Chapter 1: Preface

1.1 Background of the Report

Indonesia’s medical device industry is entering an important stage of development. For many years, Indonesia has been known as a large healthcare market that depends heavily on imported medical devices. Hospitals, clinics, laboratories, and healthcare providers across the country have relied on foreign products for many categories, especially advanced diagnostic equipment, surgical instruments, imaging systems, laboratory devices, and high-technology medical equipment.

However, the situation has started to change. The COVID-19 pandemic showed how vulnerable the healthcare system can be when the supply of medical devices depends too much on imports. During the pandemic, demand for masks, personal protective equipment, diagnostic tools, oxygen-related equipment, ventilators, and other essential medical products increased sharply. At the same time, global supply chains were disrupted. This experience encouraged Indonesia to strengthen its domestic medical device industry and reduce dependency on imported products.

As Indonesia enters 2026, the medical device sector is no longer viewed only as a healthcare-supporting industry. It has become part of a broader national agenda involving healthcare resilience, industrial development, investment, technology transfer, and public health security.

1.2 Importance of the Medical Device Industry in Indonesia

Medical devices play a critical role in improving healthcare quality. They support diagnosis, treatment, monitoring, surgery, rehabilitation, emergency response, and hospital operations. Without reliable medical devices, healthcare facilities cannot deliver effective services. In Indonesia, the importance of medical devices continues to increase due to several factors.

The population is large, healthcare access is expanding, hospitals continue to develop, and public awareness of health services is rising. The national health insurance program has also encouraged more people to access healthcare facilities, creating greater demand for medical equipment and consumable products.

At the same time, Indonesia’s geography creates a unique challenge. As an archipelagic country, Indonesia must distribute medical devices across many islands and regions with different levels of infrastructure. This makes the industry more complex than in countries with more centralized geography. Medical device companies must not only sell products but also ensure logistics, after-sales service, spare parts availability, maintenance, calibration, and regulatory compliance.

1.3 Market Transformation After the Pandemic

The period from 2020 to 2025 was a dynamic period for Indonesia’s medical device market. The market expanded rapidly during the pandemic because of emergency healthcare demand. After the peak of the pandemic, demand for certain products declined, especially pandemic-related items such as personal protective equipment and testing products. However, demand for broader healthcare equipment continued to grow as hospitals returned to normal operations and resumed investment in medical infrastructure.

This market movement shows that Indonesia’s medical device sector cannot be analyzed only from short-term demand. The industry must be understood through several key factors, including public procurement, private hospital investment, import dependency, local production capacity, regulatory requirements, and distribution capability.

The post-pandemic period also created a stronger policy push toward domestic production. The government began encouraging local manufacturing through procurement preference, local content requirements, and support for domestic medical device producers. This shift created new opportunities for local companies while also changing the competitive landscape for importers and multinational manufacturers.

1.4 Government Role and Policy Direction

The Indonesian government has a major influence on the medical device industry. Medical devices are highly regulated products because they are directly related to patient safety and healthcare quality. Therefore, government policy affects product registration, distribution permits, procurement mechanisms, local content requirements, quality standards, and post-market supervision.

One of the most important policy directions is the encouragement of domestic production through TKDN, or domestic component level requirements. This policy aims to increase the use of locally produced medical devices, especially in public procurement. The government wants hospitals and healthcare institutions to use domestic products when suitable alternatives are available.

This policy direction creates opportunities for local manufacturers to grow. It also encourages foreign companies to consider local assembly, partnerships, joint ventures, or technology transfer. However, the policy also creates challenges, especially for advanced medical devices that are not yet produced locally. In some product categories, Indonesia still depends heavily on imported technology.

1.5 Industry Opportunity and Business Relevance

Indonesia offers strong long-term potential for medical device companies. The country has a large population, expanding healthcare access, growing private hospital investment, and increasing demand for better medical services. These factors create opportunities for manufacturers, distributors, investors, and technology providers.

The market opportunity is not limited to large hospitals in major cities. Demand also comes from regional hospitals, clinics, laboratories, primary healthcare facilities, and government health programs. Basic consumables, diagnostic products, hospital furniture, monitoring devices, surgical equipment, and laboratory tools all have room for growth.

However, companies entering Indonesia must understand that the market is not simple. Price sensitivity remains high, especially in public procurement. Regulations can be complex. Distribution requires strong local networks. After-sales service is essential. For advanced equipment, buyers also consider training, maintenance, spare parts, warranty, and long-term reliability.

Therefore, success in Indonesia requires more than product availability. It requires market understanding, regulatory readiness, distribution strength, technical support, and the ability to adapt to local procurement conditions.

1.6 Indonesia’s Position in the Global and Regional Context

Indonesia has a large domestic market, but its medical device manufacturing capability is still developing. Compared with some ASEAN countries, Indonesia has strong demand potential but still needs to improve production sophistication, export competitiveness, supply-chain depth, and technology capability.

Singapore is stronger as a regional hub for multinational medical technology companies. Malaysia and Thailand have stronger manufacturing positions in certain categories, especially consumables and healthcare manufacturing. Vietnam is becoming increasingly attractive as a manufacturing base due to competitive costs and industrial growth.

Compared with the European Union and the United States, Indonesia remains at an earlier stage of medical technology development. The EU and the USA have more advanced regulatory systems, stronger research and development ecosystems, higher innovation capacity, and globally recognized medical device companies. However, Indonesia’s large domestic demand gives it an opportunity to build industrial capability gradually.

1.7 Purpose of the Report

The purpose of this report is to provide a clear and strategic understanding of Indonesia’s medical device industry as it enters 2026. The report is intended for readers who need a structured view of the market, including business owners, investors, distributors, manufacturers, healthcare operators, policymakers, and strategic partners.

This report does not only describe the market. It also explains the forces shaping the industry, including healthcare demand, government policy, import dependency, local production development, distribution challenges, and global competition. By understanding these factors, readers can better evaluate the opportunities and risks in Indonesia’s medical device sector.

1.9 Key Perspective of the Report

The main perspective of this report is that Indonesia’s medical device industry is promising but still developing. The country has strong demand, but domestic production capability remains uneven. Local producers are growing, especially in basic and medium-complexity products, but Indonesia still relies on imports for many advanced technologies. The future of the industry will depend on how well Indonesia can balance three priorities: improving healthcare access, strengthening domestic manufacturing, and maintaining access to high-quality global medical technology.

If Indonesia can improve regulatory clarity, support local innovation, attract investment, and build stronger production capability, the country has the potential to become not only a major medical device market but also a more competitive production base in Southeast Asia.

Chapter 2: Market Trends and Size of Medical Devices Industry in Indonesia

2.1 Overview of Indonesia’s Medical Device Market

Indonesia is one of the most important medical device markets in Southeast Asia. The country has a large population, an expanding healthcare system, increasing public and private hospital demand, and a government agenda that encourages better healthcare access across regions. These factors create a strong long-term foundation for the medical device industry.

However, the market has not grown in a simple upward pattern. From 2020 to 2025, Indonesia’s medical device market moved through three different phases. The first phase was the pandemic-driven expansion in 2020 and 2021. The second phase was the post-pandemic correction in 2022. The third phase was the recovery and restructuring period from 2023 to 2025.

