By Hendry Santoso, Market Research and FS

Preface

The palm oil industry is a foundational sector of Indonesia’s economy, playing a critical role not only in national export revenues but also in rural livelihoods, global food security, and the renewable energy transition. As the world’s largest producer and exporter of palm oil, Indonesia has emerged as a pivotal player in shaping the global vegetable oil landscape. From 2020 to 2025, the sector has been tested by pandemic-induced shocks, environmental pressures, policy shifts, and volatile commodity prices—but has also demonstrated resilience, adaptability, and strategic evolution.

One of the defining characteristics of Indonesia’s palm oil ecosystem is its dual structure: approximately 60% of plantations are managed by large corporations, while the remaining 40% are cultivated by millions of smallholder farmers. This composition presents both strengths and challenges. On one hand, it provides inclusive economic opportunities across rural regions. On the other, it complicates issues of certification, traceability, yield consistency, and regulatory enforcement. The government’s response has included a push for widespread Indonesian Sustainable Palm Oil (ISPO) certification and digital supply chain tracking.

Indonesia’s Economy 2nd Quarter 2025

As of Q2 2025, Indonesia’s broader macroeconomic environment provides essential context for understanding the sector’s performance. The nation recorded real GDP growth of 4.94%, slightly below earlier projections and marking the lowest year-on-year quarterly growth rate since Q3 2021. The slowdown reflects moderated domestic demand and cautious global trade conditions, even as inflation remains subdued at 1.87% year-on-year (June 2025), within Bank Indonesia’s target band of 1.5–3.5%.

The Indonesian rupiah has shown sustained depreciation during the first half of 2025, with the currency stabilizing around IDR 16,000–17,000 per USD. While this depreciation raises the cost of imported goods and capital, it supports competitiveness for export sectors such as palm oil. Meanwhile, the central bank has adjusted its benchmark rate to 5.25% as of July 2025, following a cut in an effort to stimulate economic activity amid global uncertainties.

Palm oil remains a cornerstone of Indonesia’s export economy. As of H1 2025, the agriculture sector contributes approximately 13.6% of national GDP, with palm oil representing more than 40% of that share. Despite increasing scrutiny from international buyers—especially under the European Union Deforestation Regulation (EUDR)— Indonesia has maintained its role as the top global exporter, supported by efforts to accelerate ISPO compliance and traceability reforms.

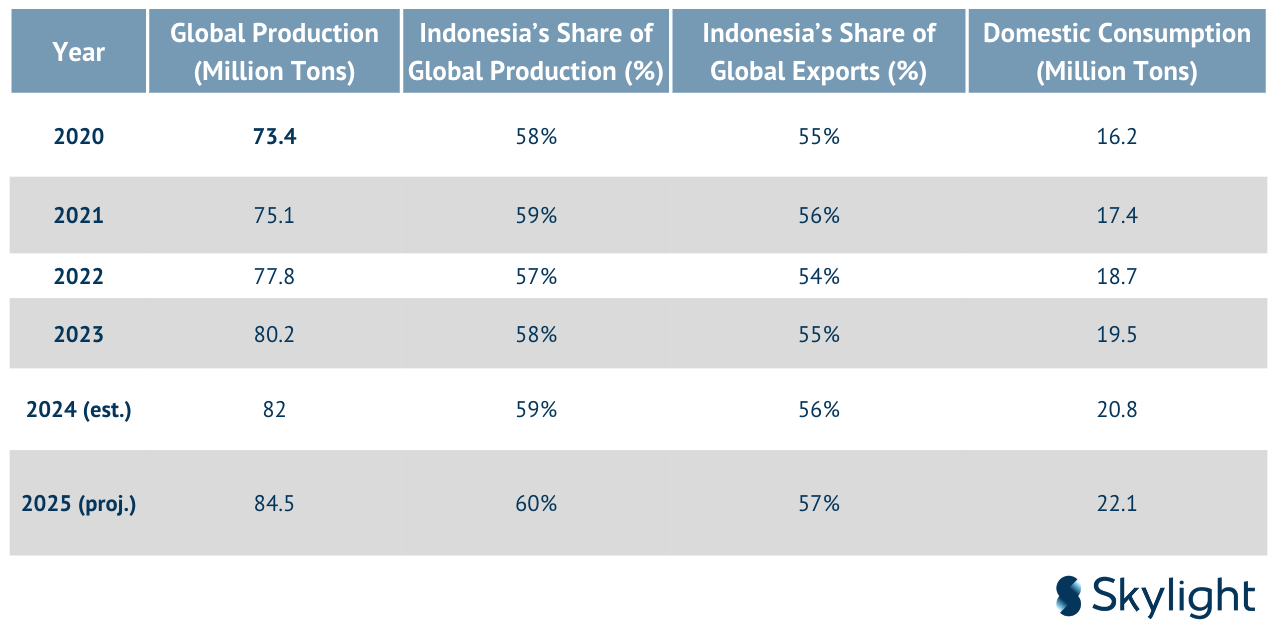

Table 1.1: Indonesia’s Share in Global Palm Oil Production and Exports (2020–2025)

This evolving macro context reinforces the critical importance of palm oil—not only as a source of growth and foreign exchange, but also as a strategic commodity navigating shifting domestic and global economic terrain. This report aims to evaluate how well the industry has adapted, what challenges remain, and where new opportunities are emerging.

Market Trends of Palm Oil in Indonesia

2.1 Overview of the Palm Oil Industry in Indonesia

The Indonesian palm oil industry has experienced dynamic growth and structural transformation from 2020 to 2025. While the COVID-19 pandemic disrupted global supply chains and demand in 2020–2021, Indonesia’s palm oil market rebounded swiftly, leveraging both external and internal growth levers. The strategic implementation of the B30 and B35 biodiesel mandates created a robust domestic demand floor, while the global supply shortage of sunflower and soybean oils—exacerbated by geopolitical tensions— heightened Indonesia’s importance as a reliable palm oil supplier.

The recovery trajectory began in earnest in 2021 with pent-up demand in the food-processing sector. From 2022 onward, export momentum strengthened, as Indonesia remained competitive despite rising scrutiny from international regulators regarding sustainability standards. Importantly, global average prices for crude palm oil (CPO) remained elevated, benefiting producers and exporters, while the weaker rupiah further enhanced the competitiveness of Indonesian palm oil in international markets.

In terms of value addition, the sector has moved steadily from primary CPO exports toward downstream products, including refined, bleached and deodorized (RBD) palm olein, stearin, biodiesel, and oleochemicals. Government policies incentivizing refinery investments, export tax adjustments, and mandatory domestic market obligations (DMO) helped rebalance domestic processing capacity and reduce volatility.

2.2 Demand Drivers

Four synergistic demand pillars have driven the expansion of the palm oil market between 2020 and 2025:

Food Industry:

Palm oil remains a cost-efficient and functional choice for food manufacturers globally. In Indonesia, household and industrial food use increased by 5.2% CAGR during this period. Demand for RBD palm olein in fast-growing African and South Asian markets has been pivotal.

Biofuels and Renewable Energy Mandates:

- The B30 mandate launched nationally in 2020 was upgraded to B35 in early

- The energy ministry forecasts biodiesel absorption to exceed 12.5 million kiloliters in

- The government’s long-term roadmap outlines a potential transition toward B40 and even B50 blending in the next decade.

Oleochemicals and Industrial Applications:

- Personal care, household detergents, lubricants, and industrial surfactants constitute a rising segment.

- Oleochemical exports from Indonesia grew from 7 million MT in 2020 to 4.9 million MT in 2024.

Supply Chain Shocks in Substitutes:

- Global disruptions to sunflower and soybean oil—especially from Ukraine and South America—pushed buyers toward palm oil.

- Palm oil’s higher productivity per hectare ensured Indonesia remained the most cost- effective supplier.

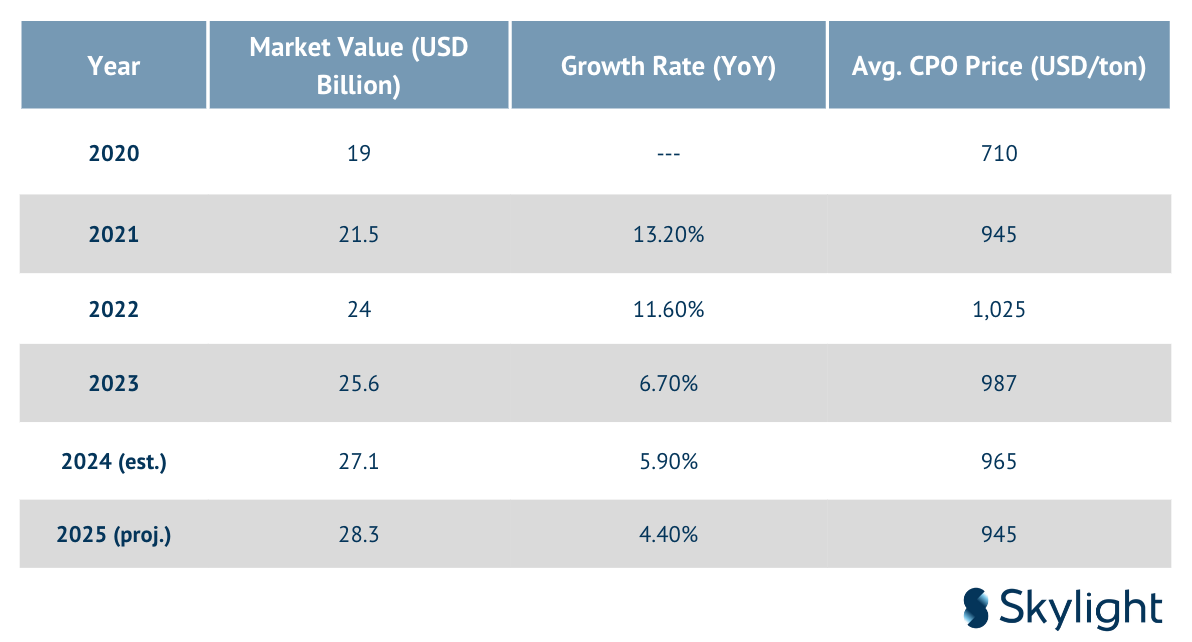

2.3 Market Size and Valuation

The market has expanded in both nominal and real terms, supported by elevated international prices, rising productivity, and diversified product offerings. Between 2020 and 2025, the estimated CAGR for the industry stands at 8.1%, significantly higher than Indonesia’s overall economic growth rate.

