Preface

The aluminium industry in Indonesia is entering a transformative period—one shaped by rising domestic demand, abundant raw materials, strong government push for downstream processing, and global shifts in supply chains and energy economics. For a long time, Indonesia was primarily known as a supplier of bauxite, exporting huge volumes to countries with more advanced refining and smelting capabilities. Today, the national agenda has shifted dramatically. Indonesia aims to become a major centre for alumina refining, primary aluminium smelting, and downstream aluminium manufacturing, positioning the industry as one of the pillars of the nation’s future industrial economy.

Aluminium is one of the world’s most essential industrial metals. It is lightweight yet strong, corrosion- resistant, recyclable without loss of quality, and suitable for high-precision applications. These properties make aluminium indispensable in construction, infrastructure, packaging, transportation, automotive (especially EVs), renewable energy components, consumer goods, and machinery. In an era focused on sustainability and energy efficiency, aluminium’s importance continues to grow.

Indonesia finds itself with a rare strategic advantage. The country owns large bauxite deposits—primarily in West Kalimantan, West Sumatra, and the Riau Islands—and has implemented bold policies encouraging domestic processing rather than exporting raw materials. This has triggered billions of dollars of investment into alumina refineries, smelting complexes, industrial zones, and supporting infrastructure. Companies from China, the Middle East, and ASEAN countries have committed to large-scale industrial projects through joint ventures, industrial estate developments, and long-term strategic partnerships.

However, the transformation is not without challenges. Aluminium smelting remains energy-intensive, and Indonesia’s electricity prices are higher compared to major global aluminium hubs that rely heavily on hydropower. Downstream manufacturers in Indonesia are technologically capable but still dependent on imported primary aluminium, leading to a structural mismatch between upstream and downstream segments. The value chain is expanding, but the pace of upstream growth has not yet matched domestic consumption.

Domestic demand has been rising consistently due to rapid urbanisation, large-scale infrastructure programmes, expansion of the packaging industry, and growing automotive and electronics manufacturing. At the same time, global aluminium dynamics—affected by China’s dominance, geopolitical shifts, energy crises in Europe, supply chain diversification, and environmental commitments—have created both opportunities and risks for Indonesia.

The period of 2020–2025 is particularly important. It captures the volatile post-pandemic recovery, global commodity fluctuations, supply chain disruptions, export policy changes in Indonesia, and significant industrial investment decisions across Kalimantan and Sumatra. This makes it a crucial window for assessing Indonesia’s competitive positioning.

This report aims to deliver a comprehensive, detailed, and integrated analysis of Indonesia’s aluminium industry from strategic, economic, industrial, and global perspectives. It is designed to help policymakers, investors, business leaders, analysts, and industry professionals understand the sector’s complexities, evaluate its potential, and make informed decisions for the future.

Strategic Highlights of Indonesia’s Aluminium Industry

Indonesia’s Structural Advantages

- One of the world’s largest bauxite reserves, providing long-term upstream security.

- Government commitment to “hilirisasi” (downstream mineral processing).

- Increasing foreign investment from China, Middle East, and ASEAN industrial groups.

- Rapid domestic growth in aluminium-consuming sectors (construction, packaging, EV components).

- Strategic location near major Asian aluminium demand centres (China, Japan, Korea, India).

Key Realities Shaping the Sector

- Domestic smelting capacity is still far below national demand.

- Downstream manufacturers rely heavily on imported primary aluminium.

- Electricity cost remains one of the biggest obstacles to competitive smelting.

- Transporting bauxite from remote mining areas to refineries is a logistical challenge.

- Environmental and social pressures are intensifying in mining regions.

Global Context Affecting Indonesia

- China’s overwhelming dominance in global aluminium production affects pricing and competitiveness.

- Europe’s energy crisis (2021–2023) caused several smelters to shut down.

- Global zero-carbon commitments increase pressure on aluminium producers to adopt cleaner energy.

- Supply chain diversification encourages investors to look beyond China for new production bases.

- Rising global demand for aluminium in EVs, solar panels, and lightweight transportation products.

Opportunities for Indonesia

- Building a fully integrated value chain from bauxite → alumina → aluminium →downstream products.

- Development of renewable-powered smelting hubs (especially hydropower-based Kalimantan zones).

- Import substitution for domestic downstream industries.

- Growth in recycled aluminium and circular-economy initiatives.

- Export potential for alumina, billets, rolled products, and extrusion materials.

- Potential to become ASEAN’s primary aluminium processing hub.

Risks and Structural Challenges

- High electricity prices and limited access to stable, low-cost energy.

- Technology gaps in producing high-grade alloys and rolled products.

- Bauxite export policy uncertainty, affecting investor confidence.

- Competition with low-cost producers in China, India, and the Middle East.

- Environmental requirements that will become stricter over time.

Reasons Why This 2020–2025 Window Matters

- Major industrial zones in Kalimantan (e.g., Ketapang, Mempawah, and IKN-related regions) are expanding.

- Several new alumina projects have entered development or operation.

- Smelting investments have been announced and funded by international partners.

- Import volume trends show a rising reliance on primary aluminium despite national resource abundance.

- Construction and automotive sectors are at multi-year demand peaks.

- Global aluminium markets remain volatile, creating both risk and opportunity.

Purpose of This Report

This report intends to provide:

- A deep understanding of the aluminium market landscape in Indonesia.

- A comprehensive assessment of supply, demand, production, and trade.

- A clear mapping of major players, industrial zones, and supply chains.

- A data-driven exploration of 2020–2025 trends.

- A strategic evaluation of opportunities and risks.

- A global benchmark positioning Indonesia relative to ASEAN, EU, and U.S. markets.

- Clear, actionable insights for policymakers, investors, and manufacturers.

The aluminium industry is not just another industrial segment—it is a foundation for Indonesia’s long-term economic modernization. It supports infrastructure, manufacturing, the energy transition, and the country’s ambition to move from a raw-material economy to a value-added industrial powerhouse.

This Preface lays the foundation for the chapters that follow, which will explore the Indonesian aluminium industry in depth, using structured analysis, updated statistics, and strategic interpretation.

Market Trend and Size

The Indonesian aluminium market has entered a phase of structural expansion, driven by downstream industrial growth, national mineral-downstreaming policies, and changing patterns of domestic consumption. Although the country remains in a transition phase from raw-material export to value-added production, the fundamental market trajectory shows consistent, broad-based growth anchored in infrastructure, manufacturing, energy, and consumer sectors. This chapter presents a holistic view of Indonesia’s aluminium market, examining market dynamics, structural trends, demand sectors, supply constraints, and projected growth outlook.

2.1 Overall Market Direction

Indonesia’s aluminium market is characterized by steady multi-year demand growth combined with a slower but improving domestic supply base. This dual dynamic creates a market environment where consumption consistently outpaces local production, sustaining a strong reliance on imported primary aluminium but simultaneously incentivizing large-scale investment in refining and smelting.

Three overarching forces define the direction of the market:

- Domestic demand is rising across nearly all major aluminium-consuming industries.

- Domestic upstream capabilities are still developing, particularly in smelting and high-purity alloy production.

- Government industrial policies strongly encourage downstream processing to maximize value addition.

The result is a fast-growing downstream market supported by construction, automotive, packaging, electrical, and renewable energy sectors, alongside moderate upstream capacity growth limited by energy pricing, technology gaps, and capital intensity.

