By Sonia Adriaty, Industrial Park

From the New Order era through the early 21st century, Java has served as the industrial heart of Indonesia, accounting for over 70% of the national non-oil-and-gas manufacturing GDP. Key provinces such as West Java, East Java, and Central Java dominate industrial activity, supported by robust infrastructure, international ports, abundant labor, and strong vocational education systems. Leading industrial estates like JIEP (Jakarta), Jababeka (Cikarang), KIIC (Karawang), and SIER (Surabaya) have long attracted major investment.

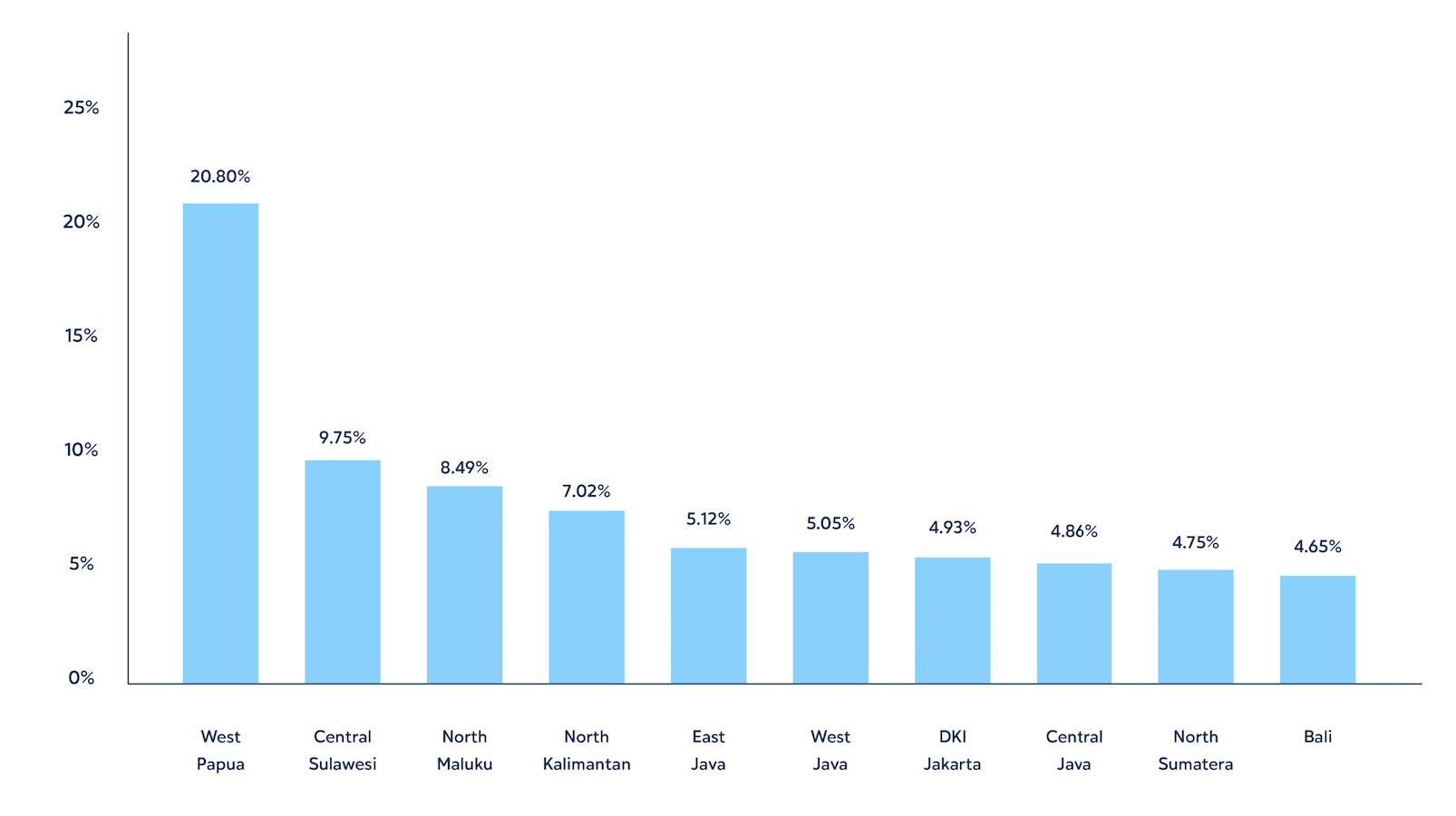

In recent years, however, industrial growth outside Java has accelerated, emerging as a critical pillar of Indonesia’s broader economic development. This shift is particularly evident in the eastern regions, where rising investment in mining and resource processing has driven major infrastructure expansion. The trend is underscored by strong 2024 regional GDP growth figures—West Papua posted the highest growth nationwide at 20.80%, followed by Central Sulawesi at 9.75%, both fueled by downstream industrial processing as the engine of transformation.

