By Hendry Santoso, Market Research and FS

Preface

1.1 The pulp and paper industry as a strategic pillar of Indonesia’s economy

The pulp and paper industry constitutes one of Indonesia’s most strategically significant manufacturing sectors, combining large-scale industrial production with renewable natural resource utilization. Unlike many extractive industries, the sector is anchored in managed forestry systems, positioning it at the intersection of industrial policy, land-use planning, export competitiveness, and environmental governance.

From a macroeconomic perspective, the pulp and paper industry contributes approximately 1.3–1.5% of Indonesia’s Gross Domestic Product (GDP) on a direct basis. When upstream forestry activities, downstream converting industries (packaging and tissue), logistics, energy generation, and supporting services are included, the sector’s total economic footprint is substantially larger. Within manufacturing, pulp and paper accounts for an estimated 6–7% of total manufacturing GDP, placing it among the most important non-oil and gas industrial contributors.

In terms of external trade, pulp and paper products generate USD 7–10 billion in annual export revenues, making the sector one of Indonesia’s largest sources of foreign exchange outside the mineral and energy complex. The industry’s ability to combine renewable inputs, scale efficiency, and export orientation gives it a structurally important role in Indonesia’s long-term economic architecture.

1.2 Forestry land base as the foundation of pulp and paper production

1.2.1 Indonesia’s national forest estate

Indonesia has one of the largest forest estates globally, with a legally designated forest area of approximately 120 million hectares. This area is administratively classified into conservation forests, protection forests, and production forests. The pulp and paper industry operates almost exclusively within the production forest category, through licenses granted for Industrial Plantation Forests (Hutan Tanaman Industri – HTI).

The availability, productivity, and governance of HTI land directly determine the sector’s capacity, competitiveness, and sustainability profile.

1.2.2 Industrial Plantation Forest (HTI) allocation and utilization

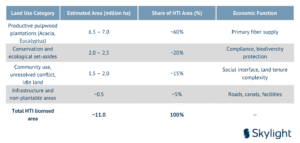

Although Indonesia’s total licensed HTI area is estimated at approximately 11 million hectares, only a portion of this land is actively planted and productive. The remainder includes conservation set-asides, community-use areas, land under dispute, and non- plantable infrastructure zones.

Table 1.1 – Utilization of Industrial Plantation Forest (HTI) Land in Indonesia

Analytical implication:

Only about three-fifths of licensed HTI land directly contributes to fiber production. This highlights the importance of land productivity, plantation yield optimization, and governance clarity for sustaining industrial output without continuous land expansion.

1.3 Geographic concentration of pulpwood plantations in Indonesia

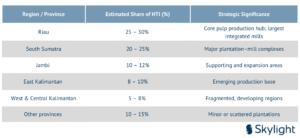

Pulpwood plantations in Indonesia are highly geographically concentrated, reflecting ecological suitability, historical investment patterns, and proximity to major pulp mills and export ports. Approximately 75–80% of Indonesia’s HTI area supplying pulp and paper is concentrated in a limited number of provinces.

Table 1.2 – Estimated Regional Distribution of HTI for Pulp & Paper

Analytical implication:

This concentration means that regional governance capacity—particularly in Sumatra and Kalimantan—plays a decisive role in determining the industry’s national performance, ESG outcomes, and investment risk profile.

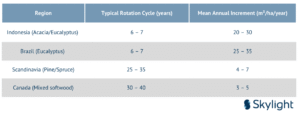

1.4 Land productivity and international competitiveness

Indonesia’s competitiveness in pulp production is strongly linked to biological productivity, rather than land area alone. Tropical plantation species such as Acacia and Eucalyptus exhibit rapid growth rates, enabling short harvesting cycles and high fiber yields.

Table 1.3 – Comparative Forestry Productivity (Selected Regions)

High productivity allows Indonesian producers to achieve globally competitive pulp cash costs, support very large mill capacities, and maintain export competitiveness. At the same time, the scale of production magnifies environmental and social risks, increasing scrutiny from regulators and international markets.

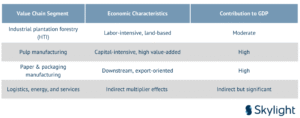

1.5 Decomposing the industry’s contribution to Indonesia’s GDP

The pulp and paper industry contributes to Indonesia’s GDP through multiple interconnected

layers, each with distinct economic characteristics.

Table 1.4 – GDP Contribution by Value Chain Segment

Combined, these segments account for:

- 1.3–1.5% of national GDP,

- ~6–7% of manufacturing GDP,

- A substantial share of Indonesia’s non-oil manufacturing

1.6 Forestry land use, climate exposure, and national trade-offs

Indonesia’s pulp and paper industry embodies a structural trade-off between economic contribution and land-use sensitivity. A significant portion of plantation forestry overlaps with peatland landscapes, which are among the world’s most carbon-dense ecosystems.

This has historically linked the sector to:

- Greenhouse gas emissions from land-use change,

- Peat drainage and fire risk,

- Biodiversity

In response, government policy and corporate practices have increasingly emphasized:

- Peatland protection and restoration,

- Zero-deforestation commitments,

- Stricter land-use

These measures directly affect the industry’s cost structure, expansion potential, and long- term contribution to GDP.

1.7 Strategic positioning within Indonesia’s long-term development framework

The pulp and paper sector occupies a unique position in Indonesia’s economic strategy:

- It is renewable based, unlike mining,

- Export-oriented, unlike many agricultural sectors,

- Capital-intensive, yet employment-generating,

- Deeply embedded in regional land-use systems.

Future contributions to GDP and exports will depend less on expanding land area and more on:

- Improving plantation productivity,

- Increasing downstream value addition (packaging, specialty paper),

- Integrating bioenergy and circular economy practices,

- Maintaining international market confidence through credible ESG

1.8 Analytical foundation for subsequent chapters

This report treats forestry land use as a core economic variable, not a background condition. The spatial distribution, productivity, and governance of HTI land underpin:

- Market supply capacity,

- Cost competitiveness,

- Environmental performance, and

- Indonesia’s international

Subsequent chapters will therefore build directly on this foundation, linking market trends, capacity expansion, trade flows, and policy dynamics to the forestry base described above.