Table 2.1: Indonesian Palm Oil Industry Market Valuation (2020–2025)

Refined palm oil products now contribute over 62% of total export revenue, reflecting Indonesia’s push toward value chain integration.

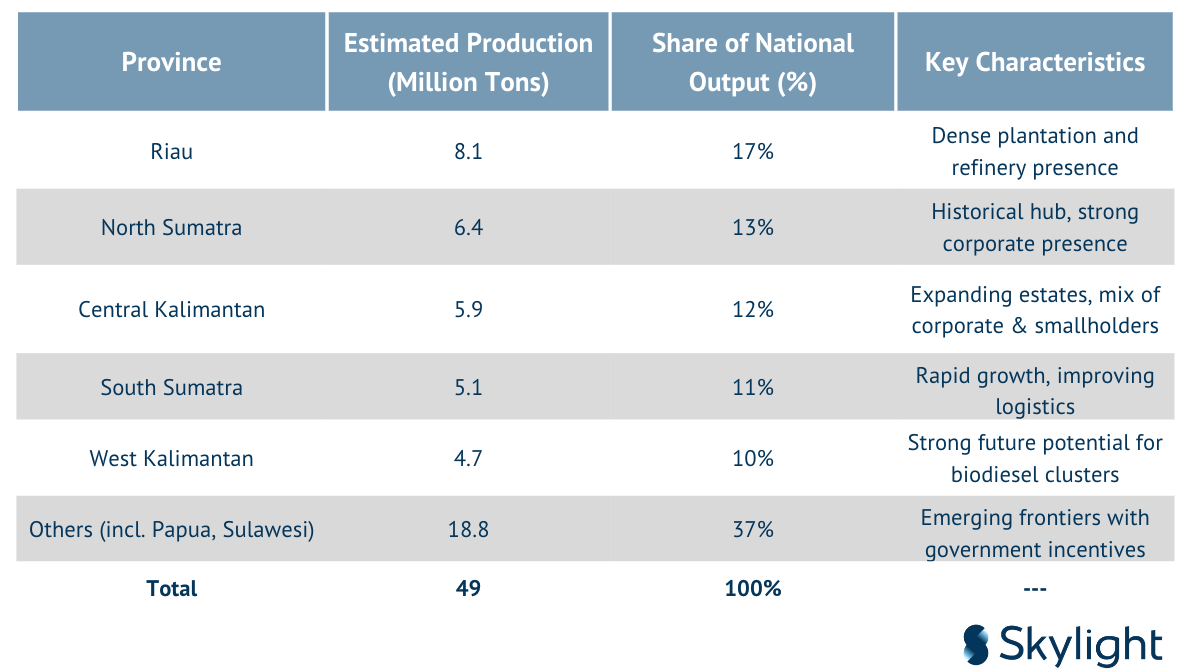

2.4 Regional Distribution and Industrial Clusters

The Indonesian palm oil landscape is geographically diverse but production is concentrated in five primary provinces. The distribution of production is shaped by plantation age, yield per hectare, infrastructure quality, and investor access.

Table 2.2: Estimated Palm Oil Production by Major Provinces (2023)

Government policy has also supported the rise of “industrial clusters”—zones of vertically integrated palm oil operations. Notable clusters include:

- Dumai-Rokan Hilir (Riau): Export gateway, refinery hub, CPO processing

- Belawan (North Sumatra): Oleochemical and biodiesel exports

- Samarinda–Balikpapan (East Kalimantan): Strategic future location given proximity to new capital (IKN)

These clusters offer logistical, tax, and export advantages—positioning Indonesia not just as a grower but as a regional processing leader.

2.5 Productivity and Technological Adoption

- Average yield in Indonesia is 6–4.1 tons/hectare/year—lower than Malaysia (4.4–4.7) due to smallholder inefficiencies.

- Digital traceability systems and satellite monitoring (e.g., SIPKEBUN) are increasingly adopted to meet global compliance.

- Government targets to replant 5 million hectares under the PSR (Peremajaan Sawit Rakyat) scheme by 2026 to boost productivity.

Major Players in the Industries

Indonesia’s palm oil sector is characterized by a significant degree of corporate concentration at the upper tier, with a relatively small number of conglomerates controlling a large portion of land and refining capacity. These corporations not only operate upstream plantations but are also heavily invested in midstream and downstream operations, including crude palm oil (CPO) refining, biodiesel production, and oleochemical manufacturing.

This vertically integrated structure enables these corporations to exert considerable influence on pricing, quality standards, export volumes, and compliance with international sustainability norms such as ISPO (Indonesian Sustainable Palm Oil) and RSPO (Roundtable on Sustainable Palm Oil).

3.2 Key Players and Holdings

Table 3.1: Leading Palm Oil Companies in Indonesia (2025)

3.3 Operational Integration

Most top-tier companies in Indonesia operate on a vertically integrated model that encompasses the following:

- Plantation operations (nucleus and plasma models)

- Harvesting and primary processing (CPO mills)

- Secondary processing (refineries for RBD palm olein and stearin)

- Tertiary manufacturing (margarine, soap base, oleochemicals)

- Biodiesel plants compliant with B30 and B35 mandates

- Export facilities at port locations with bulk terminal access

This integration provides strategic advantages:

- Cost efficiencies across the supply chain

- Resilience during commodity price volatility

- Speed-to-market for processed derivatives

- Simplified compliance with international environmental and social governance (ESG) standards

3.4 Public vs Private Ownership

The largest palm oil firms operate under diversified holding groups. For instance:

- Wilmar International is publicly listed on the Singapore Exchange (SGX)

- Astra Agro Lestari is listed on IDX (Indonesia Stock Exchange) and is a subsidiary of Astra International

- SMART Tbk is part of the Sinar Mas Group and is also publicly listed on IDX

- Musim Mas remains privately held but is globally active

- Asian Agri is part of the RGE (Royal Golden Eagle) Group, a privately owned conglomerate

SOEs such as PT Perkebunan Nusantara (PTPN Group) manage several hundred thousand hectares, although they often lag behind private firms in terms of efficiency and downstream integration.

3.5 Smallholders’ Role in National Output

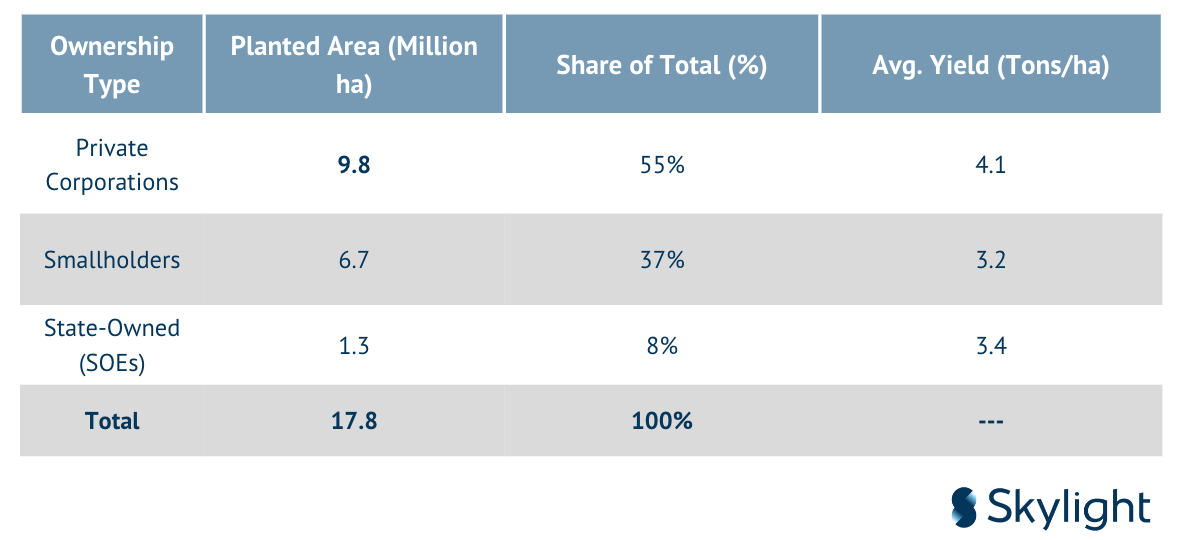

Roughly 6.7 million hectares of oil palm plantations are under smallholder control. They are divided into:

- Independent smallholders: Operate outside corporate supply chains; often lack access tocertified inputs

- Plasma smallholders: Tied to corporate nucleus estates; receive technical assistance and guaranteed off-take

Table 3.2: National Plantation Area by Ownership Type (2024)

Programs such as PSR (Peremajaan Sawit Rakyat) aim to replant 2.5 million hectares of aging smallholder plantations by 2026 using higher-yielding, certified seeds. However, land tenure challenges, financing gaps, and bureaucratic delays have slowed progress.