This movement shows that Indonesia’s medical device market is influenced by both healthcare demand and policy direction. The market is not only shaped by hospitals buying equipment. It is also shaped by emergency demand, import dependency, local production policy, government procurement, currency movement, hospital investment cycles, and the ability of local producers to replace certain imported products. By 2026, Indonesia’s medical device market can be described as a recovering and transitioning market. It is recovering because demand is returning after the sharp post-pandemic decline. It is transitioning because the government is pushing the industry toward stronger local production and lower dependency on imported products.

2.2 Market Size Development from 2020 to 2025

The Indonesian medical device market reached USD 3.367 billion in 2020 and increased to USD 3.586 billion in 2021. This was the highest point during the observed period. The increase was strongly influenced by pandemic-related healthcare demand, including diagnostic products, personal protective equipment, respiratory support devices, and other urgent medical supplies.

In 2022, the market declined sharply to USD 1.814 billion. This decline reflected the normalization of pandemic-related demand and the adjustment of procurement activity after the emergency period. Many products that experienced exceptional demand during the pandemic no longer had the same level of purchasing urgency. After 2022, the market began to recover. In 2023, the market increased to USD 2.428 billion. In 2024, it rose further to USD 2.987 billion. In 2025, the market was estimated at USD 2.779 billion. Although the 2025 estimate was lower than 2024, it still showed that the market remained significantly above the 2022 correction point.

The market trend shows that Indonesia experienced a sharp pandemic peak, followed by a deep correction, and then a recovery phase. The decline in 2022 should not be interpreted as a collapse in healthcare demand. Rather, it reflected the end of extraordinary pandemic procurement and a shift back toward more normal purchasing behavior.

The most important point is that Indonesia’s medical device market remained large even after the pandemic correction. A market size of approximately USD 2.779 billion in 2025 still represents a major opportunity in Southeast Asia, especially considering Indonesia’s population, healthcare expansion, and government investment in medical infrastructure.

2.3 Market Trend by Phase

2.3.1 Pandemic Expansion: 2020–2021

The years 2020 and 2021 were extraordinary years for the medical device sector. During this period, demand increased rapidly because healthcare providers needed urgent supplies to respond to COVID-19. Hospitals required more personal protective equipment, oxygen-related products, ventilators, testing equipment, diagnostic reagents, patient monitoring devices, and infection-control products.

This period exposed the importance of medical devices as part of national healthcare security. Products that were previously treated as normal procurement items became strategic necessities. Supply availability, import access, logistics, and local production capacity became national concerns. The market reached USD 3.586 billion in 2021, the highest figure in the 2020–2025 period. This peak reflected not only normal healthcare demand but also emergency purchasing and pandemic-related stock building.

2.3.2 Post-Pandemic Correction: 2022

In 2022, the market declined to USD 1.814 billion. This was the sharpest movement in the observed period. The correction happened because emergency demand began to normalize. Hospitals and government agencies no longer purchased pandemic-related products at the same volume as during the crisis.

Some product categories that grew aggressively during the pandemic experienced lower demand after the emergency phase. This included several categories related to testing, personal protective equipment, and respiratory support. At the same time, healthcare institutions became more selective in procurement as budgets shifted from emergency response to regular healthcare services.

This correction was also a reminder that market size during a crisis can be temporary. A high pandemic-year market value should not be used as the only basis for long-term market projections. The more reliable approach is to analyze the market after emergency demand has normalized.

2.3.3 Recovery and Restructuring: 2023–2025

From 2023 onward, Indonesia’s medical device market entered a recovery stage. The market increased from USD 1.814 billion in 2022 to USD 2.428 billion in 2023, then to USD 2.987 billion in 2024. This recovery was supported by the return of hospital operations, continued healthcare infrastructure development, and broader demand for medical services.

However, the recovery was not only about demand returning. It was also about market restructuring. The government continued to push domestic medical device production through local content policy and procurement preference. This changed the way producers, importers, and distributors approached the market.

Companies that previously relied mainly on imported products started facing stronger pressure to consider local partnerships, local assembly, technology transfer, or domestic sourcing. Meanwhile, local producers gained more opportunity to serve public procurement, especially in product categories where domestic alternatives were available.

The 2025 estimate of USD 2.779 billion suggests that the market remained in a recovery position but had not returned to the 2021 pandemic peak. This is reasonable because the 2021 figure was influenced by extraordinary demand. The more important trend is that the market after 2022 showed renewed strength and continued relevance.

2.4 Local Production Trend

Local production is one of the most important trends in Indonesia’s medical device industry. From 2020 to 2025, local production increased consistently. It rose from USD 2.119 billion in 2020 to an estimated USD 3.373 billion in 2025.

This trend is significant because it shows that local production continued to grow even when total market size declined in 2022. In other words, domestic production did not simply follow short-term market demand. It was also supported by policy direction, industrial development, and the government’s ambition to strengthen medical device independence.

The growth of local production indicates that Indonesia is gradually building stronger domestic capability, especially in selected product categories. Local manufacturers have become more relevant in basic medical consumables, hospital furniture, personal protective equipment, simple diagnostic tools, and selected medium-complexity products.

However, the increase in local production should be interpreted carefully. A larger production value does not automatically mean Indonesia has mastered advanced medical technology. Much of the local production base is still concentrated in lower-complexity or medium-complexity products. Advanced imaging, high-end surgical systems, sophisticated laboratory automation, radiation therapy equipment, and other high-technology products remain heavily dependent on imports.

Therefore, Indonesia’s local production trend is positive, but the next challenge is upgrading product sophistication. The country needs to move from basic manufacturing toward higher-value production, stronger engineering capability, quality assurance, clinical validation, and export competitiveness.

2.5 Import Trend and Market Dependency

Imports remain a major part of Indonesia’s medical device market. In 2020, total imports reached USD 2.564 billion. In 2021, imports increased slightly to USD 2.633 billion. After the pandemic peak, imports declined to USD 1.974 billion in 2022 and USD 1.778 billion in 2023. Imports then remained relatively stable at USD 1.786 billion in 2024 and were estimated to increase to USD 1.908 billion in 2025.

The import trend highlights two key points. Indonesia continues to depend on imported medical devices, particularly advanced products, while post-pandemic import growth has become more selective. Import levels have not returned to the highs of 2020–2021, partly because pandemic-driven demand has eased and domestic production policies have strengthened.

For foreign manufacturers, this means Indonesia remains attractive, but the market entry strategy must be adapted. Imported products are still needed, especially for high-end technology, but companies must be prepared for local content pressure, product registration requirements, distributor selection, after-sales expectations, and public procurement rules.

The best opportunities for imported products are likely to remain in advanced diagnostic imaging, in-vitro diagnostics, surgical technology, intensive care equipment, patient monitoring, laboratory automation, and digital health-related devices. These segments require higher technology, stronger clinical performance, and advanced technical support.

2.6 Export Trend and Industrial Potential

Indonesia’s medical device exports also changed significantly from 2020 to 2025. Exports reached USD 1.011 billion in 2020 and increased to USD 1.377 billion in 2021. In 2022, exports rose sharply to USD 2.724 billion, before declining to USD 2.158 billion in 2023 and USD 1.873 billion in 2024. In 2025, exports were estimated to increase again to USD 2.501 billion.