Figure 1: Indonesia’s Economic Growth shown by provinces in 2024

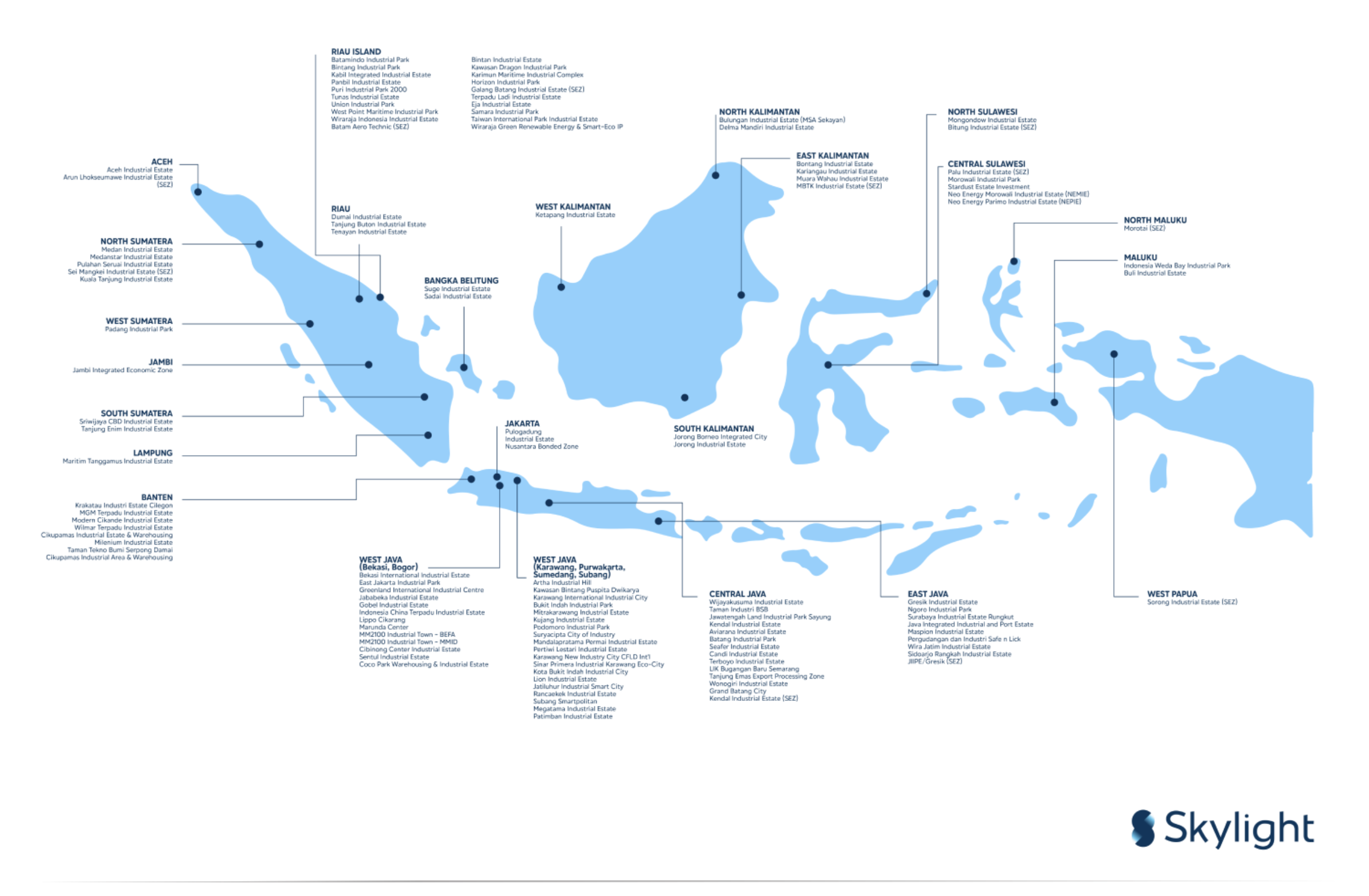

Based on data from the Association of Industrial Estates (Himpunan Kawasan Industri or HKI), of the 120 industrial parks that are HKI members, 56 are located outside Java. The province with the highest number is Riau Islands, home to 20 industrial parks spread across Batam, Bintan, and Karimun.

Figure 2: Industrial Park dispersion in Indonesia

The development of industrial zones outside Java has become a strategic agenda for the Indonesian government. Over the past decade, infrastructure projects beyond Java have aimed to address the disparity in industrial contributions across regions, particularly in Sumatra, Kalimantan, Sulawesi, and Papua, which continue to face structural challenges. This effort is strategic given that many provinces outside Java possess significant comparative advantages, such as abundant natural resources, export market potential, and geographical proximity to international shipping routes.

Michael E. Porter, a renowned economist and strategy expert from Harvard Business School, argues through the Diamond Model that a region’s industrial competitiveness is shaped by four key determinants:

- Factor Conditions: Availability of basic and advanced production factors such as cheap labor, raw materials, strategic location (basic), and skilled labor, technology, innovation, and modern infrastructure (advanced).

- Demand Conditions: Characteristics of domestic demand, especially how discerning local consumers are in pushing for quality and innovation.

- Related and Supporting Industries: Presence of efficient suppliers, strong related industries, and synergistic business clusters.