Market Trends and Size of Pulp and Paper in Indonesia

2.1 Global pulp and paper market: scale and structural context

The global pulp and paper industry remains one of the largest manufacturing sectors in the world, despite long-term structural changes driven by digitalization and sustainability pressures. As of the 2020–2025 period, global output averages:

- Paper and paperboard: approximately 420–430 million tonnes per year

- Total pulp production: approximately 185–195 million tonnes per year, of which

- Market pulp: around 70–75 million tonnes per year

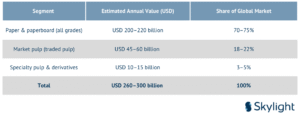

In value terms, the combined global pulp, paper, and paperboard market is estimated at approximately USD 260–300 billion annually. This wide range reflects volatility in pulp prices, energy costs, and exchange rates, particularly during the post-pandemic period.

The majority of global value is generated downstream in finished paper and packaging products. Pulp, while strategically important, acts as a price-volatile intermediate input rather than the primary value driver.

Table 2.1 – Estimated Global Pulp & Paper Market Value

2.2 Structural market trends (2020–2025): global perspective

2.2.1 Packaging paper as the dominant growth driver

Packaging paper and paperboard have become the backbone of the global pulp and paper industry. This segment now accounts for approximately 55–58% of global paper consumption and has grown at an estimated 2.5–3.5% compound annual growth rate (CAGR) between 2020 and 2025.

Growth drivers include:

- Rapid expansion of e-commerce and logistics,

- Rising consumption of packaged food and beverages,

- Regulatory pressure to replace plastic packaging with fiber-based alternatives. Packaging has therefore become the primary source of incremental market value in the global pulp and paper industry.

2.2.2 Tissue and hygiene: defensive and income-linked growth

Tissue and hygiene products account for 10–12% of global paper demand. This segment exhibits lower volatility and steady growth of approximately 2–3% per year, driven by:

- Population growth,

- Urbanization,

- Rising hygiene standards in emerging

While margins are generally lower than specialty papers, tissue provides stable demand and high-capacity utilization, making it a strategically important stabilizer for producers.

2.2.3 Graphic paper: structural decline with uneven geography

Graphic paper (newsprint, printing and writing paper) continues to decline globally at 3–5% per year. However, the pace of decline varies significantly by region:

- Rapid contraction in Europe and North America,

- Slower decline in Asia, Africa, and parts of the Middle

This uneven decline has allowed competitive producers, including Indonesia, to manage the transition by converting machines or redirecting output to export markets where demand erosion is less severe.

2.3 Indonesia’s pulp and paper market: size, structure, and growth dynamics

2.3.1 Total market size in Indonesia (USD)

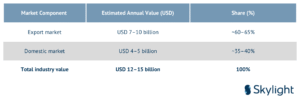

Indonesia’s pulp and paper industry generates an estimated USD 12–15 billion in annual output value, making it one of the largest manufacturing sectors in the country outside oil, gas, and basic commodities.

This value is composed of:

- USD 7–10 billion from exports, and

- USD 4–5 billion from domestic sales.

Table 2.2 – Estimated Indonesia Pulp & Paper Market Size

Key insight:

Indonesia’s pulp and paper industry is export-led by structure, not by short-term strategy. Domestic demand is growing but remains secondary in scale.

2.3.2 Indonesia’s domestic pulp and paper market

Indonesia’s domestic pulp and paper consumption is driven primarily by:

- Packaging for food and beverages,

- Consumer goods packaging,

- Tissue and hygiene products,

- Commercial and institutional uses.

Per-capita paper consumption in Indonesia remains significantly below developed economies, indicating long-term domestic growth potential. However, domestic demand growth has been moderate during 2020–2025, averaging approximately 2–3% per year, constrained by:

- Income levels,

- Digitization,

- Efficiency improvements in packaging use.

Domestic market value is estimated at USD 4–5 billion annually, with packaging and tissue accounting for the majority.

2.4 Indonesia’s export market: scale and composition

2.4.1 Export structure by product category

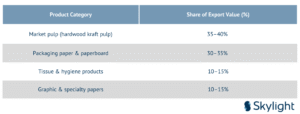

Indonesia’s pulp and paper exports are concentrated in a small number of high-volume categories.

Table 2.3 – Estimated Indonesia Pulp & Paper Export Composition

Export destinations are geographically diversified, with Asia accounting for the largest share, followed by the Middle East, Africa, and selective markets in Europe and North America.

2.4.2 Indonesia’s global market share

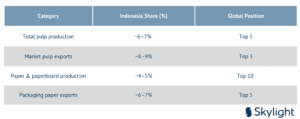

Indonesia holds a meaningful position in the global pulp and paper market, particularly in export-oriented segments.

Table 2.4 – Indonesia’s Estimated Global Market Share

Indonesia’s influence is therefore disproportionately strong in global trade flows, even if its domestic consumption share is relatively small.

2.5 Indonesia in the ASEAN pulp and paper market

2.5.1 ASEAN market size

The ASEAN pulp and paper market—including domestic consumption and exports—is estimated to be worth approximately USD 35–45 billion annually. Demand is driven by:

- Population growth,

- Industrialization,

- Rising consumer goods

2.5.2 Indonesia’s dominance within ASEAN

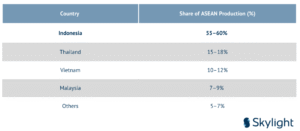

Indonesia is the dominant pulp and paper producer in ASEAN, accounting for more than half of regional output.

Table 2.5 – ASEAN Pulp & Paper Production Share

In value terms, Indonesia’s pulp and paper activities represent approximately USD 20–25 billion equivalent of ASEAN’s total pulp and paper production and trade ecosystem.

2.6 Indonesia’s market trend (2020–2025): internal dynamics

2.6.1 Shift toward packaging and downstream products

Between 2020 and 2025, Indonesia’s pulp and paper industry has:

- Expanded packaging paper capacity,

- Invested in converting and corrugated board facilities,

- Gradually reduced exposure to declining graphic paper segments.

This shift has resulted in:

- More stable revenues,

- Better alignment with domestic and regional demand trends,

- Improved resilience against global pulp price cycles.

2.6.2 Impact of cost volatility and ESG compliance

Indonesia’s market performance during this period was shaped by:

- Rising energy and chemical costs,

- Logistics disruptions during and after COVID-19,

- Increased ESG compliance costs related to forestry, peatland protection, and traceability

Despite these pressures, Indonesia’s integrated plantation-to-mill model helped maintain competitiveness relative to higher-cost producers.

2.7 Effective market size and growth ceiling for Indonesia

While headline global demand remains strong, Indonesia’s effective market size is constrained by:

- Limits on plantation land expansion,

- Regulatory and ESG requirements,

- Capital intensity of new capacity

As a result, Indonesia’s pulp and paper industry is transitioning from volume-driven growth to value-driven growth, where:

- Productivity gains,

- Product mix optimization,

- Downstream integration

become more important than capacity expansion.