The export trend shows that Indonesia has some capability to participate in international medical device trade. However, the pattern is volatile. The sharp export increase in 2022 suggests that certain product categories experienced exceptional international demand, but the decline in 2023 and 2024 indicates that sustaining export momentum is not easy.

To become a stronger exporter, Indonesia must improve consistency, quality certification, product competitiveness, production scale, and international market access. Export success requires more than local production volume. It requires compliance with international standards, strong documentation, product reliability, brand trust, and competitive pricing.

Indonesia’s export potential is real, but it is still developing. The country may have better short- to medium-term export opportunities in consumables, hospital furniture, basic medical equipment, selected diagnostic products, and contract manufacturing. For advanced devices, Indonesia still needs deeper technology capability and stronger R&D support.

2.7 Apparent Market Structure

The apparent market size is calculated by adding local production and imports, then subtracting exports. This formula helps estimate the value of products available for domestic use. This is important for interpretation. A lower market size does not always mean the industry is weaker. It may also mean that more production is being exported. Therefore, market size must be read together with production, import, and export data.

From a strategic perspective, Indonesia’s market is moving toward a more balanced structure, but it is not yet fully independent. Domestic production is growing, but imports remain essential for advanced technology. Exports show potential, but the country still needs stronger competitiveness to become a regional medical device manufacturing hub.

2.8 Demand Drivers

Several demand drivers support the long-term growth of Indonesia’s medical device market.

- The first driver is population size. Indonesia has one of the largest populations in the world, creating broad demand for healthcare services. A large population increases the need for hospitals, clinics, laboratories, diagnostic services, maternal and child healthcare, chronic disease management, and emergency care.

- The second driver is healthcare access expansion. The national health insurance system has increased the number of people accessing formal healthcare services. As more patients use hospitals and clinics, demand for medical equipment and consumables also increases.

- The third driver is hospital development. Indonesia continues to need more healthcare infrastructure, especially outside major cities. Public hospitals require modernization, while private hospitals invest in better facilities and advanced medical services to compete for patients.

- The fourth driver is disease burden. Chronic diseases such as diabetes, cardiovascular disease, kidney disease, cancer, and respiratory illness require long-term diagnosis, monitoring, and treatment. This creates demand for diagnostic devices, imaging equipment, laboratory tests, dialysis equipment, patient monitoring, and surgical technologies.

- The fifth driver is technology adoption. Hospitals are increasingly expected to improve efficiency, accuracy, and patient experience. This supports demand for digital health tools, connected devices, laboratory automation, telemedicine support equipment, electronic medical record integration, and data-enabled diagnostics.

- The sixth driver is government investment. Public healthcare programs, hospital upgrades, and national procurement initiatives can create large demand for medical devices. Government purchasing is especially important for products used in public hospitals, primary care facilities, laboratories, and regional healthcare programs.

2.9 Key Market Segments

The Indonesian medical device market can be divided into several important segments.

- The first segment is consumables and disposable products. This includes syringes, gloves, masks, wound care products, catheters, infusion sets, and other frequently used medical supplies. This segment is large because hospitals and clinics use these products continuously.

- The second segment is diagnostic and laboratory products. This includes in-vitro diagnostics, laboratory reagents, analyzers, rapid test kits, and supporting laboratory equipment. Demand is supported by disease screening, hospital laboratories, public health programs, and private diagnostic service providers.

- The third segment is hospital equipment and furniture. This includes hospital beds, examination tables, operating tables, wheelchairs, trolleys, lamps, and other facility-related products. This segment is more accessible for local producers compared with high-technology equipment.

- The fourth segment is electromedical and monitoring equipment. This includes patient monitors, ECG machines, defibrillators, ventilators, infusion pumps, and other electronic medical devices. Some products in this segment can be assembled or produced locally, but many still depend on imported components or foreign technology.

- The fifth segment is diagnostic imaging. This includes ultrasound, X-ray, CT scan, MRI, mammography, and related imaging systems. This segment is dominated by advanced technology and remains highly dependent on international producers.

- The sixth segment is surgical and specialist equipment. This includes surgical instruments, operating room technology, endoscopy systems, implants, orthopedic devices, and specialist treatment devices. Demand is supported by hospital specialization and the expansion of advanced medical services.

- The seventh segment is digital and connected medical devices. This includes remote monitoring devices, wearable health devices, telemedicine-related equipment, connected diagnostic tools, and devices integrated with health information systems. This segment is still developing but has strong future potential.

2.10 Public and Private Market Dynamics

Indonesia’s medical device demand comes from both public and private healthcare providers. These two markets have different characteristics. The public market is influenced by government procurement, budget allocation, e-catalogue listing, local content requirements, and national healthcare priorities. Public hospitals and government health facilities are more likely to prioritize products that comply with procurement rules and local content policies.

The private market is more flexible but also competitive. Private hospitals often consider product performance, brand reputation, clinical outcomes, patient experience, financing options, service support, and technology differentiation. Premium private hospitals may be more willing to purchase imported high-end equipment, especially when it supports specialist services or strengthens hospital branding.

This creates a two-layer market. The public sector creates volume and policy-driven demand, while the private sector creates demand for higher-value and more advanced technologies. Companies that understand both segments can design better market strategies.

For example, a local producer of hospital beds or basic consumables may find stronger opportunities in public procurement. Meanwhile, a multinational producer of MRI systems, robotic surgery equipment, or advanced laboratory automation may focus more on premium hospitals, specialist centers, and selected public procurement packages that require high-end technology.

2.11 Market Outlook Toward 2026

The outlook for Indonesia’s medical device market toward 2026 is positive, but selective. Demand will continue to exist because healthcare services are essential. Hospital modernization, diagnostic expansion, population health needs, and government healthcare programs will continue to support the industry.

However, growth will not be evenly distributed across all product categories. Basic products may face stronger price competition and local production pressure. Advanced products may continue to rely on imports but will require stronger compliance, local partnerships, and service support. Digital health-related devices may grow as healthcare providers adopt more connected systems.

The market is also likely to become more policy sensitive. Local content rules, procurement preference, and domestic production programs will influence purchasing decisions, especially in the public sector. Companies that ignore this policy trends may face difficulty competing in government procurement.

At the same time, Indonesia still needs imported advanced technology. This creates room for foreign companies that can offer high-quality products, clinical reliability, training, after-sales support, and partnership models that align with Indonesia’s industrial goals.

Overall, the market outlook can be summarized as follows: Indonesia’s medical device market is no longer only an import-driven opportunity. It is becoming a more regulated, more strategic, and more locally oriented market. The winners will be companies that combine product quality with regulatory readiness, distribution strength, local partnership, and long-term commitment.

Chapter 3: Major Producers in Indonesia

3.1 Overview of Medical Device Production in Indonesia

Indonesia’s medical device production sector has grown significantly over the last several years. The industry was once viewed mainly as a supporting sector with limited domestic capability, but it is now becoming part of Indonesia’s national healthcare resilience strategy. The government wants the country to reduce dependence on imported medical devices, improve local manufacturing capability, and encourage more advanced production within the country.

The development of local production became more urgent after the COVID-19 pandemic. During the pandemic, Indonesia experienced high demand for masks, personal protective equipment, diagnostic tools, syringes, ventilators, oxygen-related equipment, and hospital supplies. This situation showed that domestic production capacity is not only a business matter, but also a matter of national health security.