Using trend-based modelling, industrial growth patterns, downstream consumption ratios, and typical aluminium usage intensity across sectors, the total Indonesian aluminium market is estimated as follows:

Estimated Forecast Aluminium Market Value – Indonesia (2025–2030)

*Estimated CAGR (2025–2030): ~7.6–8.1%

2.2 Demand-Side Trends

Demand for aluminium in Indonesia is shaped by several long-lasting macroeconomic and structural drivers:

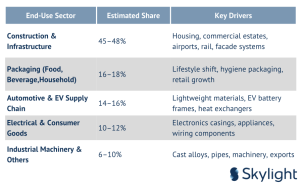

A. Construction and Infrastructure

The construction sector remains the single largest aluminium consumer in the country. Aluminium is used extensively in:

- Window and door frames

- Curtain walls and facade systems

- Roofing

- Structural profiles

- Modular components for prefabricated buildings

- Industrial estate construction

Growth in public and private projects—roads, bridges, mass housing, airports, industrial zones—creates continuous, predictable demand for extrusions, sheets, coils, and construction-grade alloys.

Trend Summary:

Demand is strong, stable, and deeply tied to national development cycles.

B. Automotive and Transportation

With Indonesia’s ambition to become an automotive manufacturing hub, especially for electric vehicles (EVs), aluminium demand is expanding in:

- Body panels

- Chassis and structural components

- Battery enclosures

- Heat exchangers

- Wheels and engine parts

Lightweight materials have become essential for fuel efficiency and EV performance, positioning aluminium as a primary material for next-generation vehicle platforms.

Trend Summary:

This segment is experiencing structural, technology-driven demand growth.

C. Packaging and Consumer Goods

Urbanisation, rising household income, and changes in consumption habits have increased demand for:

- Aluminium foil for food & beverage

- Flexible packaging

- Household product casings

- Consumer electronics (laptops, smartphones, appliances)

- Cooking utensils and containers

The packaging sector, in particular, has shifted rapidly toward aluminium-based solutions due to hygiene, recyclability, and barrier properties.

Trend Summary:

Fast-growing, highly stable, and supported by long-term demographic trends.

D. Renewable Energy and Industrial Technology

Indonesia’s energy transition adds new uses for aluminium:

- Solar panel frames

- Mounting systems

- Transmission components

- Heat-sinks and power electronics enclosures

In addition, solar and EV supply-chain expansion increases demand for high-grade extrusions and rolled products.

Trend Summary:

Emerging but rapidly accelerating; tied to energy policy and green manufacturing.

2.3 Supply-Side Trends

Indonesia’s aluminium supply environment is shaped by local resource availability, industrial capabilities, technological limits, and energy economics.

A. Upstream (Mining → Refining → Smelting)

Domestic bauxite resources are abundant, supporting long-term upstream potential. The challenge lies in:

- Refining bauxite into alumina

- Smelting alumina into primary aluminium requiring massive electricity supply

- Maintaining cost competitiveness against global producers

Current upstream characteristics:

- Refining capacity is expanding through new industrial complexes

- Smelting expansion is slower due to high operational cost

- Imports still fill a substantial portion of primary aluminium demand

Trend Summary:

Upstream growth is steady but restrained; long-term trajectory depends on energy policy and capital investment.

B. Downstream Fabrication (Extrusions → Rolled Products → Components)

Indonesia’s downstream aluminium manufacturing base is substantially more developed and grows faster than upstream capacity. Industries produce:

- Extrusions for construction and EVs

- Rolled sheets and coils

- Foils for packaging

- Casting alloy components

- Consumer-product aluminium parts

This segment is closely tied to domestic demand and is increasingly export capable.

Trend Summary:

High momentum and high value-added; the main driver of total market value.

Structural Characteristics of the Market

Several structural realities define Indonesia’s aluminium industry:

Structural Characteristic 1: Downstream Grows Faster than Upstream

Local fabrication and industrial demand are growing at a faster pace than primary aluminium production. This leads to:

- Continuous import reliance

- Opportunities for smelter investment

- Price sensitivity to global markets

Structural Characteristic 2: Energy Costs Limit Smelting Expansion

Aluminium smelting requires extremely low-cost electricity. Indonesia’s reliance on conventional power sources increases production cost, reducing global competitiveness.

Structural Characteristic 3: High Logistics Dependence

Many bauxite deposits and alumina refineries are geographically distant from fabrication centres, increasing logistics complexity and cost.

Structural Characteristic 4: Technology Gap in High-Grade Alloys

While domestic extruders and rolling mills are advancing, Indonesia still imports:

- High-purity primary aluminium

- Aerospace and defense-grade alloys

- Advanced automotive alloys

Structural Characteristic 5: Policy-Driven Industrialisation Government policy directly influences:

- Bauxite export restrictions

- Incentives for refining/smelting

- Industrial estate development

- Import tariffs on aluminium products

- Local content requirements (TKDN)

2.5 Market Outlook Through 2025

Even without precise numerical values in this version, the growth direction is clear: Demand Outlook

- Construction demand grows steadily in line with national development plans.

- Automotive industry demand accelerates as EV adoption rises.

- Renewable energy systems increase consumption of extrusions and frames.

- Packaging demand remains strong and resilient.

Supply Outlook

- Alumina refining capacity increases moderately in line with upstream investments.

- Smelting capacity expands more slowly due to energy constraints.

- Import dependence remains high in the short term.

Value Chain Outlook

- Downstream industries continue to dominate overall market value.

- Export potential increases in semi-finished and fabricated aluminium products.

- Sustainability and recycling become central themes for long-term competitiveness.

2.6 Key Market Risks Through 2025

Even in a growing market, certain risks must be managed carefully:

- Energy Cost Volatility: High electricity prices suppress smelting competitiveness.

- Regulatory Uncertainty: Shifts in export bans and downstreaming rules affect planning.

- Global Price Fluctuations: Aluminium prices are sensitive to China, India, and global energy markets.

- Quality & Technology Gap: Imports will continue for specialised alloys not yet produced domestically.

- Environmental Pressure: Mining areas face increasing demands for remediation and sustainability compliance.

- Downstream Overdependence on Imports: If smelting doesn’t catch up, downstream growth may face cost and supply risks.

2.7 Strategic Takeaways

- Indonesia’s aluminium market is structurally in growth mode, driven by downstream demand and industrial expansion.

- Domestic supply growth is slower than demand, creating structural gaps but also investment opportunities.

- Downstream processing, fabrication, and recycling represent the highest value-creation segments.

- Smelting expansion will depend on energy economics, technology partnerships, and favourable policy designs.

- For the long-term, Indonesia has the potential to become a regional aluminium hub—but only if upstream bottlenecks are systematically addressed.

Distribution Network of Aluminum in Indonesia

The distribution network of Indonesia’s aluminium industry is not just a physical flow of metal from mine to end user; it is a cost-defining, competitiveness-shaping system. High logistics costs, fragmented geography, and unequal infrastructure development mean that how aluminium moves inside Indonesia can be as important as how much aluminium Indonesia produces.

This chapter expands on the earlier version by:

- Mapping the physical flow of aluminium across Indonesia.

- Breaking down the cost structure of distribution.

- Identifying key logistics corridors.

- Profiling the Top 10 major aluminium producers/suppliers that act as national distributors, with capacity notes where available.

- Analysing how these factors affect pricing, reliability, and competitiveness.