2.8 Forward-looking market outlook (Indonesia-focused)

Looking beyond 2025, Indonesia’s pulp and paper market is expected to experience:

- Volume growth of 1–2% per year,

- Value growth of 2–4% per year, driven by packaging and higher-value products,

- Continued dominance in ASEAN,

- Stable global market share with selective gains in Indonesia’s future market size will therefore be shaped less by land availability and more by efficiency, sustainability, and strategic positioning within global supply chains.

2.9 Executive Synthesis: Indonesia Market Trend, Size, and Effective Economic Footprint

Indonesia’s pulp and paper market is frequently assessed through headline indicators such as production tonnage or export value. While these metrics are important, they do not fully capture the true scale, resilience, and strategic reach of the industry. A more accurate understanding emerges when domestic demand composition, export geography, price dynamics, and ASEAN-level leverage are examined together.

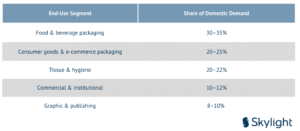

Domestic demand: structurally resilient and function-driven

Indonesia’s domestic pulp and paper demand is concentrated in non-discretionary, functional uses, rather than in declining publishing applications. Packaging for food and beverages, consumer goods, logistics, and hygiene products account for the majority of domestic consumption. As a result, domestic demand has shown steady growth of approximately 2–3% per year during 2020–2025, even as graphic paper consumption continues to decline structurally.

Table 2.10 – Indonesia Domestic Paper Demand by End-Use

This demand structure makes Indonesia’s internal market more stable and predictable than headline paper statistics often suggest, providing a reliable base load for industry capacity utilization.

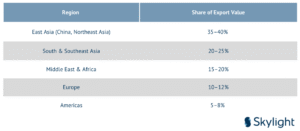

Export markets: Asia-centered with strategic diversification

Exports account for approximately 60–65% of Indonesia’s total pulp and paper market value, equivalent to USD 7–10 billion annually. Export value is strongly anchored in Asian markets—particularly East Asia—while Europe and North America function as smaller but strategically important destinations due to their higher sustainability standards and reputational influence.

Table 2.11 – Indicative Indonesia Pulp & Paper Export Value by Region

This geographic diversification reduces demand concentration risk while simultaneously anchoring Indonesia’s industry within Asia’s long-term consumption growth corridor.

Price cycles and value realization (2020–2025)

During the 2020–2025 period, Indonesia’s market size in value terms was shaped more by price movements and product mix than by volume expansion. Hardwood pulp prices experienced pronounced upcycles and corrections, amplifying export revenues during favorable periods. However, Indonesia’s vertically integrated plantation–pulp–paper structure mitigated volatility by allowing internal pulp absorption during downturns.

Packaging grades demonstrated stronger cost pass-through and faster margin recovery compared to graphic papers, reinforcing packaging as the primary value stabilizer of the industry.

ASEAN dominance expands Indonesia’s effective market

Indonesia’s role extends beyond national borders. With approximately 55–60% of ASEAN pulp and paper production, Indonesia functions as the region’s dominant supply hub. Neighboring producers such as Thailand and Vietnam—despite rapid growth—remain partially dependent on imported pulp and certain paper grades, often sourced from Indonesia.

Effective market size: beyond headline industry value

While Indonesia’s direct pulp and paper industry output is valued at approximately USD 12– 15 billion per year, this figure understates the sector’s broader economic footprint. When downstream packaging conversion, regional trade influence, logistics, and converting activities are included, Indonesia’s effective pulp and paper ecosystem value is closer to USD 18–22 billion equivalent.

These reframing highlights that future growth will be driven less by physical expansion and more by:

- Downstream upgrading,

- Packaging and converting capacity,

- Logistics efficiency,

- and ASEAN-centered trade

Pulp and paper industry is transitioning into a mature, value-optimized industrial phase.

Major Players in the Industries

3.1 Structural nature of the pulp and paper industry: why company structure matters

The pulp and paper industry is inherently shaped by scale economics, land control, and long investment horizons. Unlike fast-cycle manufacturing sectors, pulp and paper investments typically involve:

- Plantation rotations of 6–7 years (tropical hardwood),

- Pulp mills with economic lives exceeding 30–40 years,

- Capital expenditure per greenfield mill often exceeding USD 2–3 billion.

As a result, industry structure is path-dependent: early movers with access to land, capital, and political alignment consolidate power over time. Indonesia is a textbook case of this dynamic. The current corporate landscape reflects decisions made decades earlier regarding land allocation, concession policy, and industrial integration.

This has produced an industry that is:

- Highly concentrated,

- Dominated by domestic corporate groups, and

- Vertically integrated to a degree uncommon in most countries.

3.1.2 Typology of companies operating in Indonesia’s pulp and paper sector

Companies involved in Indonesia’s pulp and paper sector can be categorized into four structural types, each with distinct economic roles and risk profiles.

3.2.1 Type A – Fully integrated domestic conglomerates (systemic players)

These companies control:

- Industrial plantation forests (HTI),

- Pulp production,

- Paper/packaging manufacturing,

- Energy generation (biomass),

- Export logistics.

They define national capacity, exports, and global perception.

Key characteristics:

- Extremely high capital intensity

- Long-term land exposure

- Direct ESG and policy sensitivity

- Disproportionate influence on national statistics

3.2.2 Type B – Domestic downstream producers (paper & packaging focused)

These firms:

- Operate paper, packaging, or specialty mills,

- Source pulp internally or from domestic suppliers,

- Focus more on domestic and regional

They contribute to:

- Market depth,

- Domestic supply stability,

- Value-added manufacturing

3.2.3 Type C – Foreign multinationals (non-asset owners)

Foreign companies rarely own pulp assets in Indonesia. Instead, they influence the market through:

- Long-term offtake contracts,

- Pricing benchmarks,

- Technology and machinery supply,

- Downstream competition in export markets.

3.2.4 Type D – Ancillary and enabling players

This includes:

- Equipment suppliers,

- Chemical companies,

- Logistics and port operators,

- Certification and auditing bodies.

While not producers, they shape cost curves, compliance burdens, and operational standards.