3.6 Refinery and Processing Capacity

Indonesia operates over 120 registered palm oil refineries, supported by biodiesel plants and oleochemical facilities. These assets are heavily concentrated in Sumatra and Kalimantan, close to major plantations and export ports.

Table 3.3: Major Refinery Zones and Capacities (2024)

Indonesia’s biodiesel production capacity reached 12.5 million kiloliters in 2024, with major contributions from Wilmar, Musim Mas, and Sinar Mas Bio Energi.

3.7 FDI and Strategic Expansion

Between 2020 and 2025, total FDI inflows into the palm oil value chain amounted to approximately USD 7.5 billion, with investment focused on:

- Refinery expansions (e.g., new RBD plants in East Kalimantan)

- Biodiesel infrastructure upgrades

- Digital traceability platforms using blockchain and satellite tech

- Sustainable replanting initiatives

Notable investors include:

- Temasek Holdings (Singapore)

- Louis Dreyfus Company (Netherlands)

- Chinese SOEs focused on energy security and edible oils

3.8 Corporate ESG and Innovation Trends

Key innovation and compliance trends among major players include:

- Adoption of remote sensing and AI for yield forecasting

- Rollout of digital plantation management systems

- Expansion of zero-burning commitments and no-deforestation sourcing policies

- Participation in RSPO Jurisdictional Approaches (e.g., in Central Kalimantan)

- Development of bio-based products, including palm oil-based ethanol and bioplastics

With increasingly stringent global requirements—especially from the EU (EUDR) and buyers like Nestlé, Unilever, and P&G—Indonesian producers are being compelled to modernize operational transparency, reduce emissions intensity, and strengthen supply chain traceability.

3.9 Supply Chain and Traceability Systems

As the global market becomes increasingly concerned with sustainability and deforestation-free commodities, Indonesian palm oil producers have embraced traceability technologies to improve transparency, especially among exporters. Traceability is now essential for meeting the standards of:

- The European Union Deforestation Regulation (EUDR)

- RSPO (voluntary but widely adopted)

- Buyers’ private ESG sourcing policies

Traceability Framework Components:

- First-mile traceability: Mapping Fresh Fruit Bunch (FFB) origin using GPS- tagged smallholder and estate data.

- Mill traceability: Digital logging of suppliers entering CPO mills using weighbridge-integrated apps.

- Processing facilities: Batch tracking using ERP systems at refineries and biodiesel

- Export terminal tracking: Blockchain-based systems to log dispatches from bulk storage to vessels.

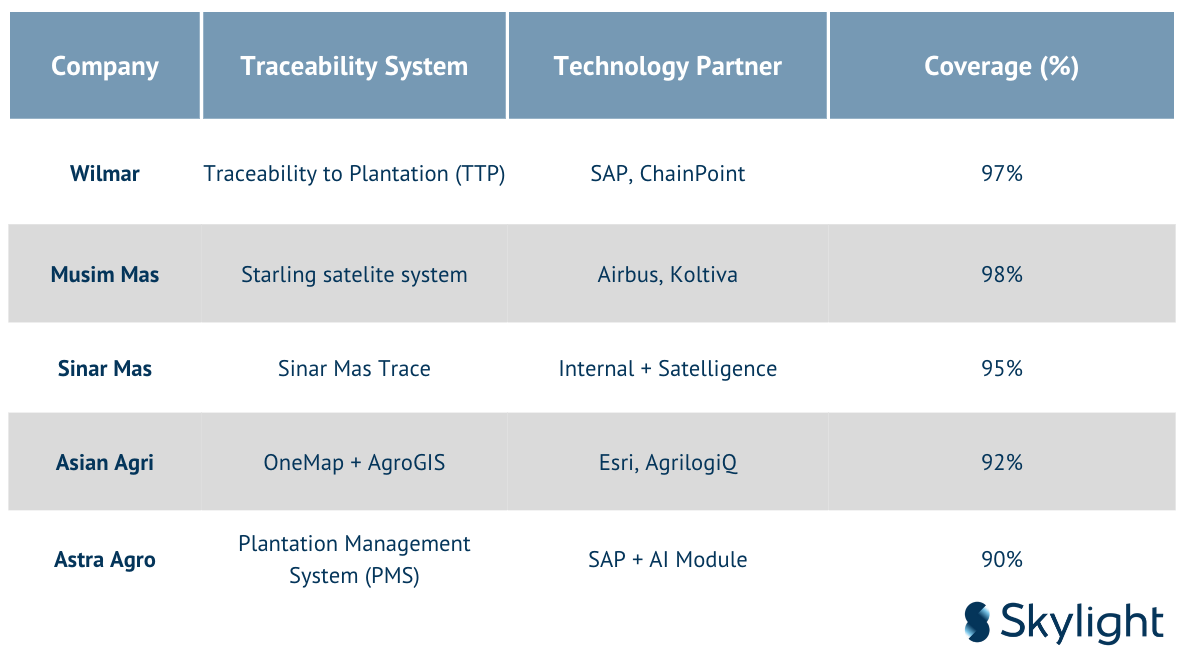

Table 3.4: Leading Traceability Solutions Adopted by Companies

3.10 Plasma Integration and Inclusive Business Models

Large producers have adopted “nucleus-plasma” partnership models, whereby smallholder groups are linked to a core estate (nucleus). Under this scheme:

- The company provides certified seedlings, fertilizer, and training

- Harvested FFB are sold back to the company at an agreed price

- Revenue is shared, and land titles may be co-managed or transferred

This inclusive business model has improved:

- Yield levels, where plasma yields rise to 8–4.1 tons/ha

- Access to finance, as producers provide bank guarantees

- Certification eligibility, improving access to RSPO/ISPO compliance

Despite progress, only around 52% of Indonesia’s smallholders are formally integrated into certified supply chains. The government’s target is to reach 70% by 2027 through PSR and new jurisdictional RSPO pilots in Central Kalimantan and Riau.

3.11Research, Development, and Innovation (RDI)

Top players have allocated increasing R&D budgets to productivity and sustainability improvements:

- Wilmar and Musim Mas have jointly developed high-oleic palm oil varieties for premium industrial use

- SMART and Bogor Agricultural University (IPB) are collaborating on climate- resilient hybrid seedlings

- Astra Agro has pioneered drone-based spraying and monitoring

- Asian Agri supports farmer field schools on low-emission fertilization

RDI efforts are also increasingly focused on:

- GHG mitigation in palm oil milling

- Alternative co-products: e.g., palm kernel shell briquettes, palm wax, and palm- based ethanol

- Digital tools for yield forecasting and land-use classification using AI/remote sensing

3.12Competitive Positioning in the ASEAN Region

Indonesia’s integrated corporate ecosystem gives it a competitive edge over peers, notably:

- Malaysia: Higher yield/ha and more RSPO-certified area, but limited land for expansion

- Thailand: Focus on smallholders and domestic consumption, lower industrial capacity

- Philippines & Vietnam: Minor producers, reliant on imports

Indonesia’s edge lies in:

- Economies of scale in both plantation and refinery output

- Logistics infrastructure via port-aligned clusters

- Growing internal market through biodiesel and food consumption

However, to maintain this lead, Indonesian firms must continually invest in:

- Supply chain traceability and deforestation-free certification

- Higher productivity for aging plantations

- Efficient use of land, labor, and water resources

Total Production, Export, Import and Potential Issues

Indonesia’s palm oil production has remained the highest globally over the last five years, consistently contributing over 57% of total global output. Despite temporary disruptions from La Niña weather patterns and pandemic-related labor shortages in 2020–2021, total production rebounded strongly in subsequent years, supported by replanting efforts, improved yields, and strong domestic demand.