By 2026, Indonesia’s medical device producers can be divided into several groups. The first group consists of producers of basic consumables and disposable products. The second group consists of producers of hospital furniture and facility-related equipment.

The third group consists of producers of diagnostic and laboratory products. The fourth group consists of producers of electromedical devices and selected medium-technology equipment. The fifth and most advanced group consists of companies beginning to enter high-technology medical devices through partnerships with global companies.

The overall direction is positive. Indonesia is no longer only producing simple medical supplies. The country has begun to produce or assemble more complex products, including ultrasound, mobile X-ray, ventilators, and CT scanner systems. However, the depth of technology is still uneven. Many high-end medical devices still depend on imported components, imported technology, or foreign principal support.

3.2 Number of Producers and Industry Base

Indonesia’s producer base has expanded in both quantity and variety. The industry now includes manufacturers of non-woven products, in-vitro diagnostic products, electromedical devices, laboratory equipment, hospital furniture, medical consumables, and selected advanced equipment.

The producer ecosystem includes large listed companies, private manufacturers, export-oriented producers, specialized engineering companies, and local subsidiaries or partners of multinational medical technology companies. This mix is important because no single type of producer can build the whole industry. Basic consumables require scale and cost efficiency. Hospital furniture requires engineering and fabrication capability. Diagnostic equipment requires quality assurance and regulatory compliance. Advanced devices require technology transfer, R&D, precision manufacturing, and long-term clinical trust.

The growth in the number of producers shows that Indonesia has a broadening industrial base. However, the capability level varies widely. Some producers are able to export and meet international standards, while others remain focused on domestic public procurement. Some companies have integrated manufacturing systems, while others still depend heavily on imported components or assembly-based production.

This means Indonesia’s medical device manufacturing landscape should not be viewed as one uniform industry. It is better understood as a layered ecosystem. At the bottom layer, Indonesia has a growing base of basic production. In the middle layer, it has increasingly capable producers in consumables, hospital equipment, and selected diagnostic products. At the upper layer, Indonesia is beginning to enter high-technology production through partnerships and localization programs, but this segment is still in the early stage.

3.3 Major Producer Categories

3.3.1 Consumables and Disposable Medical Devices

Consumables and disposable medical devices are among Indonesia’s strongest local production categories. These products include syringes, needles, infusion-related products, wound care products, urine bags, surgical apparel, masks, gloves, antiseptic products, and other frequently used hospital supplies.

This category is attractive for local production because demand is recurring and large. Hospitals, clinics, laboratories, and public health programs use consumables every day. The products are also easier to localize compared with highly sophisticated medical technologies. Production requires quality control and regulatory compliance, but it does not require the same level of technological complexity as MRI systems, robotic surgery platforms, or advanced laboratory automation.

Several Indonesian companies have become important players in this segment. One of the most visible examples is PT Oneject Indonesia, which is known for syringe and safety needle production. Another important player is PT Jayamas Medica Industri Tbk, known through the OneMed brand, which produces and sells a broad range of medical consumables, disposable products, diagnostic equipment, hospital furniture, and related healthcare products.

The main advantage of Indonesian producers in this segment is volume demand. The domestic market is large, and public procurement can support scale. Some producers also have export potential, especially for products that meet international quality standards.

However, competition is intense. Consumables are often price-sensitive products. Hospitals and procurement agencies may compare products based on price, availability, compliance, and reliability. Local producers must therefore maintain cost efficiency while meeting strict quality requirements.

3.3.2 Hospital Furniture and Facility Equipment

Hospital furniture is another area where Indonesia has relatively strong local capability. This category includes hospital beds, examination tables, operating tables, stretchers, trolleys, cabinets, overbed tables, waiting chairs, and other facility-related equipment.

This segment is suitable for Indonesian manufacturing because it relies on metal fabrication, design, assembly, finishing, quality control, and customization. Indonesia has industrial capability in these areas, especially in manufacturing centers with engineering and fabrication experience.

One of the most recognized producers in this category is PT Mega Andalan Kalasan. The company produces hospital beds and hospital furniture and has export experience. This type of producer is important because it shows that Indonesia can build manufacturing capability beyond simple disposable products.

Hospital furniture also has strong domestic demand. As Indonesia continues to build, upgrade, and modernize hospitals, demand for hospital beds and facility equipment will continue. Public hospital development, regional hospital improvement, and private hospital expansion all support this segment.

The challenge in this category is differentiation. Basic hospital furniture can become commoditized if buyers focus mainly on price. Producers that want to move up the value chain need to offer better design, durability, ergonomics, digital features, motorized systems, infection-control materials, after-sales service, and export-standard certification.

3.3.3 Diagnostic and Laboratory Products

Diagnostic and laboratory products are increasingly important in Indonesia’s medical device production landscape. This category includes rapid test products, in-vitro diagnostic tools, laboratory equipment, reagents, and related products used for disease detection and monitoring.

The pandemic accelerated awareness of diagnostic capacity. It showed that testing infrastructure is essential for public health response. Even after the pandemic, diagnostic demand remains important because of chronic disease management, infectious disease control, maternal health, cancer screening, tuberculosis programs, and hospital laboratory development.

Indonesia has local producers in this segment, but the level of sophistication varies. Some producers focus on simpler diagnostic products, while more advanced laboratory automation and high-end reagent systems remain dependent on imports or international partnerships.

This category has strong future potential because healthcare systems are becoming more diagnosis driven. Better diagnosis leads to earlier treatment, more efficient healthcare spending, and improved patient outcomes. However, the segment requires strong quality systems, clinical validation, regulatory compliance, and user trust. A diagnostic product that is cheap but inaccurate will not be accepted in serious healthcare settings.

Therefore, local producers must compete not only on price, but also on accuracy, consistency, regulatory documentation, quality assurance, and integration with laboratory workflows.

3.3.4 Electromedical Devices and Monitoring Equipment

Electromedical devices include products such as patient monitors, ECG machines, defibrillators, infusion pumps, ventilators, oxygen-related devices, and other electronically operated medical equipment. This segment is more complex than basic consumables and hospital furniture because it requires electronics, software, sensors, calibration, safety testing, and technical service.

Indonesia has started to develop capability in this area, especially through cooperation between local companies and foreign technology partners. Ventilator production is an important example. The local production of ventilators represents progress because ventilators require engineering, quality control, clinical reliability, and after-sales support.

However, Indonesia’s capability in electromedical devices is still developing. Many products in this category depend on imported components, foreign designs, or overseas technology platforms. Local assembly alone is not enough to create deep industrial competitiveness. The long-term goal should be to increase local engineering capability, component sourcing, software development, testing infrastructure, and certification readiness.

This segment is strategically important because electromedical devices are widely used in hospitals. Intensive care units, emergency rooms, operating rooms, and general wards all require reliable electronic medical equipment. Demand is likely to remain strong as Indonesia improves hospital quality and expands specialist healthcare services.

3.3.5 Advanced Imaging and High-Technology Devices

Advanced imaging and high-technology medical devices are the most challenging segments for local production. This category includes CT scanners, MRI systems, PET-CT systems, linear accelerators, advanced ultrasound systems, robotic surgery systems, and other high-value devices.