3.3 Dominant domestic conglomerates: ownership, control, and scale

- Asia Pulp & Paper (APP)

Ownership and origin

- Ultimate parent: Sinar Mas Group

- Country of origin: Indonesia

- Holding structure: multinational, with offshore finance vehicles

Operational footprint

- Multiple pulp mills and paper machines across Sumatra and Java

- Extensive HTI plantation base

- Product portfolio spanning:

- market pulp,

- packaging paper,

- tissue,

- specialty and cultural papers

Strategic role

APP is not only Indonesia’s largest pulp and paper producer, but also one of the most influential global suppliers. Its decisions on capacity utilization, grade mix, and export allocation have measurable effects on regional pulp prices and packaging availability.

- APRIL Group

Ownership and origin

- Ultimate parent: Royal Golden Eagle (RGE) Group

- Country of origin: Indonesia / Singapore

- Holding structure: international, commodity-focused

Operational footprint

- One of the world’s largest single-line hardwood pulp mills

- Highly productive plantation base

- Export-oriented, especially toward China and Northeast Asia

Strategic role

APRIL is best understood as a pulp system specialist. While historically focused on market pulp, its strategic importance lies in supplying a large share of Asia’s hardwood pulp demand and anchoring Indonesia’s role in global pulp trade.

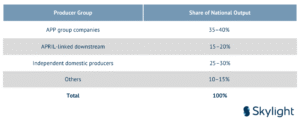

3.4 Market share and concentration in Indonesia

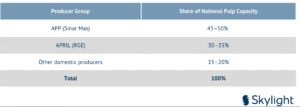

3.4.1 Pulp capacity concentration

Table 3.1 – Estimated Pulp Capacity Share in Indonesia

This level of concentration places Indonesia among the most concentrated pulp industries globally, comparable only to Brazil’s eucalyptus pulp sector.

3.4.2 Paper and packaging production share

Table 3.2 – Estimated Paper & Packaging Production Share

Interpretation:

While pulp is extremely concentrated, paper and packaging show slightly greater fragmentation, reflecting downstream specialization and domestic market participation.

3.5 Domestic downstream producers: stabilizers of the internal market

Domestic downstream companies play a critical role in:

- Absorbing domestic pulp output,

- Reducing reliance on imports,

- Serving Indonesia’s growing packaging and tissue

Examples include:

- Indah Kiat Pulp & Paper

- Tjiwi Kimia

- Fajar Surya Wisesa

Although smaller than the integrated giants, these firms:

- Improve market resilience,

- Support SME packaging ecosystems,

- Enhance downstream value capture.

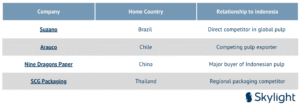

3.6 Foreign companies: influence without ownership

Foreign multinational companies are structurally important but asset-light in Indonesia.

Table 3.3 Key foreign competitors and buyers

Foreign firms shape:

- Benchmark prices,

- Quality standards,

- ESG expectations,

- Long-term demand

3.7 Vertical integration and risk concentration

Indonesia’s integrated model creates both advantage and vulnerability.

Advantages

- Lowest quartile fiber costs globally

- Energy self-sufficiency through biomass

- Strong export logistics control

Risks

- ESG issues scale nationally

- Policy shocks affect large portions of output

- Land conflicts concentrate reputational risk

This duality explains why Indonesia’s pulp and paper industry is both globally competitive and globally scrutinized.

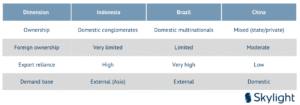

3.8 Comparative ownership models: Indonesia vs peers

Table 3.4 Ownership and Structure Comparison

Indonesia’s model emphasizes national control of strategic assets but concentrates responsibility for sustainability and governance within domestic firms.

3.9 Strategic implications for policy and competition

- Systemic importance: Decisions by two groups affect GDP, exports, and land use

- Policy leverage: Government policy has strong leverage—but also high stakes.

- ESG as national branding: Company behavior influences “Indonesia origin” perception globally.

- Limited contestability High barriers to entry reduce competition but stabilize long-term investment.

3.10 Structural outlook (2025–2035)

Over the next decade, Indonesia’s pulp and paper industry structure is likely to:

- Remain highly concentrated,

- Shift capital toward packaging and downstream conversion,

- Face increasing carbon and land-use scrutiny,

- Prioritize productivity and legitimacy over expansion.

Total Production, Export, Import and Potential Issues

4.1 Purpose and analytical framing of this chapter

This chapter consolidates global supply–demand context and national statistics into a single Indonesia-focused production and trade analysis. Rather than treating Indonesia as one data point among many countries, the chapter positions Indonesia as a structural supplier in the global and ASEAN pulp and paper system, where production, export, and import patterns reveal deeper insights about competitiveness, industrial maturity, and strategic constraints.

The period 2020–2025 is particularly significant because it captures:

- The COVID-19 shock and recovery,

- Major pulp price cycles,

- Acceleration of packaging demand,

- Tightening ESG and land-use constraints,

- and Indonesia’s transition from volume-driven to value-driven growth.

4.2 Total pulp and paper production in Indonesia

4.2.1 National production scale and composition

Indonesia is one of the world’s largest pulp and paper producers, with total annual production

during 2020–2025 estimated at:

- Pulp: ~12–13 million tonnes per year

- Paper & paperboard: ~15–16 million tonnes per year

This places Indonesia among the top five global pulp producers, and within the top ten global paper and paperboard producers.

Unlike many countries where pulp and paper output is primarily consumed domestically, Indonesia’s production structure is export-oriented by design, reflecting its role as a fiber and packaging supplier to international markets.

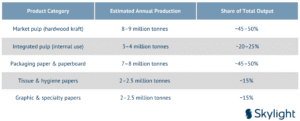

4.2.2 Production structure by product category

Table 4.1 – Indonesia Pulp & Paper Production Structure

Analytical insight:

Indonesia’s production is structurally biased toward exportable and scalable products— pulp and packaging—rather than specialty or domestic-only grades. This explains both its strong trade surplus and its exposure to global price cycles.

4.3 Export performance: Indonesia as a structural surplus producer

4.3.1 Total export volume and value

Between 2020 and 2025, Indonesia exported approximately:

- 7–8 million tonnes of pulp annually, and

- 7–8 million tonnes of paper and paperboard annually.

In value terms, this corresponds to:

- USD 7–10 billion per year in pulp and paper exports, depending on price cycles

- ~60–65% of total pulp output, and

- ~50–55% of paper & paperboard production.

This confirms Indonesia’s position as a net structural exporter, rather than a balanced or consumption-led producer.

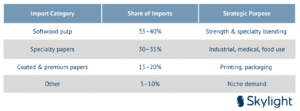

4.4 Import profile: limited but strategically important

Despite its large domestic industry, Indonesia imports certain pulp and paper products, primarily to meet:

- Specialty paper requirements,

- Short fiber/softwood pulp needs,

- Niche industrial and consumer

Annual imports during 2020–2025 are estimated at:

- 1–1.5 million tonnes per year,

- Valued at USD 0–1.5 billion annually.