3.1 Role of Distribution in the Aluminium Value Chain

The aluminium value chain in Indonesia can be summarised as:

- Upstream

- Bauxite mines → domestic alumina refineries → smelters (primary aluminium).

- Midstream

- Primary aluminium ingots/billets → downstream processors (extruders, rolling mills, foil plants, casting operations).

- Downstream

- Aluminium profiles, sheets, coils, foils, and finished components → distributors, trading houses, industrial users (construction, automotive, packaging, electronics, renewable energy, etc.).

In this chain, distribution does three critical things:

- Connects remote resources to demand centres (e.g., Kalimantan → Java).

- Adds cost and time, affecting final sale price and working capital.

- Determines reliability (on-time delivery vs delays), which can be more important than the transport charge itself.

Indonesia’s geography—17,000+ islands with population and industry highly concentrated in Java—makes aluminium logistics structurally complex.

3.2 Physical Flow of Aluminium in Indonesia

3.2.1 Typical Material Path

A stylised aluminium flow looks like this:

- Bauxite mines

- Mainly in West Kalimantan, West Sumatra, Riau Islands/Bintan.

- Alumina refineries

- Located in Kalimantan, Sumatra, and new industrial hubs.

- Bauxite is transported by truck + barge/ship to these refineries.

- Smelters (Primary Aluminium)

- Dominated by PT Indonesia Asahan Aluminium (INALUM), currently with aluminium smelter capacity around 250–275 thousand tonnes per year.

- Future expansions plan to lift national aluminium capacity to 900,000 tonnes per year by 2029, via new smelter projects.

- Downstream processors

- Extrusion plants, rolling mills, foil manufacturers, and recycling billet makersconcentrated around:

- Greater Jakarta/Bekasi/Karawang

- Surabaya–Sidoarjo–Gresik

- Tangerang/Serang

- Medan & Batam (smaller but strategic export hubs).

- Extrusion plants, rolling mills, foil manufacturers, and recycling billet makersconcentrated around:

- National distribution to end users

- Construction material distributors, door/window system dealers, packaging converters, OEM automotive & electronics manufacturers, and export customers.

The longest and most expensive legs are typically:

- From mine/refinery regions (Kalimantan/Sumatra) to processing & demand hubs in Java, and

- From Java to eastern Indonesia (Sulawesi, Maluku, Papua).

3.3 Transport Modes and Key Corridors

3.3.1 Primary Transport Modes

- Sea Freight (Coastal & Inter-Island)

- Main mode for high-volume aluminium movements:

- Bauxite → refineries

- Alumina → smelters

- Ingots/billets → downstream plants

- Finished products → outer islands or export markets

- Road Transport (Truck)

- Port → factory, factory → distributor, distributor → project sites.

- Dominant mode in Java and Sumatra due to extensive toll road network.

- Rail

- Limited role for aluminium; used in some corridors on Java but far less significant than road + sea.

3.3.2 Critical Corridors

- Kalimantan → Java

- Alumina and sometimes semi-finished products shipped to downstream processors.

- North Sumatra (INALUM) → Java & Sumatra customers

- Primary ingots/billets distributed to extruders and rolling mills.

- Java main ports (Tanjung Priok, Tanjung Perak) → Eastern Indonesia

- Aluminium products shipped to Makassar, Ambon, Papua, and other ports for construction & infrastructure.

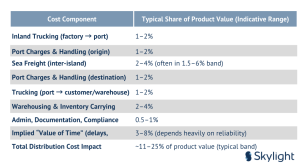

3.4 Distribution Cost Structure for Aluminium

3.4.1 Macro Picture: Indonesia’s High Logistics Cost Environment

Indonesia is widely recognised as a high-logistics-cost economy:

- Numerous studies and market reports estimate that logistics costs account for around 23–27% of GDP, much higher than in many competing countries.

- World Bank analysis shows that for shipping goods from Java to eastern Indonesia, sea freight itself is only about 1.5–6% of the value of goods, while the “value of time” (delay, waiting, inventory in transit) can reach up to 18% of goods value, making time and reliability a bigger cost component than pure transport.

- For manufacturers, transport + container handling represents about 40% of total logistics cost, with the rest split between inventory, warehousing, and admin.

For aluminium, which is relatively high value per tonne but heavy and bulky, these ratios are highly relevant.

3.4.2 Typical Cost Components for Aluminium Movements

When shipping aluminium (ingots, billets, coils, profiles) from upstream regions to Java or from Java to eastern Indonesia, cost components commonly include:

- Inland Trucking (Mine/Plant → Port)

- Port Handling & Terminal Charges

- Sea Freight (Inter-Island)

- Port Handling at Receiving Port

- Port → Warehouse/Factory Trucking

- Warehousing & Inventory Carrying Cost

3.4.3 Illustrative Cost Breakdown for Aluminium Shipment

Below is an illustrative scenario (not a contract rate) for a tonne of aluminium products shipped from North Sumatra or Kalimantan to Java and then distributed regionally. Values are expressed as percentage of product value, inspired by the logistics structure found in the World Bank freight logistics study.

Key insights from this structure:

- Sea freight is not the biggest cost; time delays and multi-stage handling dominate.

- For long routes (e.g., Java → eastern Indonesia), value of time + handling can equal or exceed the freight cost itself.

- For aluminium, such distribution costs can compress margins or push manufacturers to favour domestic suppliers closer to end markets, even if smelter ex-works prices are slightly higher.

- Upstream Distribution Costs: Bauxite → Alumina → Smelter

At the upstream level:

- Bauxite transport involves hauling ore on relatively poor roads, followed by barge/ship to refineries.

- Alumina transport to smelters, when they are not integrated on the same site,

Key cost drivers:

- Road quality and distance from mine to port (fuel, truck wear, time).

- Port capability (bulk conveyor vs manual) — determines handling cost and loading speed.

- Bulk shipping rates, which are influenced by route distance and vessel size.

- Inventory in transit, as alumina is bulky and requires specialised handling.

For smelter economics, each additional logistics step between mine, refinery, and smelter directly raises the cost per tonne of primary aluminium and can be the difference between being competitive vs needing import supplementation.

3.6 Downstream & Commercial Distribution Costs

For downstream aluminium products (profiles, coils, flat sheets, foils), the dominant flows are:

- From smelters + billet makers → extruders/rolling mills

- From extruders/rolling mills → national distributors & fabricators

- From distributors → construction and industrial sites

Here cost drivers include:

- Truck transport: often short haul but frequent.

- Multi-tier distribution margins: producer → national distributor → regional dealer →

- Inventory levels: distributors often carry substantial stock of popular profiles, adding carrying cost but ensuring availability.

- Service level & credit terms: extended credit effectively adds financial cost to the supply chain.

In practice, for many construction-grade profiles, distribution & handling can add 10–20% on top of factory price, depending on distance, volume, and channel structure, which is consistent with the macro logistics cost ranges cited earlier.

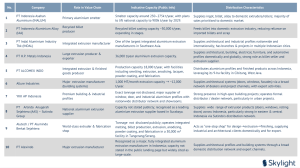

3.7 Top 10 Major Aluminium Producers / Suppliers Acting as Key Distributors

Indonesia does not publish an official “Top 10 Aluminium Distributors” list. However, based on publicly available information, we can identify major aluminium producers and suppliers that:

- Have significant production capacity,

- Operate nationwide distribution or partner networks, and

- Play a key role in supplying the domestic market.