Indonesia is still heavily dependent on imports for most advanced devices. However, recent developments show that the country is beginning to enter this segment through strategic partnerships. The establishment of a local CT scanner production facility is an important milestone because CT scanners are high-value radiology devices used for diagnosing serious diseases such as cancer, stroke, heart disease, and other priority conditions.

The presence of local CT scanner production does not mean Indonesia has fully mastered advanced imaging technology. In the early stage, production may still rely on imported components, foreign technology, and global partner support. However, it is still an important step because it creates domestic experience in producing, assembling, testing, servicing, and distributing advanced medical technology.

For Indonesia, the development of advanced device production should be seen as a long-term journey. The country needs to build skilled engineers, technical service teams, precision manufacturing capability, quality systems, regulatory expertise, and R&D partnerships. The progress may be gradual, but it is strategically important.

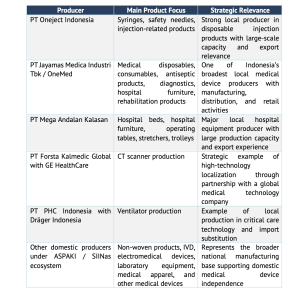

3.4 Selected Major Producers in Indonesia

The following table summarizes selected major producers in Indonesia’s medical device industry. The list is not exhaustive, but it provides an overview of important players and their product focus.

Selected Major Medical Device Producers in Indonesia

The table shows that Indonesia’s producer base is becoming more diverse. The country has companies producing basic consumables, hospital equipment, laboratory products, and selected advanced devices. This diversity is important for resilience because the healthcare system requires a wide range of products, not only one or two categories.

However, the scale and technological depth of each producer are different. Some producers operate at high volume, while others are still developing. Some are export-oriented, while others depend mainly on local procurement. Some produce finished products domestically, while others conduct localization or assembly using imported components.

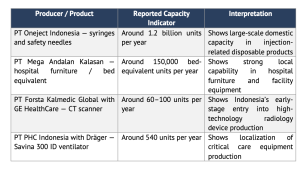

3.5 Capacity of Selected Producers

Indonesia’s production capacity differs greatly by product category. Consumables can be produced in very large volumes, while advanced devices such as CT scanners and ventilators are produced in smaller unit volumes because they are more complex and expensive.

Selected Producer Capacity Indicators

These capacity indicators demonstrate the layered structure of Indonesia’s medical device production. In basic consumables, capacity is measured in hundreds of millions or billions of units. In hospital furniture, capacity is measured in tens or hundreds of thousands of units. In advanced devices, capacity is measured in dozens or hundreds of units because the products are more complex, expensive, and technically demanding.

This difference is normal in the medical device industry. A country can produce billions of syringes but only dozens of CT scanners because the production process, value per unit, technical requirements, and demand volume are very different.

The key issue is not only capacity volume but also capacity quality. Indonesia needs to ensure that local products meet safety, quality, performance, and reliability standards. For basic products, consistency and cost efficiency are critical. For advanced products, clinical reliability, service capability, calibration, and long-term maintenance are equally important.

3.6 Production Capacity by Product Complexity

Indonesia’s production capacity can be understood more clearly by grouping products according to complexity.

Low-Complexity Products

Low-complexity products include masks, surgical apparel, simple consumables, basic wound care products, and selected disposable supplies. Indonesia has relatively strong capability in this group. These products are easier to manufacture locally because they require less advanced technology and have strong recurring demand.

However, low-complexity products are often exposed to price competition. Producers must control costs, maintain quality, and secure access to procurement channels. The biggest risk is commoditization, where buyers treat products as interchangeable and focus mostly on price.

Medium-Complexity Products

Medium-complexity products include hospital furniture, syringes, infusion-related products, selected diagnostic tools, some laboratory products, and certain electromedical devices. Indonesia has growing strength in this group. These products require better engineering, quality systems, regulatory documentation, and production discipline.

This is the most important growth zone for Indonesia in the short to medium term. The country can realistically build competitiveness in medium-complexity products if supported by investment, certification, procurement demand, and technology improvement.

High-Complexity Products

High-complexity products include CT scanners, MRI systems, PET-CT, linear accelerators, advanced ventilators, surgical robots, high-end laboratory automation, and sophisticated implant systems. Indonesia is still at an early stage in this group.

High-complexity production requires significant investment, technology transfer, precision engineering, software capability, clinical validation, and strong post-market service. Local production in this group will likely develop through partnerships with multinational companies before Indonesia can build deeper independent capability.

3.7 Role of Local Content Policy in Production Growth

Local content policy is one of the strongest drivers of Indonesia’s medical device production growth. Through TKDN requirements and procurement preference, the government encourages healthcare institutions to use locally produced devices when suitable domestic products are available.

This policy creates demand certainty for local producers. When local products are prioritized in public procurement, producers have stronger incentives to expand capacity, improve quality, and register products in government procurement platforms.

However, local content policy must be implemented carefully. If local products are available and meet quality standards, procurement preference can support industrial development. But if domestic alternatives are not yet available or do not meet clinical requirements, excessive restriction on imports can create problems for hospitals and patients.

Therefore, local content policy should not only focus on replacing imports. It should also focus on upgrading local capability. The objective should be to help Indonesian producers become more competitive, not only more protected. Protection may help companies grow in the early stage, but long-term competitiveness requires quality, innovation, efficiency, and export readiness.

3.8 Technology Transfer and Strategic Partnerships

Strategic partnerships are becoming increasingly important in Indonesia’s medical device production landscape. For advanced products, local companies often need foreign technology partners because the required expertise cannot be developed quickly from scratch.

Partnerships can take several forms. They may include local assembly, contract manufacturing, licensing, co-branding, joint ventures, technology transfer, training, or R&D collaboration. The CT scanner production facility developed through cooperation between a local healthcare company and a global medical technology company is one example of this direction. Ventilator localization through cooperation with an international medical technology company is another example.

Technology transfer is important because it can help Indonesia move from basic manufacturing toward higher-value production. However, technology transfer must be real and progressive. If localization only means final assembly, the domestic value added may remain limited. The stronger model is one where local company gradually gain engineering knowledge, supplier development, testing capability, component localization, and product development experience.

For multinational companies, partnership with Indonesian producers can be a strategic market-entry tool. It helps them align with government policy, participate in local procurement, and build long-term presence in Indonesia. For local companies, partnership can accelerate capability development and improve credibility.

3.9 Geographic Distribution of Production

Medical device production in Indonesia is concentrated mainly in industrial areas with manufacturing infrastructure, skilled labor, logistics access, and proximity to major markets. Important production areas include Java-based industrial zones such as West Java, Central Java, East Java, Banten, and the Greater Jakarta region. Yogyakarta is also relevant for hospital equipment manufacturing, especially through established local engineering companies.

The concentration of production in Java is understandable because Java has stronger infrastructure, industrial estates, ports, suppliers, and healthcare demand. However, this also creates a regional imbalance. Many healthcare facilities outside Java still depend on distribution networks that transport products from Java or from import gateways.

In the long term, Indonesia may need to develop a more distributed support ecosystem, especially for service centers, maintenance, calibration, and spare parts. Medical device production may remain concentrated in industrial hubs, but after-sales capability must be available closer to healthcare facilities across the country.

This is especially important for electromedical and advanced devices. A hospital in eastern Indonesia cannot rely only on a producer or principal located in Java if a critical device requires urgent repair. Therefore, production capacity must be supported by service capacity.