- Firm Strategy, Structure, and Rivalry: How companies are formed, organized, and compete within the national industrial system.

Using this framework, the following sections examine how various provinces outside Java—namely Riau Islands, North Sumatra, East Kalimantan, and Central Sulawesi—develop their industrial parks. Riau Islands is chosen for its long-standing designation as an industrial area, while the other three represent western, central, and eastern Indonesia respectively. Each province will be assessed in terms of strengths and weaknesses across Porter’s four determinants to provide insight into the direction of industrial transformation in each region.

Riau Islands Province

Strategically located on Indonesia’s western edge, adjacent to Singapore and Malaysia, Riau Islands (Kepri) has evolved into a vital hub for trade and industry outside Java. It benefits not only from geographic proximity but also from integrated infrastructure, investment incentives, and global connectivity. Currently, Kepri hosts 19 industrial parks across Batam, Bintan, Karimun, and Bulang—the most outside Java.

From the perspective of Factor Conditions, Batam and its surroundings were systematically developed by the central government in the 1970s as a modern industrial zone equipped with international ports, airports, road networks, and reliable electricity. Industrial parks like Batamindo, Panbil, and Tunas have flourished atop this infrastructure. The local workforce is relatively skilled and disciplined, supported by polytechnics and technical training programs. As of 2022, Kepri hosted 1,200 medium and large industries employing over 100,000 workers.