Below is an analytical list (not an official ranking), focusing on companies whose products and networks are central to aluminium distribution in Indonesia.

3.7.1 Summary Table

Major Players in the Industry

4.1 Upstream & Smelting Segment (Primary Metal Producers)

This is the most strategic part of the aluminium value chain because primary aluminium smelting is capital- intensive, energy-intensive, and sets the foundation for downstream industry.

Indonesia has one dominant smelter, supported by new projects coming online.

- PT Indonesia Asahan Aluminium (INALUM) — The Backbone of National Supply

Type: State-Owned Enterprise (Part of MIND ID)

Core Role: Indonesia’s only primary aluminium producer

Estimated Capacity: ~250,000–275,000 tonnes of aluminium per year

Products: Aluminium ingots, billets, and alloys

Why INALUM is Important:

- It supplies the majority of Indonesia’s domestic primary aluminium.

- Acts as the stabiliser for national aluminium prices.

- Supports downstream extrusion, rolling, and automotive manufacturers.

- Holds strategic reserves for national industrial needs.

Future Outlook:

Indonesia plans to increase national smelting capacity toward 900,000 tonnes per year by 2029, driven by new smelter investments in Kalimantan and Sumatra. INALUM remains the anchor for this expansion.

- PT Indonesia Aluminium Alloy (IAA)

Type: Joint venture (Recycled billet producer)

Capacity: ~30,000 tonnes/year

Products: Recycled aluminium billets

Strategic Role:

- Provides a domestic supply alternative to imported billets.

- Supports sustainability by strengthening aluminium recycling.

- Critical for extruders needing consistent billet supply.

- Major Industrial Groups Investing in New Upstream Projects

Several large companies are now entering the upstream and midstream space:

A. Harita Group / PT Cita Mineral / PT Well Harvest Winning Alumina Refinery

- Owns/refines bauxite in West Kalimantan.

- Supplies alumina for future smelting expansions.

B. Bauxite & Alumina Projects in Bulungan (North Kalimantan Industrial Park)

- Large-scale integrated renewable-powered cluster.

- Planned smelters targeting regional export markets.

C. China-backed Industrial Zones

- Investors from China are bringing technology and capital to accelerate Indonesia’s refining & smelting roadmap.

Strategic Insight:

These players will fundamentally reshape Indonesia’s upstream landscape over the next 5–10 years, reducing import dependency.

4.2 Downstream Industrial Manufacturers (Rolling, Extrusion, Foil)

Downstream aluminium producers transform ingots/billets into usable products such as sheets, coils, extrusions, and foils. These players form the economic core of the industry, meeting the needs of construction, automotive, packaging, and manufacturing sectors.

4.2.1 Major Extrusion Producers

- PT Indal Aluminium Industry Tbk (INDAL) Type: Public Company

Segment: Extrusions, fabrication, building systems

Scale: One of the largest in Southeast Asia

Importance:

- Strong presence in construction (doors, windows, curtain walls).

- Long-term supplier for commercial and industrial projects.

- Runs nationwide dealer networks and project-based distribution.

- PT HP Metals Indonesia

Segment: Extrusions for architecture, furniture, automotive

Capacity: ~36,000 tonnes/year

Strengths:

- Large domestic client base

- Strong export capability

- Competitive quality for industrial applications

- PT Alcomex Indo

Segment: Integrated extrusion (from billet to finished products)

Capacity: ~18,000 tonnes/year

Strengths:

- Large integrated plant in West Java

- In-house anodizing, powder coating, and finishing

- Strong presence in both project and retail markets

- Allure Industries

Segment: Premium architectural aluminium systems

Capacity: ~12,000 tonnes/year

Strengths:

- Known for high-spec window & door systems

- Strong dealer network

- Focus on energy-efficient building materials

- PT Alexindo

Segment: General extrusions for construction

Importance:

- One of Indonesia’s oldest and most widely recognized brands

- Strong distribution network throughout Java and Sumatra

- PT Alutech (Alumindo Berkat Sejahtera)

Segment: Extrusions + finishing + industrial components

Importance:

- Provides both architectural and industrial extrusions

- Strong fabrication capabilities for OEM customers

4.2.2 Major Rolling & Flat Products Manufacturers

- PT Taman Alumindo

Products: Aluminium sheets, coils, plates

Role: Serves roofing, packaging, signboards, general manufacturing

- PT Alumindo Light Metal Industry (ALMI) Products: Aluminium sheet & foil Importance:

- Key player in the packaging sector

- Supplier for food & beverage converters

4.2.3 Foil & Packaging Producers

- Foil Indonesia Group (various subsidiaries)

Products: Household foil, packaging foil, pharmaceutical foil

- Converters that use aluminium foil

(Though not primary aluminium players, they form a critical part of the value chain.)

4.3 National Distributors & Trading Houses

While manufacturers produce the aluminium, distribution networks decide who gets the product, where, and at what price. These companies play a crucial role in market reach:

- Sutindo Group (PT Arlindo Anugerah Sejahtera)

Role: One of Indonesia’s biggest building-material distribution groups with major strengths such as:

- Deep penetration in eastern Indonesia

- Carries multiple aluminium brands

- Strong warehousing infrastructure

- Mega Baja / Hitec / Multi brands

(Regional distributors of aluminium profiles, roofing, and sheets.) These companies allow aluminium products to penetrate smaller cities.

- Import-based Distributors

Some distributors bring in:

- Aluminium coils

- Billets

- Sheets

- Special alloys

To supply automotive and electronics manufacturers.

4.4 International Players Influencing Indonesia’s Market

Indonesia’s aluminium market is not isolated. Several global players indirectly influence Indonesia through investment and trade:

- Chinese Aluminium Groups

- Major investors in smelting projects

- Technology and capital providers

- Middle Eastern Aluminium Producers

- Exporters of ingots and billets to Indonesia

- Often more competitive on energy cost

- Australian, Indian, and Malaysian Producers

- Export alumina or billets

- Compete with Indonesian domestic suppliers

4.5 Competitive Landscape Overview

- Upstream

- Remarkably high barrier to entry

- Dominated by INALUM and foreign-invested smelter projects

- Energy cost is the key determinant of competitiveness

- Midstream

- Expanding due to government downstreaming push

- New refineries and smelters expected to increase domestic supply

- Downstream

- Highly competitive

- Many brands, significant retail presence

- Differentiation via coating, finishing, quality consistency, delivery speed

- Distribution

- Dominated by long-standing networks

- Market influence based on inventory availability and project access

- Upstream

4.6 Strategic Insights: What These Major Players Mean for Indonesia

- The Industry is Dual-Core: INALUM + Downstream Fabricators

- Downstream is More Dynamic Than Upstream

- New Smelters Will Reshape the Market

- Competition Will Shift to Value-Added Products

- Distribution Power Is a Strategic Advantage

Companies with the strongest channels (Sutindo, Indal, Alexindo, YKK AP, etc.) play a critical role in shaping nationwide availability and pricing.

Production, Export, and Import Statistics of Aluminum

5.1 Overview of Aluminium Flow (2020–2025)

Indonesia’s aluminium ecosystem can be summarised in four simple points:

- Production is stable but limited

- Smelting capacity is ~250–275k tonnes/year with moderate improvements each year.

- Consumption keeps rising

- Demand from construction, packaging, automotive, and industrial sectors pushes annual consumption above 550–600k tonnes/year by 2025.

