protein products, and community-based frozen food.

8.6 Ready Meals Are the Next Major Growth Opportunity

The writer believes that frozen ready meals are one of the most promising categories for Indonesia’s next frozen food growth phase. Today, Indonesia’s frozen food market is still strongly associated with side dishes and snacks. Consumers buy nuggets, sausages, meatballs, dim sum, fries, seafood, and frozen snacks. These products are useful, but they do not always solve the full meal problem.

Frozen ready meals can solve a bigger problem: “What can I eat quickly without cooking from scratch and without ordering delivery?”

This is a powerful opportunity because Indonesia has a rich food culture. Many local dishes can potentially be adapted into frozen formats, such as nasi goreng, ayam geprek, rendang rice, rice bowls, satay-style meals, mie goreng, soto components, sambal chicken, and regional dishes. If brands can produce these meals with good taste, proper texture after reheating, affordable pricing, and convenient packaging, frozen ready meals can become a major growth category.

However, ready meals are not easy to execute. A nugget only needs to maintain texture and taste after frying or air frying. A ready meal must maintain rice texture, sauce consistency, protein quality, aroma, portion balance, and reheating performance. Packaging must work for microwave or steaming. The product must look appetizing after reheating. The price must still compete with food delivery, warung meals, and instant food.

This means the ready-meal opportunity is large, but it requires stronger R&D than basic frozen snacks. Brands that can solve this will move the industry beyond basic processed meat into higher-value meal solutions.

8.7 Halal and Food Safety Are Not Just Compliance, but Trust Infrastructure

In Indonesia, halal and food safety should be treated as strategic brand assets. They are not merely administrative requirements. Frozen food often contains meat, poultry, seafood, seasoning, sauces, additives, and processed ingredients. Consumers want assurance that these products are halal, safe, properly labeled, and handled correctly. This is especially important because frozen food quality depends on processes that consumers cannot directly observe.