Unlike other non-Java regions, Kepri’s Demand Conditions are largely shaped by international markets—especially Singapore, Malaysia, and ASEAN countries—pushing local industries to meet global standards and adopt export-oriented production.

This has fostered a mature Related and Supporting Industry ecosystem. Core industries like electronics, semiconductors, and shipbuilding are supported by component suppliers, logistics firms, customs services, banks, and vocational institutions. This synergy positions Kepri as one of the most integrated industrial clusters outside Java.

In terms of Firm Strategy, Structure, and Rivalry, Kepri is home to numerous multinational firms in manufacturing and services. Healthy competition drives innovation and efficiency, with local governments actively encouraging a conducive investment climate through incentives and streamlined business processes.

North Sumatra Province

North Sumatra (Sumut) is endowed with abundant natural resources, particularly in agriculture and plantations—most notably palm oil and rubber. These Factor Conditions have laid a strong foundation for the development of processing industries across the region. Adequate infrastructure further supports its growth as a strategic industrial zone.

Logistically, the Kuala Tanjung Port anchors North Sumatra in Batubara Regency, which is being developed as an international hub port integrated with the Kuala Tanjung Industrial Park (KIKT). With a depth of -16 meters LWS and a 500-meter quay, it can accommodate vessels of up to 100,000 DWT. Its connectivity is supported by toll roads and a railway line directly linking the port to the Sei Mangkei Special Economic Zone (SEZ), facilitating smooth goods distribution and reducing logistics costs. Additionally, Belawan Port in Medan serves as the region’s primary domestic and regional export gateway, supporting industrial activities in and around Medan, including those in the Medan Industrial Park (KIM).

On land connectivity, recent toll road developments have significantly improved inter-regional access:

- Medan–Tebing Tinggi–Parapat Toll Road links Medan with industrial park and tourism areas in Parapat;

- Kuala Tanjung–Tebing Tinggi–Parapat Toll Road provides direct access from the port to industrial parks and Lake Toba;

- Indrapura–Kisaran Toll Road enhances connectivity along the eastern coast of North Sumatra, easing the flow of goods to and from the ports.

From a Demand Conditions perspective, local demand is still emerging, concentrated mainly in major cities such as Medan, Binjai, Tebing Tinggi, and Pematang Siantar. However, export demand remains the primary driver of manufacturing and processing industry growth. According to Statistics Indonesia (BPS), North Sumatra’s exports reached USD 9.3 billion in 2023, dominated by:

- Palm oil and derivatives,

- Natural rubber and processed products,

- Pulp and paper,

- Food and beverage products.

Key export destinations include India, China, the Netherlands, and the United States, positioning local and national firms to consistently meet high international standards.

In terms of Related And Supporting Industries, North Sumatra’s industrial ecosystem—particularly for palm oil and rubber—is well established:

- Primary raw materials are supplied by both private and state-owned plantations (e.g., PTPN IV and PTPN III),

- Processing facilities for CPO and crumb rubber exist alongside downstream industries like oleochemicals and latex-based products,

- The Sei Mangkei SEZ offers integrated infrastructure and fiscal incentives, supporting seamless downstream processing within a single industrial zone.

This agribusiness ecosystem demonstrates strong integration across upstream, midstream, and downstream sectors. However, further synergies can be developed, particularly in research, product innovation, and value-added processing.

From the standpoint of Firm Strategy, Structure, And Rivalry, North Sumatra’s industrial landscape is dominated by large-scale enterprises, including national private companies, multinationals, and state-owned enterprises (SOEs). Notable players include PTPN III Holding (palm oil plantations and CPO production), Wilmar Group (palm oil processing facilities in Sei Mangkei), and PT Toba Pulp Lestari (pulp and paper industry in Tapanuli).

While the presence of such firms ensures industrial maturity, government incentives to foster innovation-driven competition—such as tax breaks for R&D and innovation-based procurement—remain limited and represent an area for policy improvement.