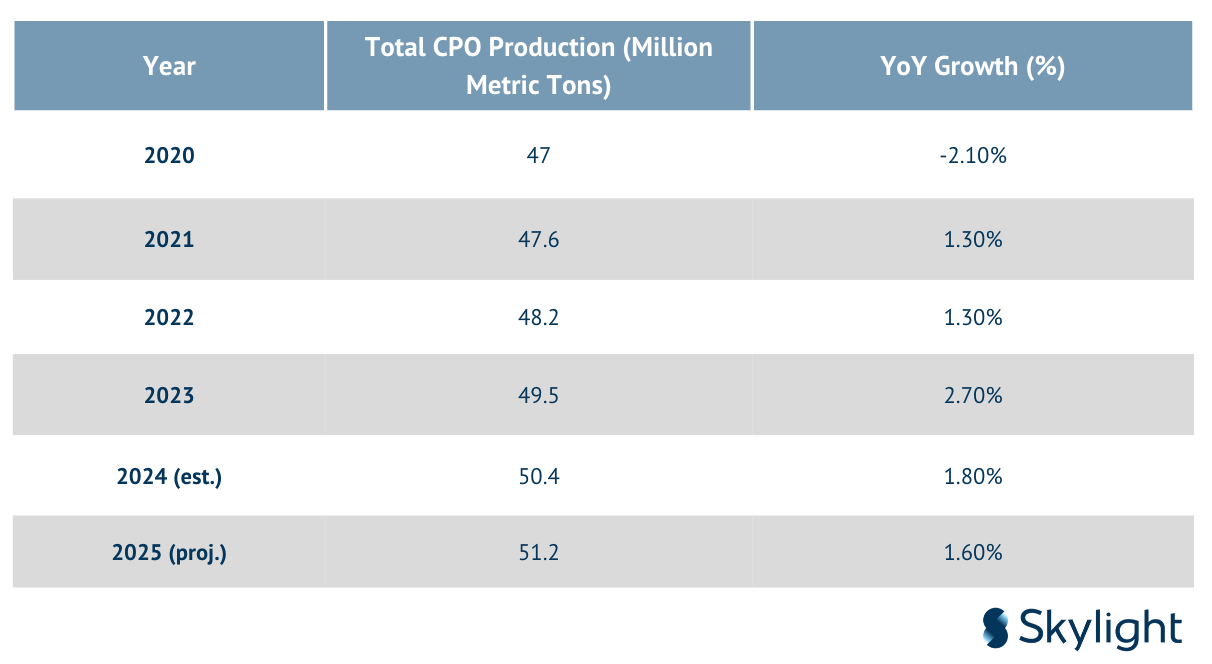

Table 4.1: Total CPO Production in Indonesia (2020–2025)

4.2 Export Trends

Indonesia’s palm oil exports are diversified across more than 150 countries, with Asia and the Middle East being the largest buyers. While the EU remains an important customer, its relative share has declined due to stricter sustainability requirements.

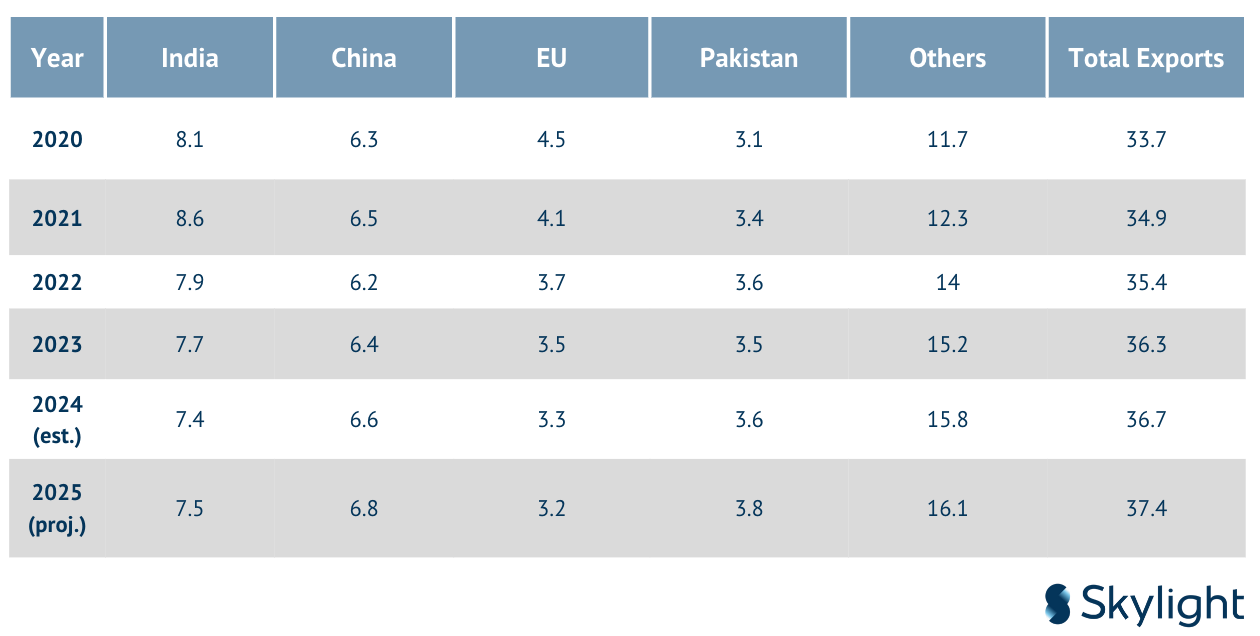

Table 4.2: Palm Oil Export Volume by Destination (Million Metric Tons)

4.3 Export Revenue Performance

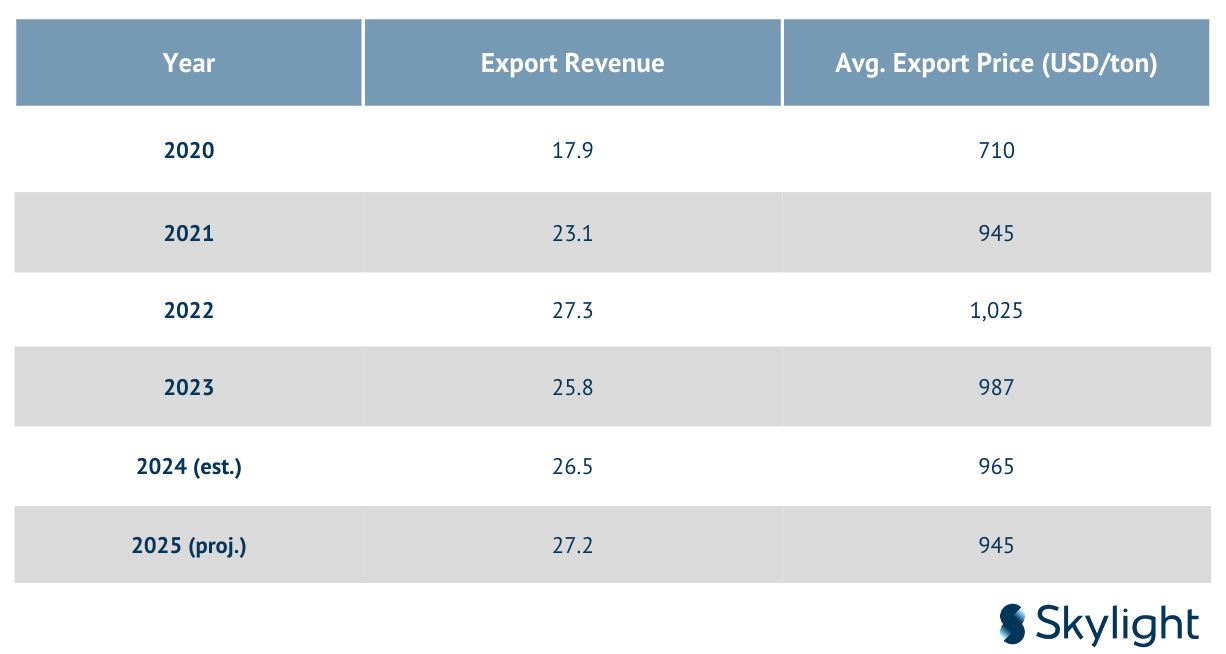

Export values are affected by both volume and international price trends. The sharp rise in CPO prices during 2021–2022 significantly boosted export revenue.

Table 4.3: Indonesia’s Palm Oil Export Revenue (USD Billion)

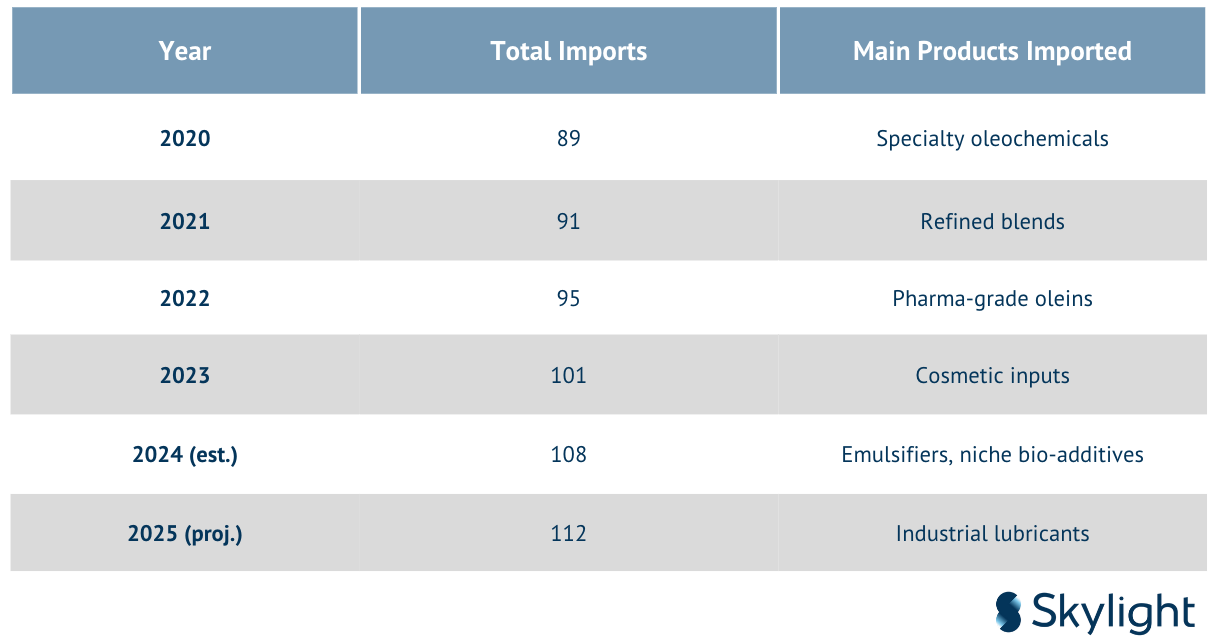

4.4 Import Overview

Indonesia is largely self-sufficient in palm oil and imports only a small volume of specialty processed palm derivatives not produced domestically.