3.10 Producer Strengths

Indonesia’s local producers have several strengths.

- The first strength is domestic market access. Local producers understand Indonesian procurement behavior, hospital needs, pricing sensitivity, and regulatory requirements. This gives them an advantage over foreign companies that rely entirely on importers or distributors.

- The second strength is policy support. Government preference for domestic products gives local producers stronger opportunities, especially in public procurement. This is particularly important for products that already have local alternatives.

- The third strength is cost competitiveness. For selected categories, Indonesian producers can offer competitive pricing because of local labor, domestic production, and proximity to buyers.

- The fourth strength is product adaptation. Local producers can adjust products to Indonesian hospital needs, language requirements, service expectations, and regional conditions.

- The fifth strength is growing export experience. Some Indonesian producers have already entered overseas markets, showing that local medical devices can compete beyond the domestic market when quality and certification are sufficient.

3.11 Producer Weaknesses

Despite positive progress, Indonesia’s producers still face several weaknesses.

- The first weakness is limited technology depth. Many producers are still concentrated in low- and medium-complexity products. Advanced technology production remains dependent on foreign partners.

- The second weakness is dependence on imported raw materials and components. Even when final products are made locally, key inputs may still come from abroad. This limits the true level of domestic value added.

- The third weakness is uneven quality capability. Some producers meet high standards and are export-ready, while others may still need improvement in quality management, documentation, testing, and compliance.

- The fourth weakness is limited R&D. Strong medical device innovation requires research, engineering, clinical validation, and collaboration between companies, universities, hospitals, and regulators. This ecosystem is still developing in Indonesia.

- The fifth weakness is service capability outside major cities. Producers of advanced devices must provide maintenance, calibration, spare parts, and technical support across the country. This remains a challenge due to Indonesia’s geography.

3.12 Future Direction of Local Producers

The future direction of Indonesia’s medical device producers should not only be about producing more products. It should be about producing better, more competitive, and more technologically advanced products. In the short term, local producers can continue to strengthen basic consumables, hospital furniture, diagnostic tools, and selected electromedical devices. These categories match Indonesia’s current industrial capability and domestic demand.

In the medium term, producers should move toward higher-value products through technology partnerships, better certification, automation, digital integration, and stronger R&D. Products such as patient monitors, ultrasound systems, ventilators, laboratory devices, and connected healthcare tools can become important growth areas. In the long term, Indonesia should aim to build deeper capability in advanced imaging, specialist treatment equipment, medical software integration, precision components, and export-oriented production.

The Ministry of Industry reported 626 medical-device industries in SIINas in 2025, covering non-woven products, IVD, electromedical devices, medical/laboratory equipment, and related categories. The Ministry of Health reported that, as of April 1, 2024, Indonesia had more than 15,000 domestic medical-device products, with 66.63% having TKDN above 40%, while e-catalogue domestic medical-device transactions reached around Rp14 trillion in 2023. For selected capacity indicators, Oneject’s syringe and safety needle capacity is reported at 1.2 billion units per year, Mega Andalan Kalasan reports 150,000 bed-equivalent units per year, the Forsta–GE HealthCare CT scanner facility is reported at 60–100 units per year, and the Savina 300 ID ventilator facility is reported at 540 units per year.

Chapter 4: Major Distributors of Medical Devices in Indonesia

4.1 Overview of Medical Device Distribution in Indonesia

Distribution is one of the most important parts of Indonesia’s medical device industry. In a country with thousands of islands, uneven healthcare infrastructure, and large differences between urban and regional markets, the ability to distribute medical devices is almost as important as the ability to produce or import them.

A medical device company in Indonesia does not only need product registration. It also needs a reliable distribution system. The distributor must be able to store products properly, deliver them safely, manage regulatory documents, support procurement requirements, provide technical assistance, and offer after-sales service.

For advanced medical equipment, distribution also includes installation, training, calibration, maintenance, spare parts, and emergency repair. This makes Indonesia’s medical device distribution sector highly strategic. Distributors connect manufacturers with hospitals, clinics, laboratories, pharmacies, government institutions, and other healthcare providers. They also help foreign manufacturers enter the Indonesian market by handling importation, registration support, product listing, sales, service, and local market access.

By 2026, the role of distributors has become more complex. The market is no longer only about selling imported products. Distributors must now adapt to local content policy, e-catalogue requirements, CDAKB certification, government procurement rules, and increasing competition from local producers. In this environment, the strongest distributors are those that combine national reach, regulatory compliance, principal relationships, technical service capacity, and procurement access.

4.2 Role of Distributors in the Medical Device Ecosystem

Distributors in Indonesia perform several important functions.

- The first function is market access. A distributor helps producers and foreign principals reach hospitals, clinics, laboratories, pharmacies, and government buyers. This is especially important for foreign companies that do not have their own direct commercial organization in Indonesia.

- The second function is regulatory support. Medical devices require product registration and distribution permits before they can be legally sold. Distributors often help principals navigate local regulatory requirements, maintain documentation, and ensure that products meet Indonesian rules.

- The third function is procurement access. Government procurement is a major channel for medical devices. Products sold to public healthcare institutions often need to be listed in the e-catalogue system. Distributors with experience in public procurement have an advantage because they understand documentation, pricing, negotiation, compliance, and transaction processes.

- The fourth function is logistics. Medical devices must be stored, transported, and delivered under proper conditions. Some products require temperature control, careful handling, sterile packaging protection, or special storage conditions. A weak logistics system can damage products and create safety risks.

- The fifth function is technical support. Many medical devices, especially electronic and high-end equipment, require installation, user training, calibration, maintenance, and repair. Distributors with biomedical engineers and service teams are more valuable than distributors that only provide sales and delivery.

- The sixth function is after-sales relationship management. Hospitals need assurance that spare parts, consumables, accessories, warranties, and service contracts are available. This is especially important for expensive equipment such as imaging systems, operating room devices, ventilators, laboratory analyzers, and monitoring systems.

4.3 Regulatory Requirements for Distribution

Medical device distribution in Indonesia is regulated because medical devices directly affect patient safety. A distributor must comply with licensing and good distribution practice requirements. One of the key requirements is IDAK, or Izin Distribusi Alat Kesehatan. This is a medical device distribution license. A company that distributes medical devices must have the appropriate legal and regulatory approval to operate as a distributor.

Another important requirement is CDAKB, or Cara Distribusi Alat Kesehatan yang Baik. CDAKB is Indonesia’s good distribution practice standard for medical devices. It covers proper handling, storage, distribution, documentation, quality control, complaint management, product recall, and post-market responsibilities.

CDAKB has become increasingly important because it is connected to government procurement access. Distributors that want to participate in the health sector e-catalogue need to meet the relevant requirements. This raises the standard for medical device distributors and encourages a more professional distribution environment. The regulatory direction is clear: Indonesia wants distributors to move from ordinary trading activity toward quality-managed healthcare distribution. This is positive for patient safety and market discipline. However, it also increases compliance costs for smaller distributors.

4.4 E-Catalogue and Public Procurement Access

The e-catalogue system is one of the most important channels for medical device distribution in Indonesia. Public hospitals and government healthcare institutions often purchase medical devices through government procurement platforms. Therefore, access to the e-catalogue can strongly influence a distributor’s sales potential.