Table 4.2 – Indonesia Pulp & Paper Imports by Type

Key insight:

Indonesia’s imports are complementary, not competitive. They enhance product range rather than substitute domestic production.

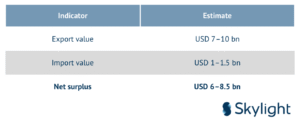

4.5 Trade balance and net export position

Table 4.3 Net trade surplus

This surplus makes pulp and paper one of Indonesia’s most important non-mineral, non- energy export industries.

4.6 Indonesia’s role in ASEAN and global trade systems

4.6.1 ASEAN anchor supplier

Indonesia supplies:

- 65–70% of ASEAN pulp production,

- 55–60% of ASEAN paper & packaging output,

- >70% of ASEAN exportable surplus.

This gives Indonesia effective regioal pricing and supply influence, particularly during global disruptions.

4.6.2 Global positioning

Globally, Indonesia accounts for approximately:

- 6–7% of total pulp production,

- 8–9% of global market pulp exports,

- 4–5% of paper & paperboard output.

Indonesia’s influence is therefore greater in trade flows than in consumption, a hallmark of a structural exporter.

4.7 Strategic implications of Indonesia’s production–trade profile

- Indonesia is a price taker in pulp, but a reliable supplier in packaging.

- Export exposure creates revenue upside—but also cyclicality

- Limited imports reinforce domestic value chains

- ASEAN dominance amplifies Indonesia’s strategic relevance

4.8 Potential Issues Affecting Indonesia’s Production and Trade Performance

While Indonesia’s pulp and paper industry demonstrates strong production capacity and a persistent trade surplus, its performance during 2020–2025 also reveals structural vulnerabilities that could materially affect future output, exports, and competitiveness. These issues are not cyclical anomalies, but systemic constraints tied to land, policy, market access, and industrial structure.

4.8.1 Forestry land constraints and fiber security

Indonesia’s pulp and paper production is ultimately constrained by the availability and productivity of industrial plantation forests (HTI). Although current fiber supply is sufficient to support existing capacity, several land-related risks persist:

- No meaningful expansion of HTI land is expected due to:

- Forest moratoriums,

- Peatland protection policies,

- Increasing land-use

- Plantation productivity gains are becoming incremental rather than

- Any disruption to plantation operations (fires, social conflict, regulatory suspension) directly impacts pulp output.

Implication:

Indonesia’s production growth is structurally capped. Future output stability depends on yield improvement and operational continuity, not land expansion.

4.8.2 ESG and deforestation-related trade risks

ESG compliance has become a binding requirement in key export markets, especially for exports to Europe and parts of North America with heightened scrutiny on land-use history, traceability, and peatland management. Even isolated incidents can trigger broad reputational and commercial impacts.

Implication:

Export volumes may remain strong, but market access risk is rising, particularly for premium markets.

4.8.3 Exposure to global pulp price cycles

As a global price taker, Indonesia benefits from pulp price upcycles but faces margin compression during downturns. Vertical integration reduces volatility but does not eliminate exposure to global supply and demand shocks.

Implication:

Export earnings are volatile even when export volumes remain stable, complicating long- term planning.

4.8.4 Energy, chemical, and logistics cost volatility

Production costs are vulnerable to fluctuations in energy prices, imported chemical inputs, and shipping costs, despite partial mitigation through biomass energy use.

Implication:

Cost inflation can erode Indonesia’s low-cost advantage, especially during weak price cycles.

4.8.5 Trade policy and non-tariff barriers

Exports increasingly face sustainability-linked regulations, carbon disclosure requirements, and environmental due diligence rules that evolve continuously and require ongoing compliance.

Implication:

Export growth is less constrained by demand and more by regulatory acceptance in destination markets.

4.8.6 Import dependence for specialty inputs

Despite being a net exporter, Indonesia relies on imported softwood pulp, specialty papers, and chemicals for higher-value production.

Any disruption to these imports can:

- Affect downstream production,

- Reduce product diversification,

- Increase cost.

Implication:

Indonesia’s trade surplus masks strategic input vulnerabilities in high-value segments.

4.8.7 Industry concentration and systemic risk

The industry is dominated by a small number of large players, enabling efficiency but amplifying the impact of operational, ESG, or policy shocks.

Implication:

The industry’s strength is also its fragility—concentration amplifies both success and failure.

4.9 Chapter conclusion

The combined analysis of production, exports, imports, and potential issues shows that Indonesia’s pulp and paper industry is globally significant yet structurally bounded. The country functions as a critical supplier to global and ASEAN markets, generating large and persistent trade surpluses. However, its future performance will hinge less on increasing output and more on:

- Sustaining fiber security,

- Maintaining ESG credibility,

- Managing cost volatility,

- Navigating evolving trade regulations.

Indonesia’s pulp and paper industry is defined by large-scale production, persistent export surpluses, and limited but strategic imports. Between 2020 and 2025, the country functioned as a global and regional supply anchor, particularly for hardwood pulp and packaging paper.

The combined production and trade data confirm that Indonesia’s competitiveness is structural, not cyclical rooted in fiber productivity, scale, and integration. However, future growth will depend less on expanding output and more on managing sustainability constraints, upgrading product mix, and preserving market access.

Government Policy

5.1 Role of government policy in the pulp and paper industry

The pulp and paper industry in Indonesia is one of the most policy-dependent industrial sectors in the country. This is because it combines three sensitive elements at once: large-scale land use, forestry resources, and export-oriented manufacturing.

Government policy therefore plays a central role in determining:

- How much fiber can be produced,

- Where plantations and mills can operate,

- What environmental standards must be met, and

- how easily products can be exported or imported

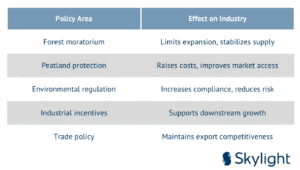

During the period 2020–2025, government policy did not aim to expand the industry aggressively. Instead, it focused on stabilizing production, tightening environmental control, and encouraging downstream value addition.

5.2 Forestry and land-use regulation

5.2.1 Industrial Plantation Forests (HTI)

Pulpwood supply in Indonesia comes mainly from Industrial Plantation Forests (HTI), which operate under long-term licenses issued by the Ministry of Environment and Forestry.