Table 4.4: Palm Oil Import Volume (Thousand Tons)

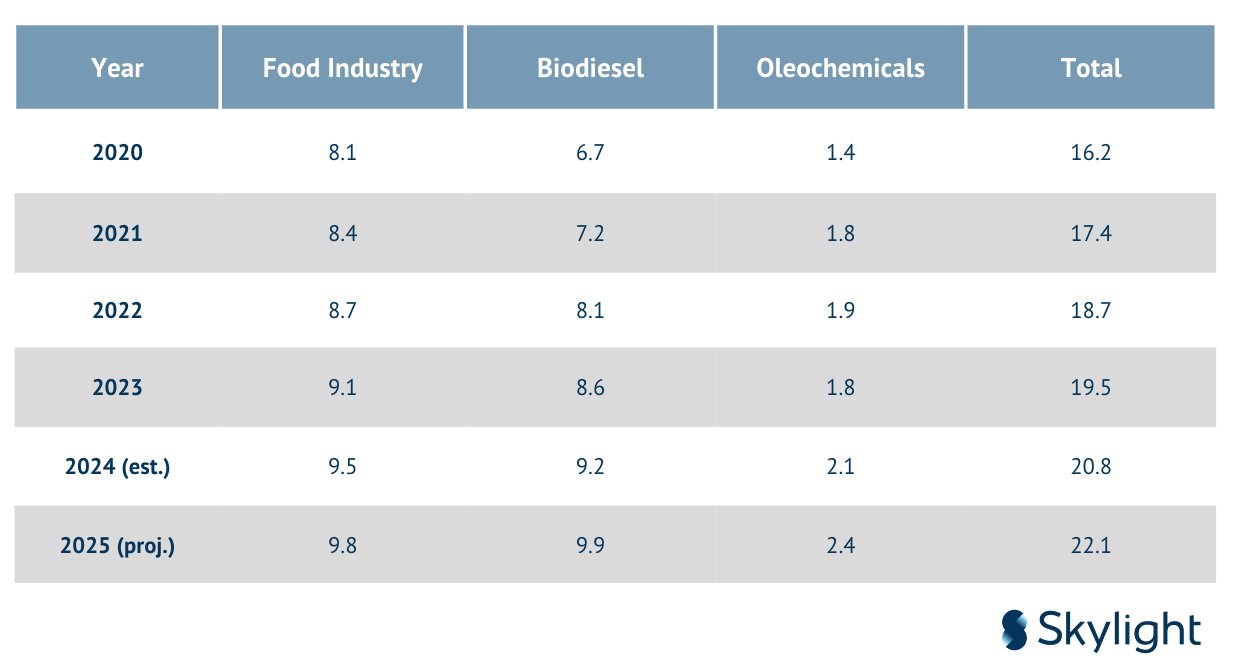

4.5 Domestic Consumption

Domestic consumption has surged due to national biodiesel blending mandates and increased industrial and retail food usage. The adoption of the B35 mandate has significantly increased demand for biodiesel feedstock.

Table 4.5: Domestic Palm Oil Consumption (Million Tons)

4.6 Trade and Policy Shocks

The 2022 temporary export ban on palm oil caused significant global price spikes and disrupted supply chains. Though lifted quickly, it prompted new discussions about:

- Domestic Market Obligation (DMO) compliance

- Export levy reforms

- Strategic buffer stocks

The EU’s upcoming EUDR enforcement (late 2024–2025) is expected to reduce direct exports to Europe unless supply chains fully comply with traceability requirements.

4.7 Potential Issues and Structural Challenges

Despite strong performance, several structural vulnerabilities and policy risks continue to affect Indonesia’s palm oil trade:

1. Over-Reliance on Key Markets:

India and China account for over one-third of total exports. Any tariff changes or bilateral disputes could severely impact volumes.

2. Traceability and EUDR Compliance Gaps:

As of mid-2025, only ~60% of export-bound palm oil is fully traceable to plantation. Many smallholders remain excluded from digital traceability networks, posing a risk to bulk exports to Europe and other ESG-sensitive markets.

3. Logistical Bottlenecks:

Port congestion and limited cold-chain storage in secondary regions (e.g., Sulawesi) reduce export efficiency. Rail and inland transport infrastructure still lags behind in Kalimantan.

4. Weather Volatility and Yield Pressure:

El Niño and La Niña cycles increasingly affect flowering and harvesting windows. A large portion of Indonesia’s plantation base is aging, with 40% of trees over 20 years old.

5. Policy Uncertainty:

Sudden export bans and levy changes erode investor confidence. Inconsistent enforcement of DMO quotas creates disincentives for efficient market allocation.

6. Price Volatility and Global Substitutes:

Global substitution with soybean oil (particularly in China and EU) could shrink margins. Volatile CPO prices affect financial planning, especially for smallholders.

7. Geopolitical and ESG Risks:

Increasing legal challenges from global environmental groups. ESG-related boycotts by multinational buyers could dampen brand image.

Benchmark / Common & Best Practices

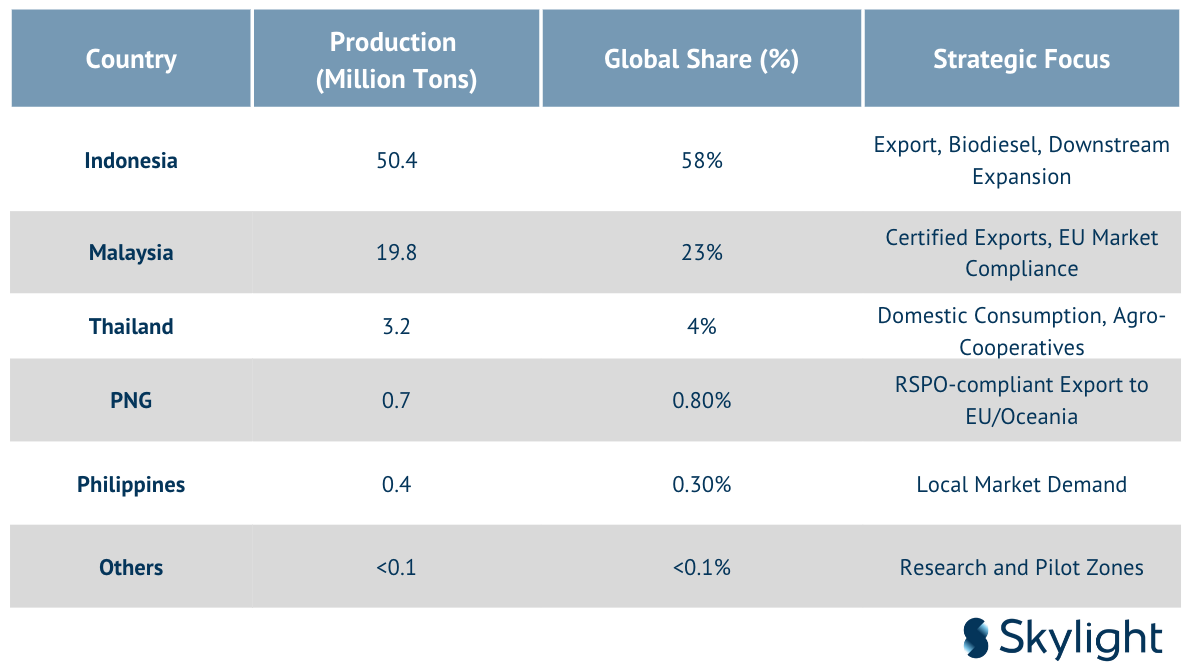

5.1 Regional Overview

Within ASEAN, Indonesia and Malaysia are the two global leaders in palm oil production. Combined, they account for over 85% of global output, shaping both international pricing and regulatory narratives. Thailand, the Philippines, Papua New Guinea (PNG), and others contribute minor volumes, mostly for domestic use or niche export markets.

