By Fahmi Shahab, Industrial Park

From state dominance to private dynamism: can Indonesia’s industrial parks keep pace with global benchmarks?

Industrial parks have historically played a pivotal role in shaping national industrial strategies across the world. In Japan, more than 1,500 designated estates were established through state planning, forming the backbone of post-war manufacturing and clustering suppliers around metropolitan hubs such as Tokyo, Osaka, and Nagoya. Australia, by contrast, does not operate multiple dispersed industrial parks but developed a single large-scale, structured industrial zone—designed with an organized layout to centralize infrastructure, logistics, and land use. In other developed economies such as South Korea and parts of Europe, industrial parks have similarly been state-driven, reflecting governments’ central role in directing industrial growth and spatial planning. Meanwhile, China and Vietnam demonstrate how state-led industrial zones can accelerate integration into global supply chains, with China’s 2,543 national-level parks contributing nearly 30 percent of GDP, and Vietnam’s 400-plus parks reaching average occupancy rates of 80 percent.

Against this global backdrop, Indonesia’s trajectory stands out. While it began with a familiar state-driven model in the 1970s, the country diverged in the 1990s by opening the sector to private participation—ushering in new momentum and international investment. This generational journey was not accidental: it was driven by a combination of structural and policy forces. First, government fiscal limitations meant that the state could not single-handedly finance large-scale estate expansion. Second, rapid globalization and the relocation of manufacturing from Newly Industrialized Countries created a strong pull for private sector participation. Third, the growing complexity of infrastructure and tenant needs required more flexible, commercially oriented developers. And finally, rising expectations from investors and global buyers pushed Indonesia to strengthen its regulatory frameworks, spatial planning, and sustainability standards. Together, these dynamics explain why Indonesia’s industrial parks have evolved through distinct phases—moving from fragmented clusters to structured estates, and now toward smart, eco-industrial ecosystems.