Key characteristics of HTI regulation:

- Licenses are long-term (often 60–100 years including extensions).

- Companies are required to:

- Plant only approved species,

- Protect conservation areas inside concessions,

- Engage with local communities.

This system provides long-term fiber security for pulp producers, but it also places strict obligations on land management.

5.2.2 Forest and peatland moratorium

Indonesia has implemented a permanent moratorium on new licenses in:

- Primary natural forests,

- Peatland areas.

This policy has several direct effects:

- No significant expansion of plantation land,

- Stable but capped fiber supply,

- Stronger protection of high-carbon ecosystems.

Impact on industry:

Production growth must come from higher productivity, not land expansion.

5.3 Peatland protection policies

A significant portion of Indonesia’s plantation forests is located on peatland. Because peatlands store large amounts of carbon, the government applies special rules to these areas.

Key policy requirements include:

- Maintaining minimum water table levels,

- Blocking drainage canals,

- Restoring degraded peat areas.

These rules increase operating costs, but they are essential for:

- Reducing fire risk,

- Maintaining export market acceptance,

- Aligning with Indonesia’s climate

5.4 Environmental permitting and monitoring

5.4.1 Environmental impact assessment (AMDAL)

All pulp and paper operations must hold valid environmental impact assessments (AMDAL). These permits cover:

- Plantation development,

- Mill construction,

- Waste, water, and air emissions

Failure to comply can lead to:

- Permit suspension,

- Production shutdowns,

- Export delays

5.4.2 Pollution control and waste management

Government regulation covers:

- Air emissions,

- Wastewater discharge,

- Chemical storage and

- Digital monitoring systems,

- Public reporting mechanisms,

- Stricter inspections.

5.5 Climate policy and carbon considerations

Indonesia has committed to reducing greenhouse gas emissions under its national climate targets. Forestry and land use play a major role in meeting these commitments.

For the pulp and paper industry, this means:

- Pressure to reduce emissions from land use,

- Requirements for carbon reporting,

- Preparation for possible carbon pricing in the future.

While a full carbon tax is not yet applied to the sector, carbon-related compliance costs are expected to rise gradually.

5.6 Industrial and manufacturing policy

5.6.1 Support for downstream processing

The Ministry of Industry classifies pulp and paper as a priority manufacturing sector, especially for:

- Packaging materials,

- Hygiene products,

- Downstream

- Encouraging packaging and converting industries,

- Reducing imports of finished paper products,

- Increasing domestic value

Policy direction:

Support downstream growth rather than new raw pulp capacity.

5.6.2 Domestic market considerations

Although export-oriented, pulp and paper producers are expected to:

- Supply domestic packaging needs,

- Support food, beverage, and consumer goods industries,

- Maintain product quality and safety standards.

This reinforces the industry’s role in domestic economic stability, not only exports.

5.7 Trade and export policy

5.7.1 Export facilitation

Indonesia applies relatively low tariffs to pulp and paper exports. Government policy focuses on:

- Facilitating exports,

- Maintaining access to key markets,

- Supporting compliance with international

5.7.2 Non-tariff trade barriers

The main export challenges come from:

- Sustainability requirements,

- Environmental due diligence laws,

- Carbon disclosure obligations in importing countries

The government increasingly works with industry to:

- Align certification systems,

- Improve traceability,

- Negotiate trade recognition

5.8 Import regulation

Indonesia allows imports of:

- Softwood pulp,

- Specialty and premium papers,

- Industrial paper grades not produced domestically

At the same time, policy aims to:

- Prevent dumping,

- Protect domestic packaging producers,

- encourage local production where

Imports are therefore selective and complementary, not unrestricted.

5.9 Policy enforcement challenges

Despite a comprehensive policy framework, challenges remain:

- Overlapping authority between agencies,

- Differences in enforcement capacity across regions,

- High compliance costs for smaller

These issues can create:

- Uneven playing fields,

- Uncertainty for investors,

- Reputational risks at the national level.

5.10 Overall policy impact on the industry

5.11 Policy direction going forward

Government policy is clearly moving toward:

- Stability instead of rapid expansion,

- Environmental compliance over flexibility,

- Value creation over volume growth.

For the pulp and paper industry, long-term success depends on adapting to regulation, not resisting it.

Benchmark and Common Practices

This chapter benchmarks Indonesia’s pulp & paper industry against major global reference models—Brazil, Finland, and China—to identify what Indonesia already does well, where it structurally lags, and which “common practices” matter most for competitiveness and market access.

6.1 Benchmark framework used in this chapter

To keep the comparison practical, the benchmark is structured into 8 operational dimensions that directly shape production cost, exportability, and long-term legitimacy:

- Fiber base & productivity

- Industry structure & integration

- Product mix (value-added vs commodity)

- Energy & carbon intensity

- ESG governance & traceability

- Logistics & market proximity

- Innovation & specialty capability

- Policy and enforcement consistency

6.2.Common best practices by benchmark country and what Indonesia can copy

6.2.1 Brazil benchmark: “World-class pulp cost curve discipline”

What Brazil is best at

- Ultra-high plantation productivity and continuous silviculture optimization

- Aggressive process efficiency (energy recovery, chemical recovery)

- Strong export logistics discipline (port integration, shipping optimization)

- Focused specialization (dominant in market pulp)

Best practices Indonesia can adopt

- “Productivity-first governance”: yield improvement targets at plantation block level,

- Advanced genetics + precision forestry (survival rates, rotation optimization),

- Continuous mill efficiency programs tied to global cost quartiles,

- Port/logistics integration to reduce delivered cost volatility.

Indonesia nuance: Indonesia already competes well on cost, but Brazil is the global reference on consistency and operational excellence at scale.

6.2.2 Finland benchmark: “Premiumization + traceability + circular bioeconomy”

What Finland is best at

- High share of specialty papers, premium packaging, biomaterials

- Strong national-level traceability, transparency, and enforcement

- Circular economy leadership (recycling systems, high recovered fiber utilization)

- Deep R&D (barrier coatings, fiber composites, biomaterial substitution)

Best practices Indonesia can adopt

- Shift product mix toward higher value density: specialty packaging, functional papers

- Build export-grade traceability systems (fiber-to-mill documentation culture)

- Scale circularity: water reuse, sludge valorization, byproduct monetization

- “Innovation pipelines”: industry + universities + suppliers for specialty grades

Indonesia nuance: Finland wins not on cheap fiber, but on trust + advanced products. Indonesia can’t copy the forest type but can copy governance discipline and premiumization strategy.