- Imports fill the gap

- Because domestic output cannot meet demand, Indonesia imports billets, ingots, coils, and special alloys.

- Exports remain small

- Most aluminium stays within Indonesia to support downstream manufacturing.

This mismatch between supply and demand helps explain the country’s downstream-driven growth but also its cost vulnerability.

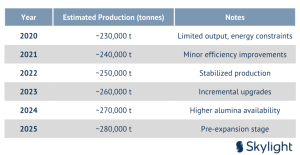

5.2 Estimated Primary Aluminium Production (2020–2025) (Production of ingots, billets, alloys from domestic smelting)

Key Insight:

Production rises slowly because smelting is extremely energy intensive.

New large-scale smelters will only begin contributing significantly after 2026–2030.

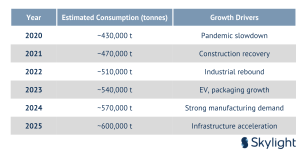

5.3 Estimated Domestic Consumption (2020–2025) (Demand from construction, automotive, packaging, and manufacturing)

Key Insight:

Domestic demand grows much faster than production.

By 2025, Indonesia uses ~2.1× more aluminium than it produces.

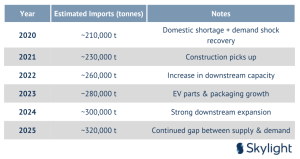

5.4 Estimated Import Requirements (2020–2025) (Billets, ingots, coils, foil stock, special alloys) Imports exist because domestic production cannot meet the needs of downstream processors. Import Quantity Estimate

Key Insight:

Despite rising alumina output, Indonesia remains import-dependent due to:

- High electricity cost of smelting

- Limited number of smelters

- Fast-growing downstream deman

5.5 Estimated Export Volumes (2020–2025) (Semi-finished aluminium exports to ASEAN & Asia)

Although Indonesia is a net importer, some downstream products (extrusions, roofing sheets, architectural profiles) are exported.

Key Insight:

Indonesia exports downstream products, not primary aluminium. This aligns with the government’s downstreaming policy.

5.6 Structural Observations (2020–2025)

- Production Stagnates, Consumption Surges

- Import Dependency Becomes Structural

- Export Growth Comes from Downstream, Not Upstream

- Pricing Volatility Affects Local Industry

- New Refining & Smelting Projects Will Change the Landscape (after 2026+)

5.7 Strategic Insight Summary

- Indonesia consumes more aluminium than it produces, making it a high-potential market.

- Imports will remain essential until large new smelters come online.

- Downstream processors (extruders, rolling mills, foil producers) drive most domestic economic value.

- Export competitiveness improves as Indonesia focuses on finished/semi-finished aluminium products.

- The 2026–2030 period is expected to shift Indonesia from a supply-constrained to a production- expanding nation.

Indonesia’s aluminium sector stands on the edge of a rare transformation. The country has the raw materials, the strategic geography, the industrial demand, and the political will to become one of Asia’s most influential aluminium hubs. The next five years will determine whether Indonesia remains a demand-driven, import-heavy market or rises into a fully integrated, globally competitive aluminium powerhouse. The opportunity is real, the momentum is building, and the players who act now will define the shape of Indonesia’s aluminium future for decades to come.

Potential Challenge and Structural Issues in Indonesia

Indonesia’s aluminium industry is positioned for long-term growth, but the road ahead is filled with structural challenges that could slow down progress or increase production costs. These challenges exist at every stage of the value chain—from mining and logistics to refining, smelting, and downstream manufacturing.

Understanding these obstacles is vital because every major investment decision, cost structure, and policy design is shaped by them.

This chapter presents the 10 most critical challenges facing the industry, each explained clearly and connected with its strategic impact.

6.1 Energy Availability & High-Power Cost

“No cheap power = no competitive aluminium.”

Aluminium smelting is one of the most energy-intensive industrial processes on earth. Electricity alone represents

30–40% of total smelting cost. Indonesia faces three key issues:

- Electricity prices are relatively high compared to global smelting hubs.

- Smelters require stable, large-scale baseload power, not intermittent supply.

- Renewable energy integration is still in initial stages.

Without major improvements in power availability and cost, Indonesia may struggle to match the competitiveness of:

- China

- India

- Middle Eastern smelting clusters (powered by cheap gas)

Strategic risk:

If power remains expensive, Indonesia’s smelting expansion could stall or operate at higher-than-global cost.

6.2 Logistics Complexity & High Distribution Costs

The country’s geography makes logistics inherently difficult:

- Many mines and refineries are located in remote areas of Kalimantan and Sumatra.

- Downstream plants and end users are mostly in Java.

- Shipments involve multiple legs: trucking → port → shipping → port →

This results in:

- High transportation costs

- Long lead times

- High inventory costs

- Uncertain delivery reliability

Delays and inefficiencies can add up to 11–25% to the final value of aluminium products.

Strategic risk:

Indonesia’s aluminium products may remain less competitive if domestic logistics are not streamlined.

6.3 Slow Development of Smelting Capacity

Indonesia has large bauxite reserves and growing alumina refining capacity, but smelting growth is slow because:

- Smelting is capital-intensive

- Requires long-term power supply agreements

- Needs advanced technology partnerships

- Faces regulatory requirements and environmental standards

While new smelter plans are announced, major capacity additions often take 5–7 years to materialize.

Strategic risk:

Growth of downstream industries may outpace upstream development, increasing dependence on imported aluminium.

6.4 Environmental & Sustainability Pressures

Global buyers increasingly demand low-carbon aluminium. This creates pressure in three areas:

- Mining practices — rehabilitation, responsible land management

- Energy sources — preference for renewable-powered smelting

- Traceability — end-to-end data on environmental footprint

Countries like Canada, Norway, and the Middle East are moving fast into “green aluminium.” Strategic risk:

If Indonesia cannot meet global ESG requirements, it will lose export opportunities in Europe and premium markets.

6.5 Technology Gaps in High-End Aluminium Products

Indonesia’s aluminium manufacturers are strong in general-purpose products, but still limited in advanced categories:

- Aerospace-grade alloys

- EV-grade aluminium parts

- High-conductivity alloys for battery systems

- High-tolerance extrusions

- Micro-thin aluminium foils

Developing these capabilities requires:

- Advanced metallurgical technology

- Precision extrusion/rolling equipment

- Skilled labor

- R&D investment

Strategic risk:

Indonesia may miss out on fast-growing, high-value aluminium markets.

6.6 Regulatory Changes & Policy Uncertainty

The aluminium industry, especially upstream, is heavily affected by government policies:

- Export bans on bauxite

- Downstream value-add requirements

- Changes in import tariffs

- Power pricing regulations

- Permitting processes for industrial estates

Strategic risk:

Investment delays or cancellations, particularly in smelting and refining projects.

6.7 Competition from Established Global Producers

Indonesia competes against countries with:

- Cheaper energy

- Larger smelting clusters

- More advanced technology

- Stronger export networks

Major competitors include:

- China (low cost, massive scale)

- India (growing rapidly)

- UAE, Bahrain, Oman (cheap gas, premium aluminium)

- Russia (low power cost)

Strategic risk:

Indonesia must position itself carefully to avoid being squeezed out of export markets.