East Kalimantan Province

East Kalimantan (Kaltim) is undergoing a significant economic transformation. Historically known as a center for natural resource extraction—particularly coal, oil, and natural gas—the province is now shifting toward a more value-added, industrial-based economy. This transition has accelerated notably since the designation of East Kalimantan as the site of Indonesia’s new capital city, Nusantara (IKN), marking a paradigm shift from extractive industries to diversified, sustainable growth.

The development of IKN has unlocked new opportunities across multiple fronts, including increased domestic demand, infrastructure expansion, and enhanced investment attractiveness. Key industrial zones such as the Kariangau Industrial Park in Balikpapan and the Buluminung Industrial Park in Penajam Paser Utara are emerging as foundational pillars for East Kalimantan’s economic diversification strategy.

As a province rich in Factor Conditions, East Kalimantan continues to lead in energy resource production. According to BPS Kaltim (2024), the mining sector still contributes over 53% of the region’s GRDP, reaffirming its role as a vital contributor to Indonesia’s national energy supply. However, infrastructure development is rapidly advancing to support industrialization. Major logistics nodes—such as Kariangau Port and Palaran Seaport—facilitate heavy industry logistics, while the 99-kilometer Balikpapan–Samarinda toll road, now connected to IKN, serves as the backbone of regional land connectivity. Additionally, clean energy projects, including gas-powered and renewable plants, are being developed in zones like Buluminung.

Despite this progress, a key challenge remains: the shortage of skilled industrial labor. Addressing this will require significant investment in technical training and vocational education to meet the evolving needs of an industrialized economy.

The establishment of IKN has also been a catalyst for strengthening demand conditions in East Kalimantan. Previously, industrial demand was largely export-driven—centered on raw commodities like coal, LNG, and palm oil. Over the past three years, however, domestic demand has surged in line with IKN’s development. Sectors such as construction materials, light manufacturing, energy, and logistics have seen sharp growth, encouraging local industries to invest in downstream processing and construction-related manufacturing.

From the perspective of related and supporting industries, East Kalimantan is laying the foundation for a new industrial ecosystem. Several key industrial zones are being developed or expanded to serve as growth hubs:

- The Kariangau Industrial Park in Balikpapan, focused on wood processing, chemicals, energy, and logistics;

- The Buluminung Industrial Park in Penajam Paser Utara, strategically located near IKN, designated for energy, building materials, and agribusiness industries;

- The Maloy Batuta Trans Kalimantan SEZ in East Kutai, which supports palm oil and mineral-based processing industries.

Regarding Firm Strategy, Structure, And Rivalry, East Kalimantan’s industrial base is still dominated by large corporations. Key players include Pertamina and PLN in energy, Kideco Jaya Agung and Berau Coal in mining, and Pupuk Kaltim in downstream resource processing. However, competition in downstream manufacturing remains limited due to:

- Continued reliance on raw commodity exports;

- An underdeveloped small- and medium-sized enterprise (SME) sector;

- Limited competitive incentives for local product innovation.

Unlocking the province’s full industrial potential will require deliberate policy interventions to stimulate innovation, strengthen SME participation, and expand value-added production across sectors.

Central Sulawesi Province

Sulawesi’s economic corridor has long been positioned as a national center for the production and processing of agricultural commodities, plantations, oil and gas, and mining. Among its provinces, Central Sulawesi (Sulteng) stands out as a region undergoing a profound transformation—from an agrarian economy to one of Indonesia’s leading nickel processing centers. With abundant natural resources and expanding infrastructure, Central Sulawesi exemplifies the success of Indonesia’s downstream industrialization strategy.

The province holds an estimated 72 million tons of nickel reserves, placing it among the largest in the world. This strategic Factor Condition has attracted significant investment into industrial estate development. One of the most prominent is the Indonesia Morowali Industrial Park (IMIP), which has become a critical driver of both regional and national economic growth. Supporting infrastructure—such as dedicated ports, internal roads, and utilities—continues to expand. In 2023, the government initiated a new phase of development, adding 4,000 hectares to the industrial park, alongside drainage, road maintenance, and connectivity enhancements to improve logistics and mobility.