Generation I (1970–1989): State-Led Beginnings

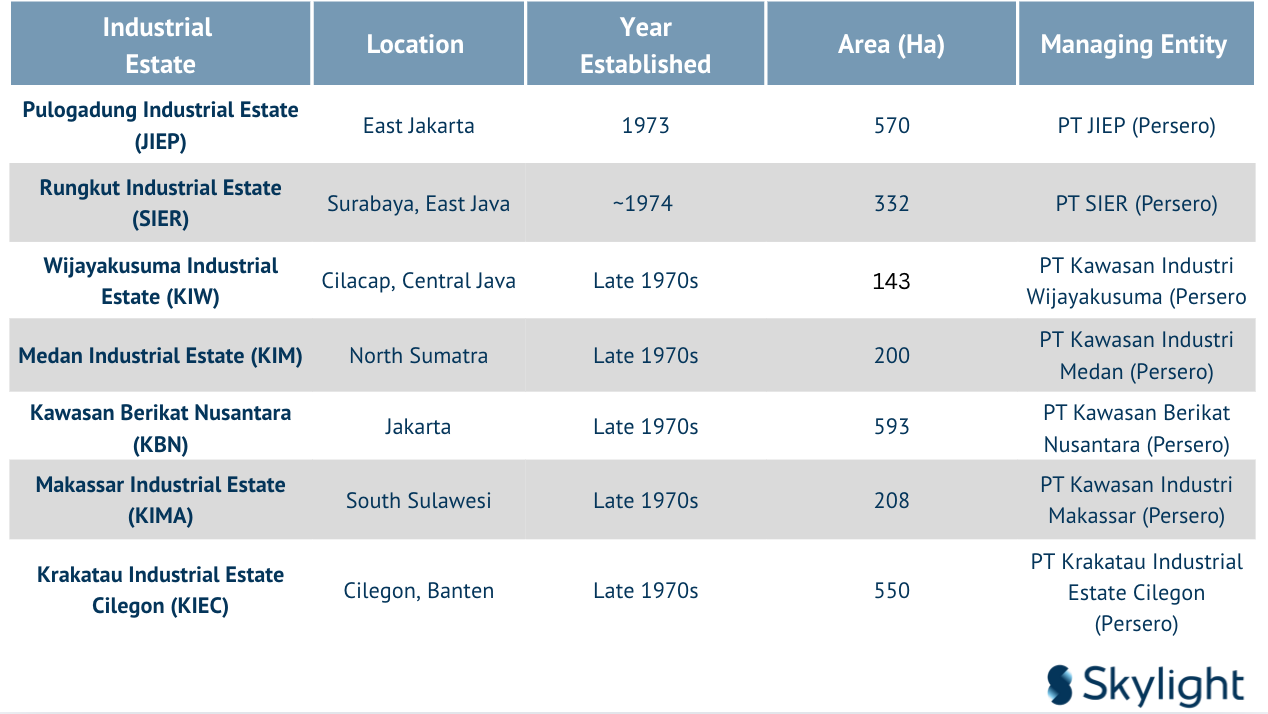

The concept of industrial parks in Indonesia first emerged in the early 1970s, with an initial feasibility study in Cilacap, then an emerging oil and gas hub. Although the plan stalled, momentum shifted to East Jakarta, where the Pulogadung Industrial Estate was established in 1973 through a joint venture between the Jakarta provincial government and the Ministry of Finance. Pulogadung quickly became a landmark project, serving as Indonesia’s first operational industrial park and a model for subsequent developments.

During this formative period, the legal framework—anchored in Ministerial Regulation No.5/1974—restricted the development of industrial estates exclusively to state-owned enterprises (BUMN/BUMD). As a result, expansion was limited but strategically significant. Building on Pulogadung’s success, the government replicated the model through regional partnerships: Rungkut Industrial Estate in Surabaya, managed by PT SIER; Medan Industrial Estate in North Sumatra; Makassar Industrial Estate in South Sulawesi; Wijayakusuma Industrial Estate in Cilacap; Krakatau Industrial Estate in Cilegon; and Kawasan Berikat Nusantara (KBN) in Jakarta.

In total, only seven estates were successfully established during this era, underscoring the state’s dominant role in shaping industrial geography. These projects, though modest in number, laid the institutional foundation for Indonesia’s industrialization. Importantly, they reflected the government’s ambition to replicate the Pulogadung model nationwide while also revealing the structural limitations of a state-only development framework.

However, this first generation faced a series of challenges and problems:

- Capital constraints: Reliance on state-owned enterprises meant expansion was limited by government fiscal capacity, slowing the pace of development.

- Infrastructure gaps: Supporting facilities such as ports, power supply, and reliable transport corridors were still underdeveloped, creating bottlenecks for tenants.

- Limited investor attraction: Foreign and domestic investors were cautious, as land preparation and estate facilities often lagged behind expectations.

- Rigid governance model: State ownership reduced operational flexibility and responsiveness to market needs, leading to inefficiencies in land pricing, service delivery, and estate management.

- Fragmented spatial planning: Without a comprehensive Rencana Umum Tata Ruang Wilayah (RUTRW), industrial activities still spilled outside designated estates, undermining the purpose of clustering.

- Environmental oversight: Early estates were primarily designed for industrial clustering, with minimal attention to sustainability, waste management, or community integration.

Despite these constraints, Generation I provided the critical institutional starting point for Indonesia’s industrial estate model. Yet, its limitations created strong pressure for reform—paving the way for the private sector participation of Generation II.

Exhibit 1 below summarizes these first-generation estates, highlighting their geographic spread, land area, and managing entities.

Exhibit 1. First-Generation Industrial Estates in Indonesia (1970s–1980s)

Generation II (1990s): Private Sector Dynamism

A turning point came in 1989, when Presidential Decree No.53/1989 opened the sector to private participation. This policy shift coincided with a wave of industrial relocation from the Newly Industrialized Countries (NICs)—including Singapore, Hong Kong, Taiwan, and South Korea—whose rising labor costs pushed manufacturers to seek more cost-efficient production bases abroad. By 1993, Indonesia emerged as a prime destination, attracting significant foreign direct investment in textiles, electronics, automotive components, and consumer goods.

The arrival of this relocation wave provided not only foreign capital but also the impetus for new types of partnerships. For the first time, domestic property developers, who had previously concentrated on residential and commercial real estate, entered the industrial estate business. Leveraging their expertise in land acquisition, master planning, and infrastructure development, these players transformed into industrial park developers—often forming joint ventures with foreign partners such as Marubeni, Hyundai, Itochu, Sumitomo, and Taisei.

The Jakarta–Cikampek toll road corridor became the epicenter of this transformation, with numerous private estates established to accommodate international manufacturers relocating from East Asia. This era also saw the rise of Indonesia’s property conglomerates in the industrial estate segment:

- PT Jababeka Tbk, which pioneered the integrated township-and-industry model with its flagship Cikarang estate.