For distributors, e-catalogue participation requires documentation readiness, product data accuracy, pricing discipline, regulatory compliance, and the ability to meet transaction requirements. Products must be properly listed, and distributors must be able to respond to procurement processes such as negotiation, mini-competition, and other purchasing mechanisms.

The transition from older e-catalogue versions to newer procurement systems also shows that Indonesia’s public procurement environment is becoming more digital and more structured. This can improve transparency and efficiency, but it also requires distributors to continuously update their systems and documentation. For local producers, e-catalogue access can open large opportunities in public procurement, especially when products have strong TKDN. For importers and foreign principals, e-catalogue access remains important but more challenging due to local content preference and stricter listing requirements. The practical result is that distributors with strong regulatory and digital procurement capability have a competitive advantage. They can help principals maintain market access even when rules change.

4.5 Types of Medical Device Distributors in Indonesia

Indonesia’s medical device distributors can be divided into several types.

- The first type is the national broadline healthcare distributor. These companies distribute a wide range of healthcare products, including pharmaceuticals, consumer health products, medical devices, diagnostics, and hospital supplies. They usually have nationwide branch networks, warehouses, logistics systems, and relationships with many healthcare customers.

- The second type is the specialist medical equipment distributor. These companies focus on specific categories such as imaging, critical care, surgery, laboratory diagnostics, orthopedics, dental equipment, or hospital engineering products. They may not have the same branch scale as broadline distributors, but they often have stronger technical expertise in their product segment.

- The third type is the multinational-affiliated or regional distributor. These companies operate in several Asian markets and represent international medical technology brands. They often combine product distribution with clinical education, biomedical service, hospital planning, and regional supply-chain support.

- The fourth type is the local producer-distributor. Some Indonesian manufacturers also operate their own distribution network. This model is common when producers want to control market access, serve public procurement directly, and maintain customer relationships.

- The fifth type is the procurement and project-based distributor. These companies may focus on tenders, hospital projects, equipment packages, and large institutional procurement. Their strength is not always warehousing scale, but their ability to manage bids, documentation, financing, project delivery, and installation.

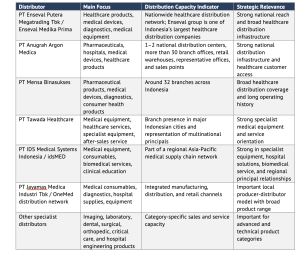

4.6 Selected Major Distributors in Indonesia

The following table summarizes selected major medical device distributors in Indonesia. The list is not exhaustive, but it represents important types of distributors in the market.

Selected Major Medical Device Distributors in Indonesia

This table shows that distribution capacity is not measured only by the number of branches. A distributor may be strong because of national coverage, product specialization, technical service, regulatory competence, principal relationships, e-catalogue access, or project execution capability.

For basic consumables, large branch networks and warehouse coverage are important. For advanced equipment, technical service and principal authorization are often more important than the number of warehouses. For public procurement, documentation and e-catalogue readiness are critical. For private hospitals, relationship management and after-sales reliability are often decisive.

4.7 Capacity of Major Distributors

Distribution capacity in Indonesia should be understood through several dimensions.

- The first dimension is geographic coverage. A strong distributor must be able to serve not only Jakarta and large cities but also regional hospitals and healthcare facilities outside Java. Indonesia’s geography makes this difficult because delivery may require inter-island logistics, local warehousing, and regional service teams.

- The second dimension is warehouse and inventory capacity. Medical devices must be stored properly. Consumables require inventory availability. Sterile products require packaging protection. Some diagnostic products require specific storage conditions. High-value equipment requires secure handling.

- The third dimension is regulatory capacity. Distributors must maintain valid licenses, product registrations, quality documentation, and distribution records. They must also handle complaints, recalls, and post-market activities.

- The fourth dimension is technical service capacity. This is essential for equipment that requires installation, calibration, maintenance, and repair. A distributor without technical service capability may be suitable for simple consumables but not for complex medical devices.

- The fifth dimension is digital and procurement capacity. Distributors must increasingly operate through digital procurement systems, e-catalogue platforms, and structured government purchasing channels. They must maintain accurate product information, pricing, and transaction readiness.

- The sixth dimension is principal management. Many distributors represent foreign medical device companies. They must manage relationships with principals, comply with brand standards, conduct product training, forecast demand, and support product launches.

A distributor with strong performance across these dimensions has a higher chance of becoming a strategic partner in the Indonesian healthcare market. Medical device distribution is a critical part of Indonesia’s healthcare ecosystem. Because Indonesia is geographically complex and highly regulated, distributors must do more than move products from producers to buyers. They must manage regulatory compliance, logistics, procurement access, technical service, inventory, customer relationships, and after-sales support.

The market size and import flow from 2020 to 2025 show that distributors handle a large and strategically important product flow. Imports remain significant, especially for advanced medical devices, while local production also requires strong distribution networks to reach healthcare facilities across the country.

Major distributors include broadline healthcare distributors, specialist medical equipment distributors, regional medical supply-chain companies, and producer-distributor models. Companies such as Enseval, Anugrah Argon Medica, Mensa Binasukses, Tawada Healthcare, idsMED Indonesia, and OneMed represent different forms of distribution strength in Indonesia.

The strongest distributors are not necessarily those with the most products. They are the companies that can combine national reach, regulatory readiness, e-catalogue access, principal relationships, technical expertise, after-sales service, and the ability to serve both public and private healthcare markets.

As Indonesia moves toward 2026, medical device distribution will become increasingly professional and policy sensitive. Distributors that adapt to stricter regulation, digital procurement, local content policy, and service-based competition will be better positioned to succeed.

Chapter 5: Import and Export Statistics of Medical Devices

5.1 Overview of Indonesia’s Medical Device Trade

Indonesia’s medical device trade reflects the structure of the country’s healthcare industry. The domestic market is large, but the production base is still developing. Local manufacturing has grown significantly, especially in consumables, hospital furniture, basic medical equipment, and selected diagnostic or electromedical products. However, Indonesia still depends heavily on imports for many advanced medical devices, particularly high-technology diagnostic, surgical, laboratory, and treatment equipment.

From 2020 to 2025, Indonesia’s medical device trade moved through a volatile period. The COVID-19 pandemic created extraordinary demand for medical products, followed by a correction after emergency purchasing declined. At the same time, Indonesia increased its policy focus on local production, domestic component requirements, and public procurement preference for locally made medical devices.

Therefore, import and export statistics must be interpreted carefully. A decline in imports does not always mean weaker healthcare demand. It may indicate normalization after pandemic procurement, import substitution, local content policy, or delayed hospital investment. Similarly, an increase in exports does not automatically mean that Indonesia has become a fully competitive global medical device producer. Exports may be concentrated in specific product categories and may fluctuate depending on global demand.

The key point is that Indonesia’s medical device trade is in transition. Imports remain important, but local production is becoming more visible. Exports show potential, but they are not yet stable enough to position Indonesia as a major global medical device exporter.

5.2 Import Statistics from 2020 to 2025

Indonesia’s medical device imports reached USD 2.564 billion in 2020 and increased to USD 2.633 billion in 2021. This was the pandemic-driven period, when Indonesia required large quantities of medical devices and healthcare supplies. Demand was especially high for diagnostic products, personal protective equipment, respiratory support devices, patient monitoring equipment, and other pandemic-related products.