IMIP is equipped with advanced facilities and cutting-edge technology to process raw nickel into high-value products. These include ferronickel, stainless steel, and electric vehicle (EV) battery components, enabling a full value chain from laterite ore to globally competitive outputs.

From a Demand Conditions standpoint, global demand for nickel—especially for EV battery production—has accelerated industrial expansion in the region. In just the first quarter of 2024, Central Sulawesi’s nickel-related exports reached USD 4.82 billion. Domestically, the momentum of Indonesia’s infrastructure development and manufacturing growth continues to boost internal demand for processed nickel products, reinforcing Central Sulawesi’s position as a strategic industrial center.

The industrial parks in Morowali and Bahodopi have emerged as the largest nickel industry hubs in Southeast Asia. The downstream mineral processing taking place in these areas reflects a full value chain transformation—from laterite nickel to ferronickel, stainless steel, and EV battery precursors.

In terms of Related And Supporting Industries, a robust ecosystem has taken shape around the core processing operations. This includes:

- Nickel processors such as PT Indonesia Tsingshan Stainless Steel;

- Power suppliers (PLN and independent power producers);

- Logistics and transport providers, including specialized trucks, shipping services, and private ports;

- Engineering, construction, and waste management services.

However, the value chain remains largely vertically integrated and closed, with many supporting services controlled by foreign investors or internal affiliates of major corporate groups.

From the perspective of Firm Strategy, Structure, And Rivalry, competition among large industrial players remains limited due to the exclusive nature of the industrial estates—each major investor operates its own production lines with minimal overlap. Nonetheless, competitive dynamics are beginning to emerge in supporting sectors at the local level. Healthy rivalry is growing in areas such as:

- Local transport services for employee shuttles and logistics;

- Industrial catering and ready-to-eat food providers;

- Local construction subcontractors offering ancillary services to larger engineering firms.

While vertical integration has driven efficiency and output in the core nickel industry, the next stage of growth will depend on deepening the local supply chain, encouraging SME participation, and enhancing technology and innovation partnerships within the region.