6.2.3 China benchmark: “Downstream demand engine + packaging ecosystem dominance”

What China is best at

- Massive domestic consumption that stabilizes demand

- Strong downstream converting and packaging ecosystem

- Speed of capacity conversion and product-market fit (fast adaptation)

- Scale-driven efficiencies across logistics and supply chains

Best practices Indonesia can adopt

- Build deeper domestic packaging ecosystems: corrugated, converting SMEs, standards

- Increase domestic absorption (reduce reliance on export cycles)

- Encourage fast conversion from lower-growth grades to packaging/specialty

- Strengthen supply chain digitalization (inventory, demand planning, shipment visibility)

6.3 Benchmark conclusion: Indonesia’s “best-fit” strategy

Indonesia is structurally strongest when it plays a dual role:

- Asia’s low-cost, reliable supplier of pulp and packaging base grades, and

- A growing regional value-added packaging hub, reducing commodity

The benchmark implies three non-negotiable priorities:

- Productivity (Brazil-style): yield + mill efficiency to maintain cost advantage

- Trust (Finland-style): traceability + governance to protect market access

- Down streaming (China-style): packaging ecosystem depth to raise value density

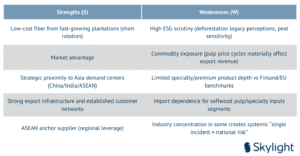

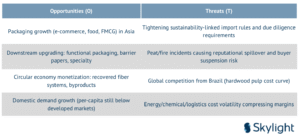

6.4 SWOT analysis for Indonesia

Table 6.2 – SWOT Matrix (Indonesia Pulp & Paper)

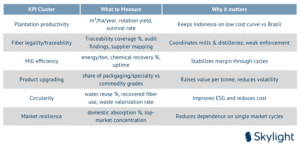

6.5 Practical benchmark KPIs Indonesia should track

Table 6.3 – KPI set aligned to benchmark best practices

Writer’s Opinion

Indonesia’s pulp and paper industry stands on a foundation that is structurally strong and difficult to replicate. Few countries possess the same combination of fast-growing plantation forests, large-scale integrated mills, and geographic proximity to Asia’s demand centers. Over the 2020–2025 period, this foundation has proven resilient through global disruptions, price cycles, and increasing regulatory pressure. In the writer’s view, this confirms that Indonesia’s pulp and paper sector is not a declining commodity industry, but a mature strategic industry entering a new phase of consolidation and upgrading.

At the same time, maturity brings limits. The era in which the industry could grow simply by expanding plantation land and building ever-larger mills is effectively over. Forest moratoriums, peatland protection, and ESG expectations have placed clear boundaries on physical expansion. These constraints should not be seen as threats, but as structural signals that Indonesia must now compete on productivity, credibility, and value creation rather than volume alone.

From an economic perspective, Indonesia’s cost advantage remains real, but it is no longer sufficient on its own. Competing producers—particularly Brazil—continue to push the global cost curve lower through genetics, silviculture, and process efficiency. Meanwhile, buyers in Europe, North America, and increasingly Asia are embedding sustainability requirements directly into purchasing decisions. In this environment, low cost without trusts risks becoming commercially irrelevant in premium markets.

Indonesia’s most important task is to protect its existing advantages while systematically reducing its vulnerabilities. This requires discipline more than ambition. The industry does not need radical transformation; it needs consistent execution across a few critical areas.

First, fiber security and productivity must remain the industry’s anchor. With no meaningful land expansion possible, the only way to sustain output is through:

- Better plantation management,

- Yield improvement,

- Fire prevention and water control, and

- Long-term concession

Failure in any of these areas directly threatens production continuity and export reliability. In contrast, success reinforces Indonesia’s position as a dependable supplier in global markets.

Second, environmental and social credibility must be treated as economic assets, not compliance costs. ESG-related investments—such as peatland restoration, traceability systems, and community engagement—often appear expensive in isolation. However, when viewed against the risk of market exclusion, buyer disengagement, or reputational damage, these investments function as insurance mechanisms that protect export revenue and industry legitimacy.

In the writer’s assessment, one of Indonesia’s biggest risks is not regulation itself, but uneven compliance and enforcement. High-performing companies may meet global standards, but isolated failures can still create negative perceptions that affect the entire national industry. This makes collective discipline and transparent reporting increasingly important.

Third, product mix upgrading is no longer optional. Heavy reliance on market pulp exposes Indonesia to price volatility and external demand shocks. While pulp will remain a core product, future value growth should increasingly come from:

- Packaging and paperboard,

- Functional and barrier papers,

- Hygiene and consumer-related products, and

- Downstream converting activitiesthese segments offer more stable demand and higher value per They also strengthen domestic and regional supply chains, reducing excessive dependence on a small number of export markets.

Fourth, domestic and asean markets deserve more strategic attention. Indonesia has historically looked outward, and this export orientation has been successful. However, rising domestic consumption and asean growth present opportunities to:

- Absorb more production locally,

- Stabilize demand through cycles, and

- Anchor the industry within regional value

A stronger domestic base does not weaken exports; it makes them more resilient. Finally, the writer views government policy as broadly supportive but execution sensitive. The policy direction—limiting land expansion, enforcing environmental standards, and encouraging downstream value addition—is strategically sound. The challenge lies in:

- Consistent enforcement,

- Regulatory clarity, and

- Coordination between

When policy is predictable and fairly enforced, the industry can plan long-term investments with confidence. When it is uneven or unclear, it increases risk premiums and discourages upgrading.

In conclusion, Indonesia’s pulp and paper industry is well-positioned but no longer in a growth-at-any-cost phase. Its future success depends on consolidation rather than expansion, trust rather than volume, and value rather than tonnage. If the industry continues to strengthen productivity, credibility, and downstream capability, it can remain a cornerstone of Indonesia’s industrial economy for decades.

The writer’s overall judgment is clear; Indonesia does not need to change what industry it has. It needs to change how that industry measures success.

Conclusion

This report has assessed Indonesia’s pulp and paper industry from multiple angles: market trends, industry structure, production and trade performance, government policy, international benchmarks, and strategic positioning. When these elements are viewed together, a consistent picture emerges. Indonesia’s pulp and paper industry is structurally strong, economically important, and globally embedded—but it is also operating within clear and tightening boundaries.

From the production and trade analysis, it is evident that Indonesia has become one of the world’s most important pulp-producing countries and a major exporter of paper and packaging products. During the 2020–2025 period, the industry consistently generated large export surpluses, contributing billions of US dollars in foreign exchange each year.

This confirms pulp and paper as one of Indonesia’s most significant non-minerals, non- energy manufacturing export sectors, with a stable role in national GDP, employment, and regional development.