Table 5.1: Palm Oil Production in ASEAN (2024)

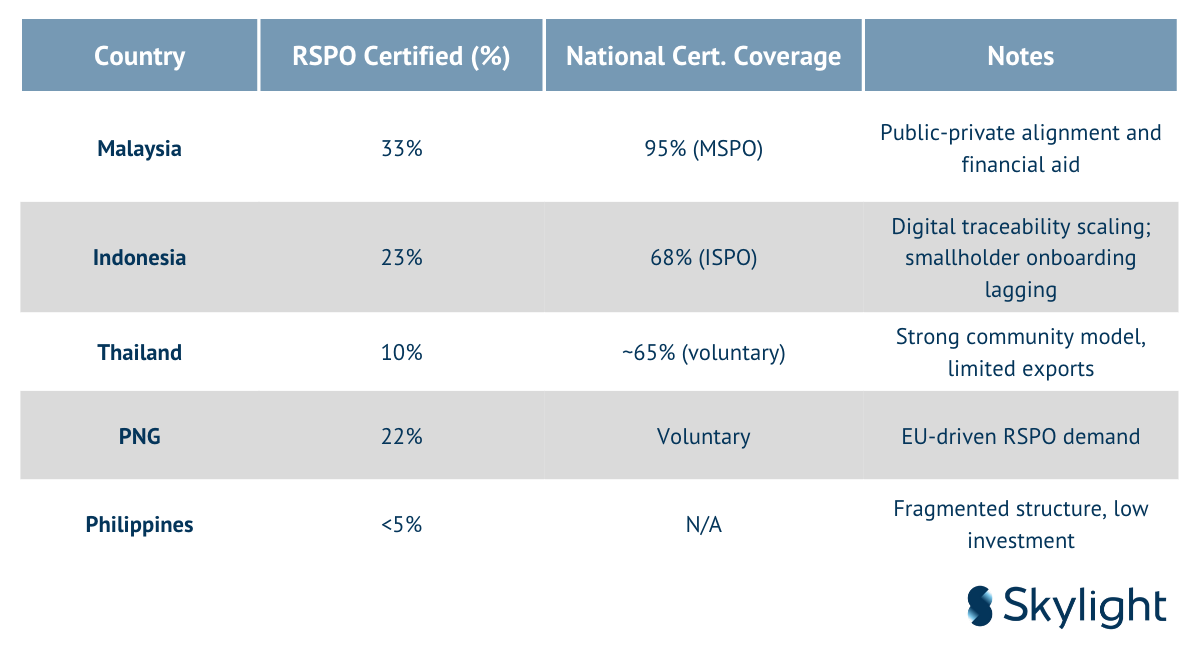

5.2 Certification, Sustainability, and ESG

Malaysia leads the region in sustainability standardization:

- MSPO: Mandatory for all producers since 2020, with 95% of national volume certified

- Strong integration with RSPO and satellite monitoring (notably with government support)

Indonesia’s ISPO certification, mandatory since 2020 for corporations and by 2025 for smallholders, has seen rapid expansion:

- 68% of volume ISPO-certified by mid-2025

- RSPO adoption lower due to cost and documentation burden for smallholders

Thailand and PNG emphasize localized and cooperative models. PNG, though small, performs well in RSPO due to buyer pressures from Europe and Australia.

Table 5.2: Certification Penetration in ASEAN (2025)

5.3 Smallholder Structure and Inclusion

Malaysia uses centralized agencies (FELDA, RISDA) to group and support smallholders. Services include subsidized replanting, shared equipment, and technical training. Thailand’s success hinges on farmer cooperatives that process and market FFB collectively.

Indonesia’s progress:

- Plasma-nucleus schemes under major companies (e.g., Asian Agri)

- Government’s PSR replanting initiative (~400,000 ha re-planted by mid-2025)

- App-based traceability pilots (e.g., SIPKEBUN, OneMap integration)

Challenges remain in land legality, fragmented supply chains, and limited access to financing tools for certification, inputs, and training.

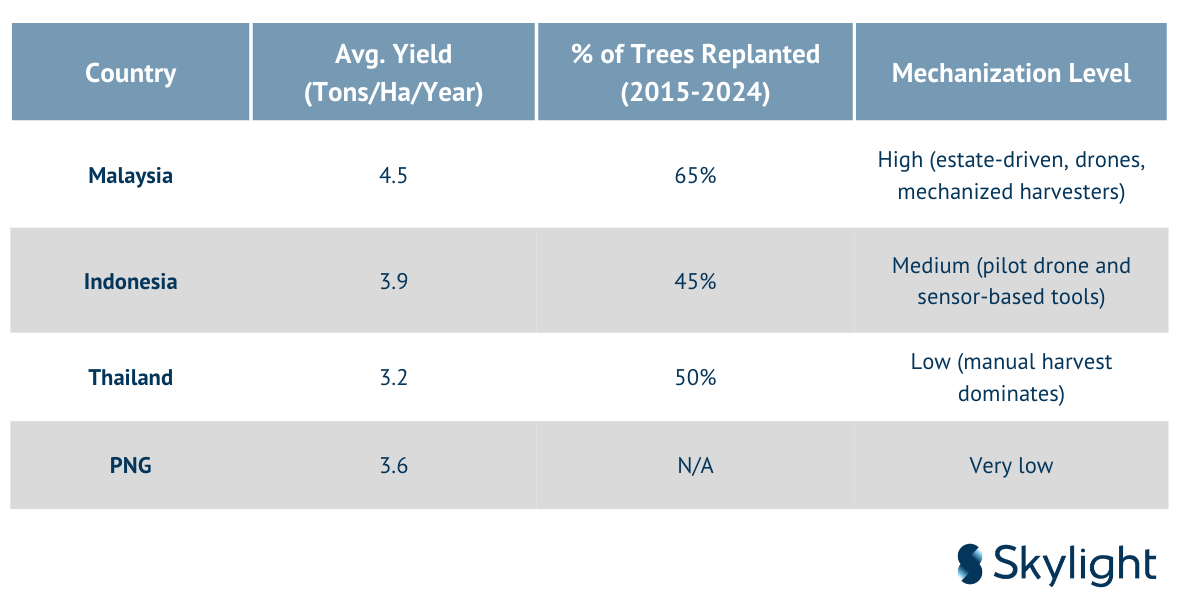

5.4 Yield and Productivity Benchmarking

Indonesia still underperforms in productivity compared to Malaysia, largely due to older trees and lower-quality inputs among independent smallholders.

Table 5.3: Yield and Replanting Efforts (2024)

5.5 Biodiesel Mandate Comparison

Indonesia has unmatched biodiesel policy ambition:

- B30 nationwide by 2020, B35 by 2023, aiming for B40 trials in 2026

- Subsidized through export levy via BPDP-KS fund

- Government-set Domestic Market Obligation (DMO) prioritizes domestic biodiesel consumption over exports

Malaysia and Thailand:

- Malaysia: B20 in select urban areas; lacks robust DMO

- Thailand: Flexible B7–B10 blending depending on sectoral supply

Indonesia’s model has successfully absorbed CPO surplus and stabilized domestic prices, although concerns over fiscal burden and environmental trade-offs persist.

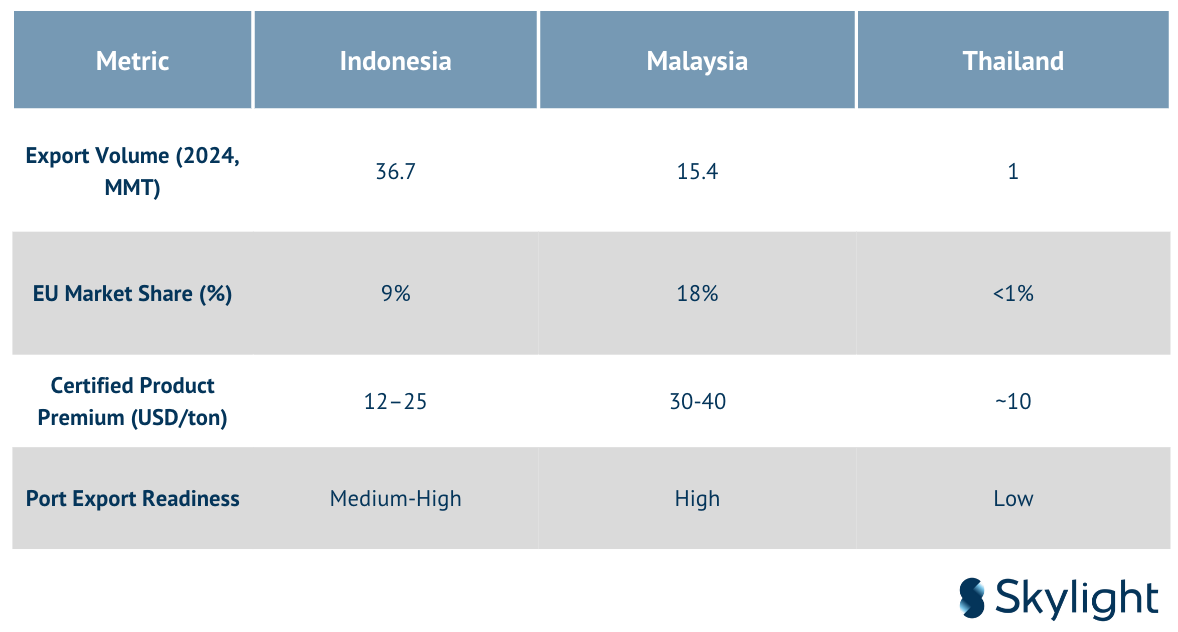

5.6 Export Strategy and Logistics Infrastructure

Malaysia maintains superior port efficiency and direct links to premium EU/US markets. High RSPO coverage allows price premiums and preferential trade treatment.