Conclusion

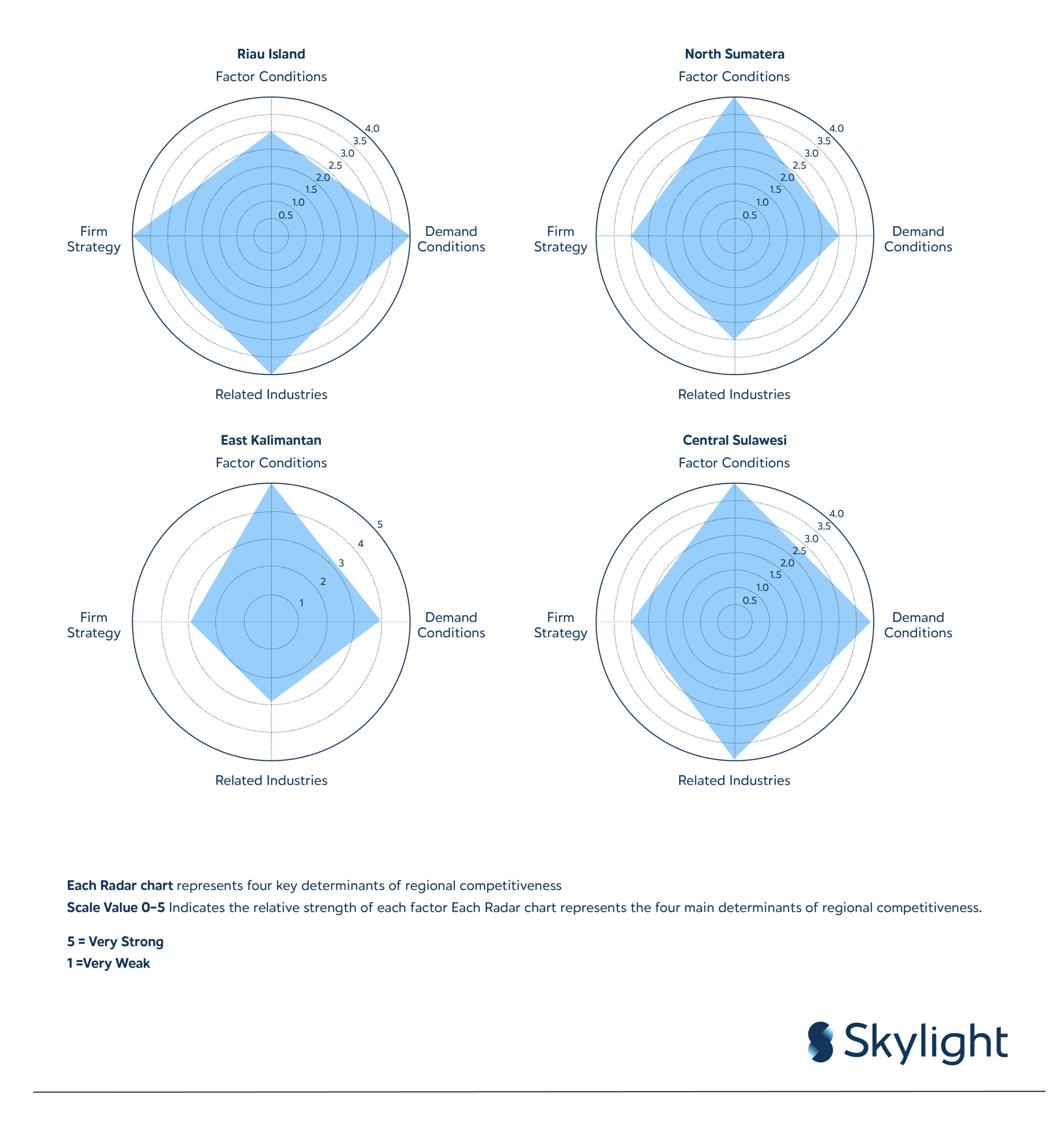

Using the Porter’s Diamond framework, it is evident that each region exhibits distinct competitive characteristics shaped by the interplay of factor conditions, demand conditions, related and supporting industries, and firm strategy, structure, and rivalry—alongside enabling or constraining government policies.

Figure 3: Radar Chart Porter’s Diamond Model

- In Riau Islands Province, strategic advantages stem from its proximity to Singapore and its location on international shipping routes. These geographic benefits have facilitated the development of light manufacturing, logistics, and electronics assembly clusters, especially in Batam and Bintan. However, constraints include limited natural resources and a small domestic market base, making the region’s growth trajectory heavily reliant on exports and foreign investment.

- North Sumatra serves as a major agro-industrial hub, anchored by key commodities such as palm oil, rubber, and coffee. These underpin a robust export structure. Nonetheless, downstream industrial integration remains underdeveloped, with weak linkages between agriculture and processing industries. While infrastructure—including toll roads, ports, and airports—is relatively advanced, further innovation and product diversification are needed to unlock the region’s full potential.

- East Kalimantan has long been a dominant player in Indonesia’s energy sector, endowed with substantial reserves of coal, oil, and gas. Its strategic relevance has increased with its designation as the site of the new capital (IKN), triggering major infrastructure investments. Despite this, the province remains highly dependent on extractive industries, with limited value-added processing, rendering it vulnerable to global commodity price fluctuations.