6.8 Skills Gap & Workforce Readiness

Advanced aluminium production requires:

- Metallurgical engineers

- Automation experts

- Skilled extrusion/rolling technicians

- Quality-control specialists

Indonesia still faces shortages in high-skill labour for:

- Alloy development

- Precision extrusion

- Casting technology

- Digital manufacturing

Strategic risk:

Slow efficiency improvement and dependence on foreign workforce in early project phases.

6.9 Capital Intensity & Access to Long-Term Financing

Smelters, rolling mills, and advanced extrusion plants require billions of dollars in investment. Challenges include:

- Long payback periods

- Need for multi-decade power agreements

- Global commodity price volatility

- High upfront infrastructure costs

Strategic risk:

Expansion may remain slower than demand growth.

6.10 Challenge 10 — Uneven Development Across the Archipelago

Java is highly developed. Other regions are not. This creates:

- Regional supply gaps

- Higher prices in eastern Indonesia

- Unequal economic benefits

- Inefficient movement of aluminium between regions

Strategic risk:

Uneven development undermines the goal of a fully integrated national aluminium industry.

Indonesia’s aluminium industry faces significant challenges—but none are insurmountable. In fact, every challenge also represents an opportunity. High logistics cost can be solved with better industrial zones. Technology gaps can be filled with global partnerships. Smelting constraints can be overcome through renewable-powered industrial clusters. If Indonesia addresses these challenges wisely, the country will not only secure domestic aluminium independence but could rise to become Southeast Asia’s strongest aluminium powerhouse. The world’s demand for aluminium is accelerating—and Indonesia is one of the few nations with the resources, market size, and industrial ambition to lead the next decade.

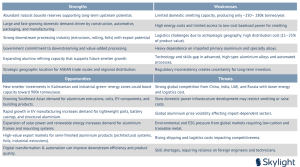

6.11 SWOT MATRIX — INDONESIA’S ALUMINIUM INDUSTRY

Benchmark and Common Practices

Indonesia’s aluminium industry does not operate in isolation. To assess its competitiveness, it is essential to benchmark the country against major global aluminium-producing and aluminium-consuming regions: ASEAN, the European Union (EU), and the United States (USA).

This comparison highlights where Indonesia currently stands, where it excels, and where significant improvement is needed.

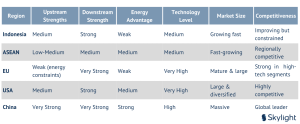

7.1 Benchmark Summary Table (High-Level Comparison)

7.2 Indonesia vs ASEAN

Upstream (Mining, Alumina, Smelting)

- Indonesia is the only ASEAN country with large-scale bauxite reserves and significant alumina refining.

- Indonesia also has the largest smelting ambition in the region.

ASEAN peers:

- Malaysia, Thailand, Vietnam: mostly downstream processing; limited upstream resources.

- Singapore: entirely downstream trade & processing.

Competitive insight:

Indonesia holds a clear upstream advantage in ASEAN but lacks the smelting scale of China.

Downstream (Extrusions, Rolling, Foils)

Indonesia’s advantage:

- Indonesia has some of Southeast Asia’s largest extrusion manufacturers (Indal, HP Metals, Alexindo, Etc)

- Strong building and automotive component segments.

ASEAN competition:

- Thailand has strong automotive extrusion capabilities.

- Vietnam is emerging in rolled products.

Competitive insight:

Indonesia is top tier in ASEAN for downstream processing but faces rising competition from Vietnam and Thailand.

Energy & Logistics

- Indonesia: energy costs high, logistics complex (inter-island).

- Malaysia, Thailand, Vietnam: more compact geography, lower logistics friction.

Competitive insight:

Indonesia’s logistics cost is ASEAN’s biggest disadvantage.

7.3 Indonesia vs European Union (EU)

Upstream

- EU has minimal bauxite and declining smelting due to high energy costs.

- Indonesia is stronger upstream, with natural reserves and refining potential. Downstream

EU’s downstream capabilities are:

- Highly advanced

- Technology-intensive

- High precision

- Dominant in aerospace, automotive, and high-end industrial aluminium

Competitive insight:

EU outperforms Indonesia in technology, quality, and advanced alloys, but struggles with upstream supply and energy cost.

Sustainability & ESG EU requires:

- Low-carbon aluminium

- Traceability

- Responsible mining

- Circularity and recycling standards

Indonesia:

- Improving ESG but not yet at EU-level compliance.

Competitive insight:

To penetrate EU markets, Indonesia must strengthen ESG and carbon reporting.

7.4 Indonesia vs United States (USA)

Upstream

- USA has strong smelting history, but many plants shut down due to high energy cost.

- Similar to the EU, the USA depends heavily on imported aluminium and alumina.

Indonesia is stronger in upstream potential, but the USA has:

- Better energy reliability

- Better R&D infrastructure

- Better financial and technological support for smelting modernization

Downstream

The USA has:

- Large, advanced rolling mills

- Automotive-grade extrusion capacity

- Aerospace alloy expertise

Indonesia lacks:

- High-end alloys

- Aerospace-grade material

- Battery-grade advanced aluminium products Market Size

USA market is one of the largest aluminium consumers globally, especially in:

- Automotive

- Construction

- Packaging

- Aerospace

- Military & industrial sectors

Indonesia’s market is growing fast but is still mid-sized in comparison.

Competitive insight:

Indonesia can grow rapidly but needs decades of investment to match USA’s advanced ecosystem.

7.5 Market Orientation Benchmark (What Each Region Focuses On)

Indonesia

- Building materials

- Automotive parts

- Rolled products

- Packaging foil

- Construction profiles

ASEAN

- Automotive

- Packaging

- General manufacturing

EU

- Aerospace

- EV lightweighting

- High-end engineering components

- Ultra-thin foil technology

USA

- Military-grade aluminium

- Aerospace & aviation

- Automotive lightweighting

- Advanced engineering alloys

7.6 Insights: Where Indonesia Stands Today

- Better than ASEAN in upstream capability, but weaker in logistics.

- Comparable to ASEAN in downstream strength, with some sectors leading.

- Stronger than EU & USA in natural resources, but far behind in technology.

- Energy cost is Indonesia’s biggest disadvantage globally.

- Downstream potential is Indonesia’s biggest advantage, especially for export.

- If smelting capacity reaches 900,000 tonnes/year by 2029, Indonesia will leapfrog ASEAN and approach global mid-tier producer status.

Indonesia is neither behind nor ahead of the world—it stands at a powerful midpoint. Strong in resources, strong in demand, strong in downstream potential. Weak in energy, weak in logistics, weak in advanced technology. How Indonesia acts in the next 5 years will decide whether it stays a downstream-driven market or rises into a globally relevant aluminium powerhouse.

Writer’s Opinion

Indonesia’s aluminium industry sits at a pivotal crossroads where its natural advantages, industrial ambition, and regional positioning intersect with structural weaknesses that must be addressed to unlock its full potential. At the upstream level, Indonesia holds abundant bauxite reserves and a growing alumina refining capacity, giving it a natural foundation that most countries in ASEAN lack. Yet despite this strong footing, the country has not yet developed the large-scale, cost-efficient smelting capability needed to achieve true industrial sovereignty.

The result is a persistent gap between what Indonesia can produce and what it actually needs. Today, domestic demand exceeds 600,000 tonnes per year, while production capacity still hovers around 250,000 to 280,000 tonnes. This imbalance forces the country to rely heavily on imported billets, ingots, and coils, creating long-term vulnerabilities in pricing, supply security, and competitiveness. In essence, Indonesia has the raw potential to lead, but not yet the industrial engine to fully capitalize on that potential.