- Lippo Group, which diversified into mixed-use developments combining residential, commercial, and industrial facilities.

- Sinar Mas Land, which gradually expanded into industrial park projects, aligning with its large-scale township strategy.

- Other domestic groups such as Agung Podomoro and Bekasi Fajar also entered the space, seeking to capture long-term demand from manufacturers.

By the mid-1990s, nearly 80 percent of new industrial park development was driven by private entities, a dramatic reversal from the state-dominated model of the previous generation. This era is therefore recognized as the second generation of Indonesian industrial parks—defined by private-sector dynamism, international joint ventures, and the integration of Indonesia into regional supply chains.

Yet, the success of Generation II was accompanied by challenges and problems that revealed structural weaknesses:

- Uncoordinated land use: rapid private development often outpaced spatial planning, leading to overlapping zones and urban sprawl.

- Infrastructure bottlenecks: while parks were established along the toll corridor, supporting logistics—ports, rail, and energy supply—did not always keep pace.

- Environmental concerns: with limited regulation, wastewater, emissions, and solid waste management were not systematically addressed, creating long-term sustainability risks.

- Speculative land practices: some developers acquired land far beyond immediate demand, raising land prices and reducing affordability for manufacturers.

- Uneven quality of estates: while some parks achieved world-class standards, others offered only basic infrastructure, creating inconsistency across the sector.

- Social impacts: rapid industrial expansion sometimes clashed with surrounding communities, particularly in land acquisition and limited local employment benefits.

These shortcomings underscored the need for stronger regulatory frameworks, standardized practices, and spatial integration, which would later emerge as the hallmarks of Generation III.

Generation III (2009–2015): Regulation and Structuring Growth

Uncontrolled industrial sprawl in the 1990s and early 2000s created mounting challenges for spatial planning, environmental sustainability, and infrastructure efficiency. To address these issues, the government enacted Government Regulation No.24/2009, which mandated that all new industrial operations must be located within designated industrial estates. This milestone was further reinforced by Law No.3/2014 on Industry and Government Regulation No.142/2015 (subsequently updated to PP No.20/2024), which elevated industrial estates to the status of strategic national infrastructure for manufacturing.

In this new regulatory landscape, industrial park developers began to assume a far more institutionalized and strategic role, ushering in the third generation of Indonesian industrial parks. One defining characteristic of this era was the emergence of multiple ownership and equity structures:

- 100% State-owned estates, continuing the legacy of earlier parks such as Pulogadung or SIER.

- 100% private-owned estates, developed by domestic conglomerates and foreign investors with full operational control.

- Hybrid joint ventures, where private capital partnered with state entities, combining the government’s regulatory influence and land resources with private efficiency and market-driven development.

This diversified ownership model broadened investment options and accelerated estate development across the archipelago.

At the same time, the government retained critical responsibilities outside the park gates. While private developers were tasked with creating world-class industrial estates, the state focused on building supporting infrastructure such as ports, highways, and energy systems, as well as ensuring human capital readiness. A key priority was aligning the education system with industry demand: creating stronger “link and match” mechanisms between graduates and industrial employers. This focus on skills development was vital to ensure that Indonesia’s growing workforce could effectively meet the rising sophistication of global manufacturing requirements.

Yet, Generation III also faced persistent challenges and structural problems:

- Implementation gaps: although the regulations were ambitious, enforcement varied widely across provinces, with some estates still operating below national standards.

- Coordination issues: central and regional governments often had overlapping mandates, leading to regulatory fragmentation and delays in permitting.

- Infrastructure lag: despite progress, connectivity to ports, rail, and power grids remained uneven, limiting the competitiveness of parks outside Java.

- Land acquisition difficulties: protracted negotiations, high costs, and community resistance slowed estate expansion.

- Workforce mismatch: although the government promoted link-and-match initiatives, many graduates lacked the technical and digital skills demanded by global manufacturers.

- Limited incentives for green transition: sustainability requirements were not yet strongly enforced, leaving environmental management as an afterthought in many estates.

In short, Generation III represented not only the formal structuring of industrial development through regulation, but also the beginning of a shared-responsibility model: private developers managing estates, the government enabling connectivity and workforce supply, and both sectors working together to ensure competitiveness in an increasingly globalized economy. However, the execution challenges of this period highlighted the urgent need for a more integrated, sustainable, and technology-driven model—setting the stage for Generation IV.