Indonesia, by contrast:

- Excels in scale, processing, and diversification

- Dumai, Belawan, Balikpapan serve as major export hubs

- Has shifted more exports toward India, China, Bangladesh, Pakistan, and Africa to buffer EU risk

Table 5.4: Export Strategy and Logistics Assessment

5.7 Key Takeaways

Indonesia leads ASEAN in volume, vertical integration, and biodiesel policy but still lags in sustainability certification, yield efficiency, and export value realization per ton. Malaysia’s smaller but higher-certification model is better aligned with EU market expectations. Thailand offers strong grassroots cooperative lessons.

To enhance competitiveness, Indonesia should prioritize:

- Scaling RSPO certifications to improve market access and premiums

- Improving productivity via smallholder mechanization and high-yield seeds

- Logistics investment beyond Sumatra and Kalimantan

- Full traceability ahead of EUDR implementation

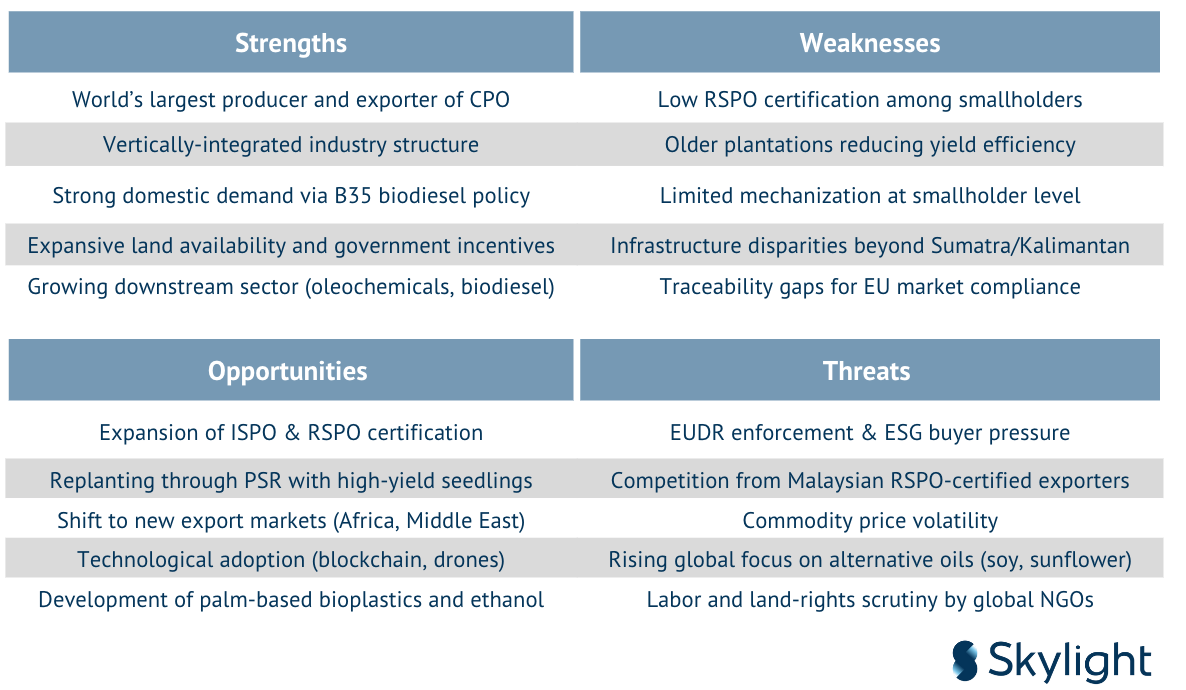

5.8 SWOT Analysis of Indonesia’s Palm Oil Industry Compared to ASEAN Peers

A strategic SWOT analysis helps summarize Indonesia’s relative positioning and its potential response to internal and external pressures across the ASEAN landscape.

Table 5.5: SWOT Analysis – Indonesian Palm Oil Industry (2025)

Key Insights from SWOT:

- Strengths confirm Indonesia’s global dominance and potential for long-term self- reliance through integrated policies and biofuel mandates.

- Weaknesses show urgent structural gaps in sustainability, smallholder capacity, and aging infrastructure, particularly in frontier zones.

- Opportunities lie in diversifying export markets, upgrading technology and certification, and positioning palm oil as a sustainable product with high-value

- Threats include regulatory headwinds, reputational risks, and stiffer competition from Malaysia and Latin American entrants.

Strategically, Indonesia must reinforce its strengths by scaling certified production, close traceability gaps, and mitigate external threats through diplomatic engagement and downstream diversification.

Government Policy, Challenge and Barrier

The Indonesian palm oil industry, while a dominant player globally, is navigating a complex landscape of operational, regulatory, environmental, and social challenges that must be addressed to ensure its long-term viability. This chapter explores these challenges in detail and provides a critical analysis of the interrelated risks that threaten the industry’s growth, credibility, and market access.

6.1 Environmental and Sustainability Pressures

Palm oil expansion has long been associated with tropical deforestation, biodiversity loss, and greenhouse gas (GHG) emissions. International scrutiny, particularly from the European Union (EU) and environmental NGOs, continues to shape the perception of Indonesia’s palm oil footprint.

- Deforestation Allegations: Satellite data and field reports indicate that illegal land clearing still occurs, especially in frontier regions such as Papua and West Kalimantan. Although Indonesia enacted a moratorium on new plantation permits (Presidential Instruction No. 8/2018), enforcement remains inconsistent.

- Peatland Conversion: Legacy plantations in high-carbon peatlands contribute significantly to Indonesia’s GHG These areas are also highly flammable, increasing the risk of transboundary haze.

- Biodiversity Impacts: Conversion of forested lands into plantations has led to habitat fragmentation for endangered species like orangutans and tigers.

6.2 Traceability, ESG Compliance, and Market Access

The EU’s Deforestation Regulation (EUDR), effective from 2024, mandates full traceability of palm oil imports. This places direct pressure on Indonesia’s fragmented supply chains:

- Plot-Level Traceability: Smallholders represent over 40% of production but often lack geolocation tools, proper records, or legal land titles.

- Certification Challenges: RSPO and ISPO certification coverage remains low among independent Certification costs, complexity, and lack of support hinder adoption.

- Export Risk: As markets move toward deforestation-free commitments, non- compliant producers face exclusion, lost revenue, and declining buyer trust.

6.3 Labor and Social Governance

Labor rights remain a contentious issue, particularly in non-corporate plantations:

- Child and Forced Labor: Despite labor laws (Law No. 13/2003), there are persistent reports of underage workers, excessive working hours, and contract

- Gender Disparity: Women are disproportionately represented in lower-paid, informal roles with limited protection.

- Land Tenure Conflicts: Disputes between plantation firms and indigenous or local communities stem from overlapping claims and historical land acquisition without free, prior, and informed consent (FPIC).

6.4 Economic Volatility and Cost Pressures

The industry is exposed to both global price cycles and domestic financial burdens:

- CPO Price Fluctuations: Prices are highly sensitive to geopolitical dynamics, export policies, and competing oil markets (soy, rapeseed, sunflower).

- Input Inflation: From 2021–2024, fertilizer, fuel, and logistics costs increased by 20–40% due to global supply disruptions.

- Dependence on Subsidies: The biodiesel mandate (B30/B35) is subsidized through BPDP-KS, which is itself funded by export levies. Any dip in export revenue strains subsidy sustainability.

6.5 Infrastructure and Productivity Gaps

- Aging Trees and Declining Yields: Over 40% of Indonesia’s palm trees are over 20 years old. Without replanting, yield per hectare drops significantly.

- Slow Replanting Uptake: Despite the PSR program, only ~400,000 hectares have been replanted by mid-2025 out of the targeted 2.5 million hectares.

- Regional Disparity: While Sumatra and parts of Kalimantan are well-developed logistically, Papua and Sulawesi suffer from poor road and port access, limiting efficient transport of fresh fruit bunches (FFB).

6.6 Fragmented Policy Implementation and Bureaucracy

Multiple institutions govern palm oil—often with overlapping mandates—which complicates policy execution:

- Conflicting Land Use Classification: The One Map Policy aims to harmonize land designations, but inconsistencies persist between forestry and plantation zones.

- Export Policy Volatility: Sudden bans (e.g., in 2022) and fluctuating levies have undermined investor confidence.

- Slow Disbursement of Incentives: PSR and other state-funded initiatives face bureaucratic delays, undermining smallholder trust.