- Central Sulawesi has experienced rapid industrial transformation, largely due to nickel-based industrial zones such as the Indonesia Morowali Industrial Park (IMIP). The global push for electric vehicle battery materials has positioned the province as a focal point of mineral downstreaming. However, accelerated industrialization has also generated challenges—most notably, gaps in workforce quality, and unresolved social and environmental concerns.

Collectively, these four provinces benefit from relatively well-developed infrastructure conducive to industrial expansion. They also share structural challenges: a reliance on primary sectors, weak domestic supporting industries, and insufficient vocational training systems to supply competitive labor for high value-added activities.

To address these issues, downstream industrial development must prioritize strengthening local value chains, expanding employment, and driving inclusive economic growth. This requires improved governance—particularly in development planning, investment regulation, and environmental management. Coordinated policy action between central and local governments will be critical, not only to attract investment but also to ensure equitable distribution of economic gains.

Sources:

- Skylight Analytics Hub

- Badan Pusat Statistik Provinsi Kepulauan Riau. (2024). Statistik Industri Besar dan Sedang Provinsi Kepulauan Riau 2022.

- Badan Pusat Statistik Provinsi Kepulauan Riau. (2023). Perkembangan Ekspor Impor Provinsi Kepulauan Riau Desember 2022.

- Jurnal Industri. (2022). Daftar dan Alamat Perusahaan Yang Berada Di kawasan Industri Batamindo

- Badan Pusat Statistik Provinsi Sumatera Utara. (2024). Statistik Industri Manufaktur Besar dan Sedang Provinsi Sumatera Utara 2022.

- Bank Indonesia. (2022). Laporan Perekonomian Provinsi Sumatera Utara November 2022.

- (2024). Sei Mangkei Special Economic Zone.

- Badan Pusat Statistik Kalimantan Timur. (2024). Provinsi Kalimantan Timur Dalam Angka 2024.

Bank Indonesia. (2024). Laporan Perekonomian Provinsi Kalimantan Timur – November 2024.

Pemerintah Provinsi Kalimantan Timur. (2024). Kawasan Industri Provinsi Kalimantan Timur.

Badan Pusat Statistik Provinsi Sulawesi Tengah. (2024). Provinsi Sulawesi Tengah Dalam Angka 2024. - Bank Indonesia. (2024). Laporan Perekonomian Provinsi Sulawesi Tengah Agustus 2024.

- Kawasan Industri. (2024). Kawasan Industri Mendominasi 16 PSN Baru, Investasi Ratusan T Masuk Sulawesi.

- T Indonesia Morowali Industrial Park. (2024). IMIP Official Website.

- com. (2024). Menilik Pertumbuhan Masyarakat di Sekitar Kawasan Smelter di Sulawesi Dulu dan Kini. https://money.kompas.com/read/2024/07/01/145516526/menilik-pertumbuhan-masyarakat-di-sekitar-kawasan-smelter-di-sulawesi-dulu-danKOMPAS.com

- (2024). Hilirisasi Nikel di Sulawesi Tengah, Apa Saja Efeknya Bagi Ekonomi Daerah. https://finance.detik.com/industri/d-7408141/hilirisasi-nikel-di-sulawesi-tengah-apa-saja-efeknya-bagi-ekonomi-daerahdetikfinance

- Kementerian PUPR. (2023). Pengembangan Infrastruktur Kawasan Industri Morowali.

https://pu.go.id/berita/kementerian-pupr-kembangkan-infrastruktur-pendukung-psn-kawasan-industri-prioritas-morowali-sulawesi-tengah - CNN Indonesia. (2025). Longform IMIP, Nikel, dan Emas 2045.

https://www.cnnindonesia.com/longform/ekonomi/20250213/longform-imip-nikel-dan-sepiring-hati-untuk-indonesia-emas-2045/index.html\ - https://katadata.co.id/finansial/makro/67a30341b8ab4/ekonomi-papua-barat-tumbuh-paling-tinggi-melesat-20-8-imbas-proyek-gas-tangguh