- Indonesia produces less than half of the aluminium it consumes.

- Downstream manufacturers are already ASEAN leaders in extrusions and construction systems.

- Smelting requires 30–40% energy cost, making Indonesia less competitive.

- Logistics inefficiencies add 11–25% to final aluminium product costs.

- ESG compliance will determine future access to EU and US markets.

- Indonesia lacks high-end aluminium technology for aerospace and EV-grade alloys.

- Indonesia has the potential to become ASEAN’s aluminium hub with proper strategy.

This contrast becomes even more visible when examining the downstream sector, which is arguably Indonesia’s strongest asset. The country has developed one of the most dynamic aluminium downstream industries in ASEAN. Companies in extrusion, rolling, and foil manufacturing have matured significantly, serving a wide range of sectors including construction, automotive, packaging, and consumer goods.

This downstream growth is not only robust but strategically important. It generates higher value per tonne of aluminium and creates broad spillover effects across the economy. Indonesia’s strength lies in its ability to produce value-added aluminium products that feed into real, growing domestic markets. The industry’s core competency is not in smelting, but in transforming aluminium into finished systems and industrial components. This downstream positioning is unique because it gives Indonesia a competitive advantage even in the absence of large-scale smelting.

This downstream-led structure, however, exposes Indonesia to significant risks. Because local smelting output is insufficient, downstream manufacturers must source a substantial portion of their raw material from abroad. As a result, the industry’s cost structure is heavily influenced by external forces. Imported aluminium leaves Indonesia vulnerable to global price volatility, fluctuating foreign exchange rates, and changes in shipping costs. Downstream manufacturers do not just compete on production quality—they compete on their ability to manage supply-chain risks.

For Indonesia to achieve long-term stability, smelting expansion must become a national priority. Without a reliable domestic supply of primary aluminium, downstream growth will remain constrained, and pricing will remain unpredictable. This is why several industry stakeholders consistently highlight the need for a strategic, long-term plan to accelerate smelter development.

One of the most critical elements shaping Indonesia’s aluminium trajectory is the cost of energy. Smelting is extraordinarily energy-intensive, and electricity accounts for as much as 30–40% of overall production cost. Countries such as China, India, and the United Arab Emirates dominate global smelting largely because they enjoy low-cost coal, gas, or hydroelectricity. Indonesia, however, faces significantly higher industrial power tariffs and inconsistent availability of baseload power near mining and refining zones.

This reality places Indonesia at a competitive disadvantage and explains why downstream growth has outpaced smelting expansion. To attract large investments in smelting, Indonesia must establish industrial clusters with long- term, low-cost, and renewable energy solutions. Industrial parks in North Kalimantan and Sumatra are promising steps, but these initiatives must be scaled up and integrated with national energy planning.

Compounding the energy challenge is Indonesia’s logistical complexity. The country’s geography, while rich in natural resources, complicates logistics with multiple inter-island routes involving trucking, port handling, and sea freight. This increases transportation cost significantly, often adding 11–25% to the final cost of aluminium products.

These logistics challenges are structural—they cannot be solved through small interventions. They require coordinated improvements in port infrastructure, industrial zoning, and supply-chain integration. Without such systemic improvements, Indonesia’s aluminium products will face continued competitiveness pressure compared to countries with smoother logistics ecosystems.

Another strategic dimension shaping Indonesia’s aluminium future is the rapid rise of ESG and low-carbon requirements worldwide. Global buyers, especially in the EU and US, are no longer treating environmental sustainability as an optional advantage—it has become a prerequisite for market entry. As the world shifts toward “green aluminium,” producers must demonstrate responsible mining, renewable-powered smelting, traceable production chains, and strong recycling initiatives.

This emerging reality presents both a challenge and an opportunity for Indonesia. If the country continues with coal- reliant smelting, it may struggle to penetrate premium export markets. But if Indonesia accelerates investments into hydro- and renewable-powered smelting clusters, it could produce competitively priced low-carbon aluminium and secure a unique position in the global supply chain.

Equally important is the country’s current technological capability. Indonesia has strong capacity in general-purpose aluminium products, but it still lacks expertise in high-end segments such as aerospace-grade alloys, EV battery casings, high-tolerance industrial extrusions, and ultra-thin foil. These advanced applications require world-class metallurgy, precision equipment, and automated production lines—capabilities that Indonesia has yet to fully develop. The gap is not merely technological; it is also human. Indonesia needs more metallurgists, extrusion specialists, industrial designers, and quality engineers. Without a significant upgrade in talent development and R&D investment, the country risks being locked into mid-tier aluminium production while missing out on high-value markets.

Despite these challenges, Indonesia’s regional position presents a powerful opportunity. Within ASEAN, Indonesia holds the strongest combination of resources, industrial capacity, and market size. Thailand may be strong in automotive aluminium, and Vietnam may be rising in rolled products, but no ASEAN country matches Indonesia’s integrated potential. With proper strategic direction, Indonesia can establish itself as the regional hub for aluminium processing and value-added exports. Such leadership would not only strengthen Indonesia’s domestic economy but also enhance its geopolitical influence within Southeast Asia’s industrial ecosystem.

Ultimately, the direction of Indonesia’s aluminium industry will be determined by several key decisions made over the next five years. The country must decide whether it will secure low-cost energy to support smelting expansion, invest heavily in advanced downstream technologies, modernize its logistics infrastructure, and fully align with global sustainability standards. These decisions are not isolated—they are interconnected. Energy influences smelting: smelting influences downstream cost; logistics influence competitiveness; ESG influences export markets. Together, they form the architecture of Indonesia’s aluminium future.

If Indonesia addresses these structural constraints with decisive action, it can transition from an import-dependent aluminium market into a truly competitive, fully integrated aluminium powerhouse. The global demand for aluminium— driven by electric vehicles, solar energy, construction, and lightweight manufacturing—is growing rapidly, and Indonesia is one of the few nations that possesses the natural resources, market size, and industrial ambition to lead this next phase. The opportunity is significant. The momentum is building. The question is whether Indonesia is ready to execute.

Conclusion

Indonesia’s aluminium industry stands at a decisive turning point where its natural strengths, industrial ambitions, and economic transformations meet significant structural constraints. Throughout this report, it becomes clear that Indonesia possesses a rare combination of competitive advantages: abundant mineral resources, a rapidly growing domestic market, and one of the most robust downstream aluminium processing sectors in Southeast Asia. These factors position Indonesia uniquely for long-term industrial leadership. However, the country must confront enduring challenges — particularly in smelting capacity, energy costs, logistics efficiency, and technological sophistication — before it can fully realize its potential.

The country’s upstream foundation is strong in terms of geological resources yet limited in terms of actual smelting capacity. Domestic production remains far below domestic demand, forcing Indonesia to rely heavily on imports. This structural gap exposes the industry to fluctuating global aluminium prices, currency volatility, and fragile international supply chains. As highlighted throughout the analysis, Indonesia currently produces less than half of the aluminium it consumes, leaving downstream manufacturers dependent on imported billets, ingots, and coils. This dependency not only increases production costs but limits the nation’s ability to stabilize local pricing or assert influence over regional aluminium markets.