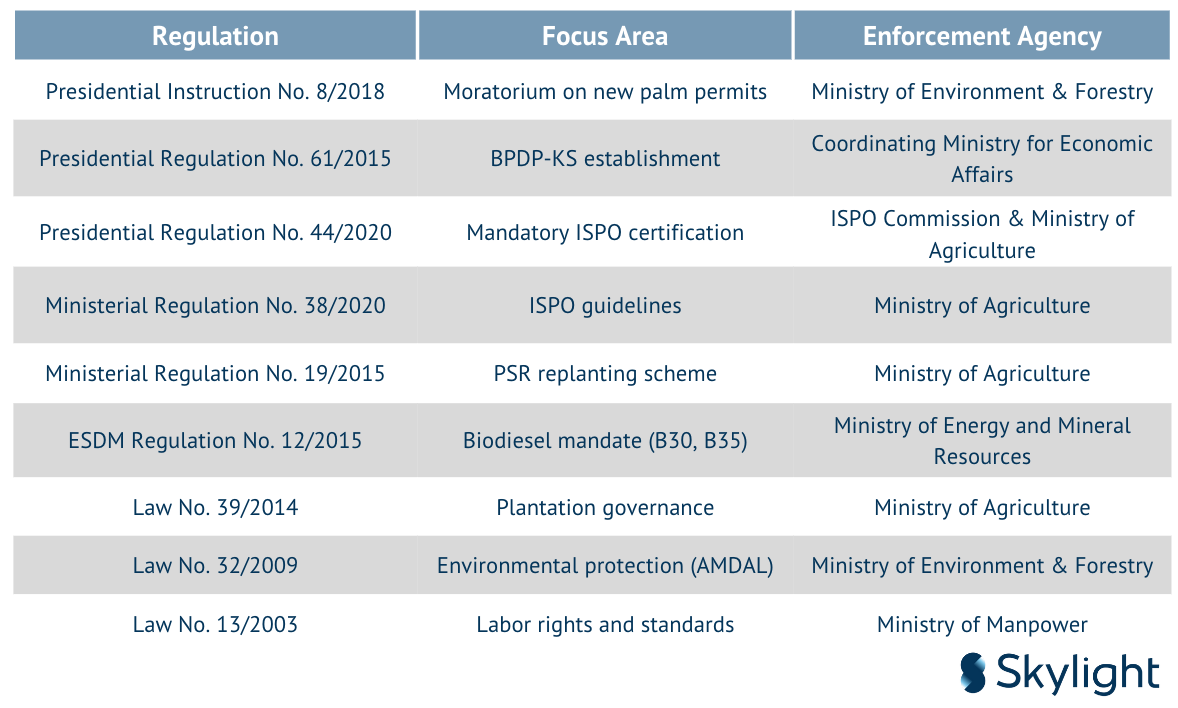

6.7 Key Laws and Regulations

A range of laws and regulations have been implemented to address these issues:

Outlook

As we move into the latter half of the 2020–2025 period, Indonesia’s palm oil industry is standing at an inflection point. Having established itself as the undisputed global leader in production and export volume, the question is no longer whether Indonesia can dominate the global market—but whether it can redefine it. The sector is increasingly judged not only by its economic output, but by its environmental footprint, social inclusion, and adaptability to a complex, rapidly evolving regulatory and geopolitical landscape.

- Sustainability Must Transition from Compliance to Embedded Culture: The mandatory implementation of ISPO (Indonesian Sustainable Palm Oil) certification and rising RSPO uptake are significant milestones. Yet these frameworks alone cannot guarantee global legitimacy unless sustainability becomes internalized within business models.

- Current Gap: Many producers pursue certification solely for market access, not due to belief in its Audits are often treated as episodic rather than as part of continual improvement.

- Future Path: Sustainability must be embedded into operational DNA—from estate planning and labor practices to waste management and emissions This includes annual self-assessment, transparent grievance handling systems, and adaptive ESG reporting.

- Example: Large groups like Golden Agri-Resources have begun integrating satellite-based deforestation tracking and grievance portals, setting new

7.2 Reimagining Smallholder Inclusion as an Economic Strategy

Roughly 41% of Indonesia’s oil palm area is controlled by smallholders. Yet these stakeholders remain underproductive, undercapitalized, and often excluded from certification programs.

- Structural Barriers: Legal land tenure, replanting finance, access to high-yield seedlings, and traceability compliance remain elusive.

- Strategic Imperative: Inclusion is not merely a social responsibility—it is a supply chain security Buyers and regulators are increasingly asking for traceable and deforestation-free sources.

· Solution Framework:

- Land legality reform integrated with the One Map Policy

- Digital extension services via mobile platforms

- Blended finance models involving public-private-NGO collaboration for PSR (Peremajaan Sawit Rakyat)

- Formation of certified smallholder cooperatives with pooled certification costs

7.3 Digital Transformation as a Non-Negotiable Catalyst

The Fourth Industrial Revolution offers transformative potential for palm oil:

- Traceability: From blockchain to satellite imaging, technology can enable full plot-to-port visibility

- Productivity: AI-based yield prediction, drone fertilization, and IoT sensors can help optimize input use

- Compliance and ESG: Real-time dashboards can track fire incidents, labor compliance, and environmental risks

Yet adoption is uneven. Large estates pilot innovations while smallholder’s lag. The government must catalyze a national digital roadmap for the industry

7.4 ESG is Not a Constraint—It’s a Competitive Advantage

In global markets, environmental, social, and governance (ESG) performance is no longer a reputational metric—it’s a license to operate. Investors are recalibrating portfolios, and buyers are aligning supply chains with ESG filters.

- Case Study: Nestlé and Unilever now require verified deforestation-free sourcing and full traceability. Non-compliance leads to supplier exclusion.

- Financial Implication: Banks and insurers are beginning to tie lending rates and risk assessments to ESG scores. Poor performers face higher costs of capital.

Indonesia has an opportunity to redefine palm oil as a responsible, climate-smart commodity—if it aligns incentives, enforces compliance, and promotes its success stories globally.

7.5 Institutional Reform Must Be Cohesive and Courageous

The policy landscape is fragmented. ISPO is managed by the Ministry of Agriculture, but land legality rests with ATR/BPN, while replanting is coordinated through multiple overlapping schemes.

- Current Bottlenecks: Slow disbursement of PSR funds, conflicting land designations, inconsistent enforcement

- Strategic Proposal: Create a Presidential Task Force for Palm Oil Sustainability with legal authority to synchronize ministries, accelerate reform, and oversee One Map implementation.

7.6 Indonesia Can Lead the Global Palm Oil Narrative—If It Chooses To

The international discourse around palm oil has been largely negative, driven by deforestation data and advocacy campaigns. Indonesia must take control of the narrative:

- Transparency: Public access to certification data, complaint outcomes, and fire alerts

- Innovation Showcases: Promote success stories of sustainable palm oil villages, digital cooperatives, and climate-smart practices

- Global Advocacy: Engage multilaterals, standards bodies, and buyer countries with verified data, rather than defensive rhetoric

The next five years will define the next 50. Indonesia must decide whether it will remain a volume-based, resource-extractive industry—or evolve into a model of regenerative, inclusive, and technology-driven agriculture.

With bold vision, strategic execution, and coordinated governance, Indonesia can not only protect its economic interests—but elevate its global leadership in sustainable commodities.

Sources

- Skylight Analytics Hub

- Badan Pusat Statistik (BPS) Indonesia – https://bps.go.id

- Gabungan Pengusaha Kelapa Sawit Indonesia (GAPKI) Annual Reports

- United States Department of Agriculture (USDA) – FAOSTAT & Oilseeds Reports – https://fas.usda.gov/

- BPDP-KS (Badan Pengelola Dana Perkebunan Kelapa Sawit) – https://bpdp.or.id

- International Monetary Fund (IMF) – World Economic Outlook – https://imf.org/en/Publications/WEO

- Center for International Forestry Research (CIFOR) – Palm Oil and Land Use Publications – https://cifor.org/publications/

- World Resources Institute (WRI) – Indonesia Forestry & Land Governance – https://wri.org/indonesia

- Sawit Watch Indonesia – https://sawitwatch.or.id

- Roundtable on Sustainable Palm Oil (RSPO) – Impact Reports & Certification Data – https://rspo.org/resources

- Serikat Petani Kelapa Sawit (SPKS) – Smallholder Research – https://spks.or.id

- Mongabay Indonesia – Environment & Agriculture – https://mongabay.co.id

- Eco-Business – Sustainable Agrifood Reporting – https://www.eco- com

- European Commission – EU Deforestation Regulation (EUDR) – https://environment.ec.europa.eu/deforestation-free-products_en

- Food and Agriculture Organization (FAO) – Food Outlook Reports – https://fao.org/giews/reports/food-outlook/en/

- OECD-FAO Agricultural Outlook 2023–2032 – https://fao.org/publications/oecd-fao-agricultural-outlook-2023- 2032/en/

- ASEAN Secretariat – Agriculture Statistics & Reports – https://asean.org/our-communities/agrifood/

- World Agroforestry (ICRAF) – Palm Oil & Land Use – https://worldagroforestry.org

- International Finance Corporation (IFC) – Sustainable Finance & Palm Oil – https://ifc.org

- UN Environment Programme – Emissions from Agriculture – https://unep.org

- Global Canopy – Risk in Supply Chains – https://globalcanopy.org

Disclaimer

The content on this platform (“Platform”) is proprietary to Skylight, protected under copyright and intellectual property laws, and cannot be reproduced or used without written authorization. The insights shared are for informational purposes only, do not constitute professional advice, and may not reflect the latest industry developments. Skylight and its contributors disclaim all liability for actions taken based on the content and do not guarantee specific outcomes from past insights or case studies. Use of the Platform does not establish any contractual or advisory relationship with Skylight. By accessing this Platform, you agree to these terms. © 2025 Skylight Strategic Indonesia. All rights reserved