Generation IV (Today and Beyond): Smart Eco-Industrial Parks

Indonesia is now entering a fourth generation of industrial park development, shaped by globalization, sustainability, and digitalization. The next frontier is the creation of smart eco-industrial parks, designed to integrate:

- Digital systems such as IoT-enabled utilities, smart grids, and automated logistics for real-time efficiency.

- Green infrastructure including renewable energy integration, circular economy practices, and low-carbon operations.

- Collaborative governance through stronger alignment between central and local government, private developers, and surrounding communities.

Globally, several benchmarks illustrate how smart eco-industrial parks can transform economies. Kalundborg Symbiosis in Denmark is often cited as the world’s first successful eco-industrial park, where companies exchange energy, water, and by-products in a closed-loop system. Ulsan Mipo Eco-Industrial Park in South Korea, covering more than 6,000 hectares, has become a model for large-scale industrial symbiosis, achieving significant reductions in CO₂ emissions and resource use. Suzhou Industrial Park in China has evolved into a digitally enabled, green manufacturing hub, attracting more than 90 Fortune 500 companies while embedding sustainability standards. Even in Australia and Europe, emerging eco-industrial precincts integrate renewable energy microgrids, waste-to-resource systems, and advanced monitoring platforms.

By comparison, Indonesia’s industrial parks are not yet fully operating as smart eco-industrial parks. While some estates have begun introducing renewable energy, centralized wastewater treatment, and pilot-scale digital systems, a comprehensive transformation remains incomplete. Several challenges persist:

- Fragmented infrastructure: many parks are still struggling with reliable electricity, clean water, and logistics connectivity.

- High investment costs: smart and green technologies require significant upfront capital, which not all developers can shoulder.

- Limited regulatory incentives: although sustainability is encouraged, policy frameworks and fiscal incentives to accelerate eco-industrial upgrades remain underdeveloped.

- Human capital readiness: operating smart technologies requires advanced digital and technical skills, yet the talent pipeline is still catching up.

- Coordination gaps: public–private collaboration is uneven, with different regions moving at different speeds in adopting eco-industrial models.

As a result, Indonesia’s parks are in a transitional phase—moving beyond traditional estates toward smart eco-industrial ecosystems, but not yet achieving full integration at a national scale. The opportunity, however, is clear: with consistent policy support, targeted investment, and stronger human capital development, Indonesia could position itself alongside global leaders in smart and sustainable industrial park development.

Author’s Recommendations

The generational evolution of Indonesia’s industrial parks underscores the necessity for a recalibrated strategy that balances regulatory alignment, investor confidence, technological adoption, and differentiated development pathways. Several imperatives emerge:

- Strengthen institutional coherence: Greater coordination between central, provincial, and local authorities is required to align spatial planning and regulatory enforcement, thereby reducing overlaps and providing investors with predictable governance.

- Reinforce investor trust through sustainability and transparency: Industrial parks that internalize ESG principles, ensure transparent management, and provide reliable infrastructure will hold a distinct advantage in attracting global FDI. Fiscal instruments and incentives should be more systematically deployed to reward sustainable practices.

- Embrace digitalization as an inevitability: The next wave of competitiveness will be determined by the degree to which parks integrate digital technologies—IoT-enabled utilities, data-driven logistics, and predictive maintenance systems. For global investors, digital readiness will increasingly serve as a proxy for long-term resilience and operational excellence.

- Adopt differentiated models of industrial development: Not all estates need to pursue the eco-industrial paradigm. The strategic orientation of each park must be informed by its tenant profile and investment type. For instance, a data center–oriented estate should prioritize digital infrastructure, uninterrupted energy supply, and advanced cooling systems rather than resource-sharing or waste symbiosis. In contrast, estates dominated by heavy manufacturing or resource-intensive sectors will derive greater value from eco-industrial models and circular economy practices.

- Benchmark relentlessly against regional competitors: To secure its position in global supply chains, Indonesia must continually measure itself against regional peers such as Vietnam, Malaysia, Thailand, and India. Offering competitive land pricing, streamlined permitting, robust infrastructure, and a skilled workforce will be essential to remain on par with or ahead of the region.

Source

- Skylights Analytics Hub