Despite this upstream constraint, Indonesia’s downstream aluminium industry continues to perform exceptionally well. The country has established strong capabilities in extrusion, rolling, architectural systems, automotive components, and packaging materials. These sectors have grown consistently due to rising domestic consumption across construction, infrastructure, manufacturing, and consumer goods. What stands out is that Indonesia’s competitive advantage lies not in producing raw aluminium but in transforming aluminium into high value finished products, a position that supports both domestic industries and export potential. This downstream engine offers Indonesia a strategic edge, especially as global demand for lightweight materials accelerates.

Yet downstream success also magnifies upstream vulnerability. Being forced to source raw aluminium from abroad reduces Indonesia’s competitiveness and constrains its ability to scale downstream output. To fully unlock the country’s aluminium potential, smelting capacity must become a national industrial priority. Expanding smelting operations requires addressing several interconnected issues, the most critical being energy availability and cost. Aluminium smelting is highly energy-intensive, and electricity typically accounts for 30–40% of total production cost. Indonesia’s current industrial power tariffs are still relatively high compared to global smelting hubs such as China, India, and the Middle East. Unless Indonesia can provide secure, low-cost, and preferably renewable energy for smelters, large-scale upstream expansion will remain challenging.

Logistics pose another major structural barrier. Indonesia’s archipelagic geography creates a multi-stage logistics chain — truck → port → ship → port → truck — that adds significant cost and time to aluminium distribution. Logistics inefficiencies can add between 11% and 25% to the final cost of aluminium products, eroding competitiveness and slowing supply-chain responsiveness. A modern, integrated logistics ecosystem is therefore essential for the aluminium industry to operate efficiently and at scale.

In addition to energy and logistics constraints, Indonesia must adapt to global environmental expectations. Sustainability, traceability, and low-carbon aluminium are no longer optional; they have become prerequisites for entering premium markets, especially in the European Union and United States. For Indonesia, this represents both a challenge and an opportunity.

If the country continues relying on fossil-fuel-based smelting, it risks losing access to ESG-sensitive markets. Conversely, if Indonesia accelerates renewable-powered smelting — particularly through hydro-based industrial zones — it can position itself as a future supplier of green aluminium, a category that is rapidly gaining global relevance and price premiums.

Technological capability also requires significant improvement. Indonesia remains strong in general-purpose aluminium but lags behind global leaders in advanced alloys, aerospace materials, EV components, and ultra-thin foil. Developing these high-value segments will require targeted investment in R&D, industrial automation, metallurgical innovation, and specialized workforce development. Without such advancements, Indonesia risks being locked into mid-tier production while global demand shifts toward higher-precision aluminium applications.

Benchmarking against ASEAN, the EU, and the USA reinforces these insights. Indonesia is the strongest player in ASEAN in terms of resource availability and downstream processing, but it lags behind its regional peers in logistics efficiency and technological specialization. Compared with the EU and USA, Indonesia is significantly weaker in environmental compliance, advanced manufacturing capabilities, and product sophistication, yet it enjoys advantages in resource availability and domestic demand that the EU and USA no longer possess. These comparative strengths and weaknesses highlight the strategic choices Indonesia must make in the coming decade.

Ultimately, the future of Indonesia’s aluminium industry hinges on several key decisions that will shape the next phase of national industrial development. These include:

- Whether Indonesia can secure low-cost, reliable energy to make smelting economically competitive.

- Whether the country can modernize logistics infrastructure to reduce supply-chain inefficiencies.

- Whether downstream industries will invest in advanced technology and move into higher-value aluminium segments.

- Whether Indonesia will fully adopt world-class ESG practices to access global premium markets.

These decisions are deeply interconnected. Improvements in energy policy influence smelting investment; smelting influences downstream cost; logistics influence national competitiveness; and ESG determines access to global markets.

If Indonesia acts decisively, the country has the potential to evolve from an import-dependent aluminium consumer into a fully integrated aluminium powerhouse. The global aluminium industry is entering a period of extraordinary growth, driven by electric vehicles, renewable energy, sustainable construction, and advanced packaging. Few countries in the world have both the natural resources and the industrial base to capture these emerging opportunities. Indonesia does. The question now is not whether Indonesia can lead, but whether it will choose to take the steps necessary to do so.

The moment is now. With bold strategic execution, Indonesia can become the aluminium hub of Southeast Asia, a major global supplier of value-added aluminium, and a cornerstone of regional industrial strength. The potential is enormous — but the decision to unlock it lies ahead.

Sources

- International Aluminium (2025). Aluminium statistical yearbook 2020–2025. https://international-aluminium.org

- World Bureau of Metal Statistics. (2025). World metal statistics yearbook: Aluminium balance 2020–2025.

- United States Geological Survey. (2025). Mineral commodity summaries: Bauxite and alumina 2020–2025. https://www.usgs.gov

- Asian Development Bank. (2025). Indonesia infrastructure and logistics development report 2020– 2025. https://www.adb.org

- Ministry of Energy and Mineral Resources (ESDM). (2025). Annual mineral and coal mining report 2020–2025. https://esdm.go.id

- Ministry of Industry (Kemenperin). (2025). Aluminium industry development statistics 2020–2025. https://kemenperin.go.id

- Indonesia Investment Coordinating Board (BKPM). (2025). Investment realization and industrial cluster development reports. https://bkpm.go.id

- PT Indonesia Asahan Aluminium (INALUM). (2025). Annual reports and sustainability disclosures 2020–2025. https://inalum.id

- Harita Group. (2025). Well Harvest Winning alumina refinery project publications 2020–2025. https://harita.com

- International Energy Agency. (2025). Global aluminium energy consumption trends 2020–2025. https://iea.org

- World Bank Group. (2025). Indonesia economic update and manufacturing sector analysis 2020– 2025. https://worldbank.org

- ASEAN Secretariat. (2025). Intra-ASEAN metal trade and industrial cooperation report 2020– 2025. https://asean.org

- European Aluminium Association. (2025). Sustainability and low-carbon aluminium standards. https://european-aluminium.eu

- United States Department of Commerce. (2025). Aluminium import monitoring and analysis reports. https://www.commerce.gov

- CRU Group. (2025). Global aluminium market forecasts and smelting cost analysis 2020–2025.

- Fitch Solutions. (2025). Indonesia metals & mining outlook 2020–2025.

- McKinsey & Company. (2024). Global aluminium demand outlook and EV market impact. https://mckinsey.com

- Deloitte (2025). Metals sector outlook: Decarbonization and market shifts. https://www2.deloitte.com

- Badan Pusat Statistik. (2025). Indonesia trade statistics for HS 7601–7616 (Aluminium and articles thereof). https://bps.go.id

- Indal Aluminium Industry Tbk. (2025). Annual report and product catalogue.

- PT HP Metals Indonesia. (2025). Corporate publications and capacity overview.

- Allure Industries. (2025). Product specifications and architectural aluminium systems report.

- PT Alexindo. (2025). Corporate catalogue and national distribution portfolio.

- PT Alcomex Indo. (2025). Manufacturing capabilities and technical profile.

- PT Alumindo Light Metal Industry. (2025). Annual company filings.

- United Nations Comtrade Database. (2025). Global aluminium trade records 2020–2025. https://comtrade.un.org

- International Trade (2025). World aluminium trade analysis 2020–2025. https://www.trademap.org

- London Metal (2025). Historical aluminium price data 2020–2025. https://www.lme.com

- Various authors. (2020–2025). Articles from Journal of Materials Processing Technology, Materials Science Forum – Aluminium Alloys, and Journal of Light Metals and Manufacturing.