In 2022, imports declined to USD 1.974 billion. The decline continued in 2023, when imports reached USD 1.778 billion. In 2024, imports were relatively stable at USD 1.786 billion. In 2025, imports were estimated to increase to USD 1.908 billion.

The data shows three important patterns.

- First, imports were highest during the pandemic period. The 2020 and 2021 figures were elevated because Indonesia needed urgent medical supplies and equipment

- Second, imports declined sharply after the pandemic peak. This was caused by reduced emergency demand, normalization of procurement, and stronger government pressure to use domestic products where available.

- Third, imports remained significant even after the decline. The 2025 estimate of USD 1.908 billion shows that Indonesia still needs imported medical devices. This is especially true for advanced technologies that are not yet widely produced domestically.

- The import pattern confirms that Indonesia is not fully self-sufficient in medical devices. Local production is growing, but imports remain essential for high-end and specialized healthcare technology.

5.3 Export Statistics from 2020 to 2025

Indonesia’s medical device exports also changed significantly during the same period. Exports reached USD 1.011 billion in 2020 and increased to USD 1.377 billion in 2021. In 2022, exports rose sharply to USD 2.724 billion, the highest level in the period. Exports then declined to USD 2.158 billion in 2023 and USD 1.873 billion in 2024. In 2025, exports were estimated to recover to USD 2.501 billion.

The export trend shows that Indonesia has real export capacity in certain medical device categories. However, the movement is volatile. The sharp increase in 2022 suggests that Indonesia benefited from strong external demand in selected product groups. The decline in 2023 and 2024 shows that export momentum was not fully sustained.

In 2025, exports were estimated to increase again, suggesting that Indonesia may regain some export strength. However, the export structure still requires deeper analysis. A high export number does not necessarily mean that Indonesia is exporting advanced technologies. Many exports may still come from lower- or medium-complexity products such as consumables, medical furniture, basic devices, or contract-manufactured products. Indonesia’s export opportunity will depend on product quality, international certification, pricing, delivery reliability, production scale, and the ability to meet destination-country regulatory requirements.

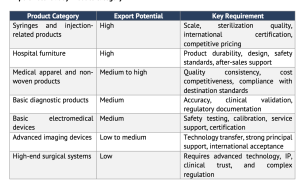

5.4 Export Strength by Product Category

Indonesia’s export strength is more visible in categories that match local manufacturing capability. These include medical consumables, hospital furniture, selected disposable products, non-woven medical products, basic diagnostic tools, and selected equipment produced under domestic or partnership-based manufacturing models.

Indonesia has several advantages in these export categories. It has a large labor force, growing manufacturing infrastructure, increasing domestic production experience, and proximity to regional markets. For products that do not require extremely advanced technology, Indonesia can compete through cost efficiency, production scale, and quality improvement.

However, export competitiveness depends on more than price. Medical devices are regulated products, so exporters must meet the requirements of destination countries. This may include ISO 13485 certification, product testing, technical documentation, sterilization validation, clinical evidence, CE marking for Europe, FDA requirements for the United States, or country-specific registration in ASEAN markets.

Table 5.5

Export Potential by Product Category

Indonesia’s short-term export opportunity is strongest in products where domestic producers already have capability and where international buyers are open to cost-competitive alternatives. The longer-term opportunity is to move into higher-value products through partnerships and technology upgrading.

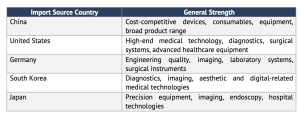

5.7 Key Import Source Countries

Indonesia imports medical devices from several major global producers. The import market is led by China, followed by the United States, Germany, South Korea, and Japan. These countries are important because they supply different types of medical technologies. China is a major source of cost-competitive medical devices, consumables, hospital equipment, and increasingly more advanced products. The United States is strong in high-end medical technology, diagnostics, surgery, life sciences tools, and hospital equipment.

Germany is known for engineering quality, imaging, laboratory systems, surgical instruments, and hospital technology. South Korea is increasingly active in diagnostics, imaging, aesthetic devices, and digital health-related equipment. Japan is strong in precision medical technology, imaging, endoscopy, and hospital equipment.

Major Medical Device Import Source Countries for Indonesia

These source countries reflect Indonesia’s mixed demand profile. The country needs both affordable products and advanced technologies. This creates a diverse import market in which price, quality, technology, regulatory compliance, and service capability all matter.

5.8 Export Destination Opportunities

Indonesia’s medical device export opportunities can be divided into regional and global markets.

- The first opportunity is ASEAN. ASEAN markets are geographically close and may be more accessible than Europe or the United States. Countries such as Malaysia, Thailand, Vietnam, the Philippines, Singapore, Cambodia, Laos, and Myanmar may offer opportunities depending on product category and regulatory requirements. However, ASEAN is also competitive. Malaysia and Thailand already have strong medical device manufacturing bases, while Singapore is a high-standard regional hub.

- The second opportunity is the Middle East and Africa. These regions may offer demand for cost-competitive medical consumables, hospital furniture, and basic healthcare equipment. Indonesian exporters may have opportunities if they can meet quality requirements and build distribution partnerships

- The third opportunity is developed markets such as the European Union, United States, Japan, and Australia. These markets offer higher value but are much harder to enter. Producers must meet strict regulatory standards, strong documentation requirements, quality systems, and post-market surveillance obligations.

- The fourth opportunity is humanitarian and institutional procurement. Products such as syringes, medical consumables, hospital supplies, and basic equipment may be purchased by international organizations, aid agencies, or government programs. This channel requires strong quality assurance, large-scale production, and reliable delivery.

The most realistic export strategy for Indonesia is to start with categories where the country has proven capability, then gradually move into more regulated and higher-value markets.

Chapter 6: Potential Issues and Challenges

6.1 Overview of Challenges in Indonesia’s Medical Device Industry

Indonesia’s medical device industry has strong growth potential, but the sector also faces significant challenges. The country has a large healthcare market, growing local production, supportive government policy, and increasing demand from hospitals, clinics, laboratories, and public health programs. However, market potential does not automatically become market success.

The medical device industry is complex because it combines healthcare regulation, manufacturing capability, import activity, distribution networks, public procurement, clinical quality, and after-sales service. A company that wants to operate successfully in Indonesia must understand all these layers. It is not enough to have a good product. The product must be registered, distributed properly, accepted by healthcare users, priced competitively, supported technically, and aligned with government procurement policy.

The main barriers in Indonesia can be grouped into several areas: regulatory complexity, import dependency, limited local technology capability, raw material dependency, procurement challenges, pricing pressure, distribution difficulty, after-sales service limitations, quality and certification gaps, talent shortage, R&D limitations, and competition from global producers.

These challenges do not mean that Indonesia is an unattractive market. On the contrary, they show that Indonesia is a large but demanding market. Companies that understand the barriers can build stronger strategies. Policymakers that understand the barriers can design better interventions. Local producers that understand the barriers can upgrade their capability more realistically.

6.2 Regulatory Complexity

Regulation is one of the biggest barriers in Indonesia’s medical device industry. Medical devices must be properly registered before they can be sold. Distributors must have valid licenses. Product documentation must be prepared correctly. Companies must comply with quality, safety, labeling, and post-market requirements.