The corporate structure of the industry explains much of this performance. A small number of large, vertically integrated domestic groups control most plantation land, pulp capacity, and export flows. This concentration has allowed Indonesia to achieve economies of scale, cost efficiency, and export reliability.

At the same time, it has also concentrated responsibility. Operational, environmental, or reputational issues at the company level can quickly become national-level risks, affecting the perception of Indonesian pulp and paper in global markets.

The combined production and trade data clearly show that Indonesia’s industry is export- oriented by design. More than half of pulp and paper output is shipped overseas, primarily to Asia. China, ASEAN, and other Asian markets anchor demand, while Europe and North America remain important for higher-value and sustainability-sensitive segments. This export orientation has delivered strong growth, but it also exposes the industry to global price cycles, external regulations, and shifting buyer expectations.

Government policy has played a decisive role in shaping the current industry model. Over the past decade, and especially during 2020–2025, policy direction has moved away from expansion and toward control, stability, and environmental governance.

Forest moratoriums, peatland protection, environmental permitting, and climate commitments have effectively limited land-based growth. At the same time, industrial policy has encouraged downstream processing and domestic value addition. The overall message from policy is clear: the pulp and paper industry is expected to remain important, but it must operate within strict environmental and social boundaries.

The international benchmark analysis reinforces this conclusion. Compared with Brazil, Indonesia remains competitive on cost but faces strong competition at the low end of the pulp market. Compared with Finland, Indonesia lags in specialty products, innovation, and governance transparency, but benefits from much lower fiber costs.

Compared with China, Indonesia lacks a massive domestic demand base but serves as a critical external supplier. These comparisons suggest that Indonesia’s most realistic and effective strategy is not to compete on all fronts, but to strengthen its existing advantages while selectively upgrading toward higher-value segments.

Across all chapters, one consistent theme stands out: the future of Indonesia’s pulp and paper industry is not about producing more, but about producing better. Physical expansion is constrained by land, regulation, and environmental limits. As a result, future competitiveness will depend on:

- Plantation productivity and fiber security,

- Operational efficiency and cost control,

- Environmental credibility and traceability, and

- Gradual movement toward higher-value and downstream products.

At the same time, domestic and regional markets deserve greater strategic attention. While exports will remain central, stronger domestic absorption—particularly in packaging and hygiene products—can reduce volatility and strengthen the industry’s long-term resilience. ASEAN, where Indonesia already plays a dominant role, offers additional opportunities to anchor demand closer to home.

In simple terms, Indonesia’s pulp and paper industry has already won the battle of scale, but it is now entering a phase where discipline, trust, and value creation matter more than size. The industry does not face an existential threat, but it does face a strategic choice: remain primarily a commodity exporter exposed to cycles, or evolve into a more balanced, value-driven industrial system.

In addition, this report highlights that the long-term sustainability of Indonesia’s pulp and paper industry will increasingly depend on institutional coordination and collective responsibility. Given the high level of industry concentration, outcomes are shaped not only by individual company performance but by how the sector behaves.

Strong coordination between industry players, regulators, and local communities will be critical to maintaining operational continuity, preventing environmental incidents, and preserving Indonesia’s credibility in global markets. In this context, transparency, consistent enforcement, and shared standards are not simply governance ideals—they are practical economic safeguards.

Finally, Indonesia’s pulp and paper sector should be viewed as a long-cycle strategic industry, where decisions made today will shape outcomes decades into the future. Investments in plantation management, downstream capabilities, environmental protection, and human capital may not deliver immediate returns, but they determine whether the industry remains competitive, trusted, and resilient over time.

If Indonesia continues to align industrial ambition with environmental discipline and market realities, the pulp and paper industry can remain a stable pillar of national development, supporting exports, employment, and regional growth well beyond the current planning horizon.

Sources

- Skylight Analytics Hub

- Badan Pusat Statistik. (2023). Industri manufaktur dan perdagangan luar negeri Indonesia. https://www.bps.go.id/subject/8/industri-manufaktur.html

- Badan Pusat Statistik. (2024). Statistik perdagangan luar negeri Indonesia. https://www.bps.go.id

- Brazilian Tree Industry (IBÁ). (2023). Brazilian pulp and forestry industry statistics. https://iba.org

- Confederation of European Paper Industries. (2023). Key statistics: European pulp and paper industry. https://www.cepi.org

- Food and Agriculture Organization of the United Nations. (2022). Global forest resources assessment. https://www.fao.org/forest-resources-assessment

- Food and Agriculture Organization of the United Nations. (2023). FAOSTAT forestry and pulp & paper statistics. https://www.fao.org/faostat

- Food and Agriculture Organization of the United Nations, Advisory Committee on Paper and Wood Products. (2023). World pulp and paper outlook. https://www.fao.org/forestry/industries/adv-committee-paper/en/

- International Council of Forest and Paper Associations. (2023). Sustainability progress and best practices. https://www.icfpa.org

- International Energy Agency. (2022). Energy efficiency and emissions in industry. https://www.iea.org/topics/industry

- International Labour (2023). Employment by sector: Manufacturing and forestry. https://www.ilo.org

- Kementerian Lingkungan Hidup dan Kehutanan Republik Indonesia. (2023). Statistik kehutanan Indonesia. https://www.menlhk.go.id/site/post/86/statistik-kehutanan

- Kementerian Lingkungan Hidup dan Kehutanan Republik (2022). Kebijakan moratorium hutan dan gambut. https://www.menlhk.go.id

- Kementerian Perdagangan Republik Indonesia. (2023). Peraturan dan kebijakan ekspor-impor. https://www.kemendag.go.id

- Kementerian Perindustrian Republik Indonesia. (2023). Roadmap industri pulp dan kertas nasional. https://www.kemenperin.go.id/kategori/industri-pulp-dan-kertas

- Royal Golden Eagle Group. (2023). Sustainability and ESG framework. https://www.rgei.com/sustainability

- Asia Pulp & (2023). Sustainability report. https://www.asiapulppaper.com/sustainability

- APRIL Group. (2023). Sustainability and operations report. https://www.aprilasia.com/sustainability

- United Nations Framework Convention on Climate Change. (2022). Indonesia nationally determined contribution. https://www4.unfccc.int/sites/NDCStaging/pages/Party.aspx?party=IDN

- World Bank. (2022). Indonesia: Forestry, land use, and manufacturing sector overview. https://documents.worldbank.orgWorld (2023). Global trade and industrial competitiveness reports. https://www.worldbank.org